1. Introduction

In 2017, the King of Saudi Arabia, King Salman, issued a royal decree that gave women the right to drive a car in the Kingdom of Saudi Arabia. Following this decree, June 24, 2018, was the first day for women to officially drive on the Saudi streets next to men. According to the General Authority for Statistics (GASTAT), and as reported in Saudi Gazette (2020), between June 24, 2018, and January 20, 2020, approximately driving licenses were issued to women in Saudi Arabia, with of them being Saudi women (see Figure 1).

The effects of this change have attracted interest from academics in social science. For instance, we can mention the recent papers Al-Garawi, Dalhat, and Aga (2021); Al-Garawi and Kamargianni (2021b, 2022), which are based on the surveys Al-Garawi and Kamargianni (2021a) that measure the social, economic, and environmental impact of women driving in Saudi Arabia. A further consequence of this enactment is that there is a new group of drivers with a need for insurance for which claim history is unavailable, making the question of fair insurance pricing of great relevance for the Saudi insurance industry.

In the same year, 2017, the Saudi Arabian Monetary Agency (SAMA) introduced a no-claim discount (NCD) system for the Saudi auto insurance market in response to a high number of road accidents (Middle East Insurance Review 2017). According to SAMA guidelines, insurance companies in Saudi Arabia must offer eligible discounts to their clients who do not report accidents for at least one consecutive year, with the discount increasing for each subsequent year, up to five years (SAMA 2016). Nonetheless, it is relevant to specify that this system only considers the number of accidents to determine the discounts and omits the claim severities, meaning that minor and severe accidents are punished equally. Hence, it may over-penalize policyholders generally involved in less severe accidents with no fatalities, which may be the case of women drivers as described in Al-Garawi, Dalhat, and Aga (2021).

Insurance companies in Saudi Arabia typically employ a-priori variables to determine their base auto insurance premiums. Thus, the Saudi NCD system is a-posteriori or merit-rating system that classifies policyholders into groups according to their risk. In fact, the Saudi NCD system is a particular example of the auto insurance pricing schemes known as Bonus Malus systems (BMSs). The origins of BMSs can be traced back to the early 1960s in the European insurance market, and their optimal design is based on the seminal work of Bichsel (1964); Bühlmann (1964); Delaporte (1965). More recently, Lemaire (1995) provided a modern and exhaustive treatment of BMSs, including a comprehensive list of references, modeling and evaluation tools, and an in-depth description of 31 systems worldwide. The fundamental principle of a BMS is that the policyholder will receive a premium discount (Bonus) if they file no claim during the prior year or a premium rise (Malus) if there is a claim. Typically, these systems are organized into classes with different premium levels and employ the current policy year claim history and class to determine the following year’s class of an insured. The vast majority of implemented BMSs, as is the case of the Saudi NCD system, consider the claim frequency solely to determine the movement of policyholders in the different classes. For instance, of the 30 systems studied in Lemaire and Zi (1994), only the Korean BMS penalizes the policyholders depending on their claim numbers and sizes. In this system, accidents that caused property damage (PD) are distinguished from those that caused bodily injury (BI). The latter are penalized more since, on average, they claim more.

To the best of our knowledge, the NCD system of the Saudi Arabian auto insurance market has not been studied in the actuarial literature. Thus, this paper aims to investigate the Saudi NCD system for third-party insurance coverage with the following question in mind:

-

Are the Saudi NCD’s current rules ensuring long-term financial stability for policyholders and insurance companies?

-

Are the current rules adaptable for the new generation of women drivers in Saudi Arabia?

The remainder of the paper is organized as follows. Section 2 presents the rules of the current Saudi BMS and establishes the essential modeling tools for its study. The Saudi BMS is evaluated in Section 3 by examining its convergence rate (Section 3.1), mean asymptotic premium level (Section 3.2), and elasticity (Section 3.3). Section 4 includes a sensitivity analysis of the Saudi BMS to changes in the claim frequency of a policyholder. Finally, Section 5 concludes.

2. The Saudi BMS

Insurance companies in Saudi Arabia consider multiple rating factors to determine their premiums. Some of the factors they may consider are: policyholder information (age, occupation, type of driving license, region, claim history, traffic violations, etc.), type of motor insurance policy (comprehensive or third-party), vehicle-related characteristics (manufacturer, model, year of manufacture, etc.), and any additional benefits that the insured wishes to include in their policy. However, given that each insurance company selects the rating factors they consider appropriate for their insurance pricing, the previous list is not comprehensive.

In addition, Saudi insurers must offer discounts to their policyholders based on their claim history according to a government-imposed NCD system (or BMS) monitored by the Saudi Arabian Monetary Agency (SAMA). This Saudi Arabian BMS provides discounts depending on the current category of the policyholder and their number of claims in the previous year. The bonus structure ranges between 10% and 50% for third-party policies and 15% to 60% for comprehensive insurance coverage, these two being the most significant motor coverages offered in Saudi Arabia. The detailed discount system for third-party and comprehensive policies is presented in Table 1, retrieved from Middle East Insurance Review (2017).

In Saudi Arabia, as in other countries, by law, third-party liability insurance is a compulsory/mandatory insurance for drivers. This policy covers the damage caused by the policyholder’s vehicle to third parties (individuals and properties), but it does not compensate for the damage inflicted on the insured driver or the insured’s vehicle. On the other hand, a comprehensive policy, which is optional, includes all the coverages of third-party insurance plus compensation for damages to the policyholder, their vehicle, and passengers.

No-claim discounts encourage insured drivers to adopt safer driving practices since the more consecutive years without reporting claims, the more significant the discount they will receive. In the long run, via this system aims, the drivers are assessed fairer according to their driving behaviors.

The rest of this paper considers only third-party liability coverage since it can be regarded as more relevant to the Saudi insurance market due to its obligatory status. In fact, Saudi traffic management does not allow car registration or renewal requests unless a car owner has a valid third-party liability policy.

We now give a more detailed representation of the BMS described in Table 1 for third-party policies. First, we divide insured drivers into six classes ranging from 1 to 6, with premium levels 100, 90, 80, 70, 60, and 50, respectively. This means new policyholders start in class 1 at level 100, and each claim-free year results in a one-class movement with a higher discount. For instance, if a new policyholder does not report a claim for five consecutive years, they will be in class 6 with a premium level of 50. Moreover, reporting one or more claims is penalized as follows:

-

If the policyholder is in class 1, they will remain in the same class.

-

If the policyholder is in one of classes 2 or 3, they will return to class 1.

-

If the policyholder is in class 4, they will return to class 2.

-

If the policyholder is in class 5, they will return to class 3.

-

If the policyholder is in class 6, they will return to class 4.

For clarification, the movement occurs when the claim is reported. Settlement and payment of claims may take a long time, especially for BI claims and death cases, hence the reason that the transition occurs when the claim is reported. Table 2 summarizes the transition movements of insured drivers based on their number of claims during one policy period.

We now establish the basic modeling setup to study the Saudi BMS.

2.1. Modeling the Saudi BMS

Like most BMS (cf. Lemaire (1995)), the Saudi NCD system can be modeled using a discrete-time Markov chain. To justify this statement, we observe that only the knowledge of the number of claims within a policy year and the current class is required to determine next year’s policyholder class. In other words, the future class for a policyholder is independent of the past and dependent only on the present, which is the property of a (first-order) Markov chain. Moreover, in this section, we assume that the driving patterns of a group of policyholders remain constant over time, implying that the Markov chain is time-homogeneous. This last assumption may not hold for a group of novice drivers, given that changes in their driving abilities may be expected due to experience. However, in the long run, they can be expected to reach stable driving practices, making the present analysis relevant. In Section 4, we consider a scenario with improvements in the driving patterns of a group of insureds. Next, we give the formal mathematical definitions.

Let be a discrete-time time-homogeneous Markov chain on a state-space In this case, represents the number of classes in a BMS, each state in denotes a particular BMS class, and describes the movement of a policyholder through the different classes in time. Furthermore, we denote by the transition probabilities of going from state to state in one-step, that is, and by the corresponding (one-step) transition matrix Thus, we obtain the following one-step transition matrix describing such a system

P=[p11p120000p210p23000p3100p34000p4200p45000p5300p56000p640p66].

Figure 2 shows the transition diagram of the Saudi BMS.

To fully specify the transition probabilities of the Markov chain describing the movement of a policyholder within the classes of the Saudi BMS, we now make an assumption regarding their claim frequency. According to studies by Hossack, Pollard, and Zehnwirth (1999); Frangos and Vrontos (2001); Kaas et al. (2008), a Poisson distribution is an appropriate model for the claim frequency of individual drivers. Therefore, we assume that the number of claims of a driver follows a Poisson distribution with parameter also referred to as the claim frequency of the policyholder. Then, the probability of observing claims in one period when the claim frequency is is given by

pk(λ)=e−λλkk!,k=0,1,….

Furthermore, the assumption of being constant over time yields the transition matrix below

P(λ)=[1−p0(λ)p0(λ)00001−p0(λ)0p0(λ)0001−p0(λ)00p0(λ)0001−p0(λ)00p0(λ)0001−p0(λ)00p0(λ)0001−p0(λ)0p0(λ)].

Although the claim frequency may vary individually in a group of policyholders, we are interested in studying the behavior of the BMS for a whole cohort of drivers. Hence, for our analysis, we consider the claim frequency of an “average” driver in the group. In the present case, we assume in what follows. There are two main reasons for this assumption. Firstly, this allows for comparison with the BMSs analyzed in Lemaire and Zi (1994), given that the same was employed there. Secondly, the Saudi insurance company “Allied Cooperative Insurance Group” (ACIG) gratefully provided us with a claim insurance data set for the years 2017 to 2021. In this database, the average claim frequency over all the policyholders for 2017 to 2019 is 0.097, 0.094, and 0.092, respectively, which is close to our assumption of The years 2020 and 2021 exhibit much lower claim frequencies (0.068 and 0.074, respectively), which can be attributed to the COVID-19 pandemic. This shows that the assumption of being constant over time may not be totally realistic since it can be affected by some “rare” events. However, it still provides insightful information and makes the analysis mathematically tractable. Thus, with this value of the claim frequency, we obtain the transition matrix below.

P(0.1)=[0.095160.9048400000.0951600.904840000.09516000.904840000.09516000.904840000.09516000.904840000.0951600.90484].

In particular, observe that policyholders with have a 90.48% chance (the probability of not making a claim) of moving upwards in the system in each step.

Given that a new insured can reach the maximum discount level in the Saudi BMS within a minimum of five years, we are now interested in studying the system’s behavior after a certain number of years, which we denote by For such a purpose, we look at the -step transition probabilities of the Markov chain. Here, in full generality we write to denote the transition probabilities of going from state to state in -steps/periods, that is, Note that these transition probabilities can be computed using the well-known Chapman-Kolmogorov equation

p(n)ij=∑kp(n−m)ikp(m)kj,

where and for any states (see, e.g., Resnick (1992)). Furthermore, we denote by the -step transition matrix of the process, that is, In particular, (2.3) implies that

P(n)=Pn=P⋯P⏟n-times.

We also write to denote the -step transition matrix associated with 2.2. Thus, for the five-step transition matrix of the Saudi BMS with is given by

P(5)(0.1)=[0.024660.029030.205490.070500.063790.606530.024660.029030.014120.261870.063790.606530.004540.049150.014120.070500.255160.606530.004540.008900.054380.070500.063790.797900.004540.008900.014120.110750.063790.797900.002420.011020.014120.090620.083920.79790].

For the matrix above, we observe that after five steps, approximately 61% of new insureds with will reach the class with the highest discount (50%).

Next, we are interested in studying the system behavior over the long-run, that is, when First, notice that the Makov chain describing the Saudi BMS is irreducible (it is possible to go from every state to every other state) and positive recurrent (we have a finite number of classes). Then, there exists a vector called the stationary distribution, satisfying

ππ(λ)=ππ(λ)P(λ).

The vector represents the probability of a policyholder being in each of the given states when the number of periods tends to infinity. This last statement becomes clear from the limit relationship below, which follows by noticing that the Markov chain is aperiodic:

lim

where denotes the column vector of ones of appropiated dimension. Finally, it is easy to show that (2.4) has explicit solution given by

\small{ \begin{aligned} \pi_1(\lambda) &= \frac{1-p_0(\lambda)-3(1 - p_0(\lambda))p_0(\lambda)^2+2(1 - p_0(\lambda))p_0(\lambda)^3}{(1-3(1 - p_0(\lambda))p_0(\lambda)^2)}\,, \\ \pi_2(\lambda) &= \frac{(1-p_0(\lambda)-2(1 - p_0(\lambda))p_0(\lambda)^2+(1 - p_0(\lambda))p_0(\lambda)^3)p_0(\lambda)}{(1-3(1 - p_0(\lambda))p_0(\lambda)^2)}\,, \\ \pi_3(\lambda) &= \frac{(1-p_0(\lambda)-(1 - p_0(\lambda))p_0(\lambda)^2)p_0(\lambda)^2}{(1-3(1 - p_0(\lambda))p_0(\lambda)^2)}\,, \\ \pi_4(\lambda) &= \frac{(1-p_0(\lambda))p_0(\lambda)^3}{(1-3(1 - p_0(\lambda))p_0(\lambda)^2)}\,,\\ \pi_5(\lambda) &= \frac{(1-p_0(\lambda))p_0(\lambda)^4}{(1-3(1 - p_0(\lambda))p_0(\lambda)^2)}\,,\\ \pi_6(\lambda) &= \frac{p_0(\lambda)^5}{(1-3(1 - p_0(\lambda))p_0(\lambda)^2)} \,. \end{aligned} }

Thus, for the particular instance, we obtain

\small{ \pmb{\pi}(0.1)=[0.00316, 0.01161, 0.01843, 0.09200, 0.08325, 0.79154] \,, \tag{2.5} }

indicating that approximately of drivers will eventually reach the class with the biggest discount.

3. Evaluation of the current Saudi BMS

Historically, insurance rating has been about having policyholders pay premiums proportional to the risk they bring to the insurance company, thereby dividing claim costs more fairly. As previously mentioned, a primary characteristic of a BMS is that it classifies policyholders according to their risk. However, it is essential to determine how well a BMS assigns premiums according to the different risk levels of insured drivers. In this section, we assess the efficiency of the current Saudi BMS by employing a series of tools from Lemaire (1998). Moreover, we compare our results with the Malaysian and Brazilian BMSs described in Appendix A. We have selected these two systems given that they possess a similar number of classes to the Saudi BMS: 6 classes in the Malaysian system and 7 classes in the Brazilian one. For completeness, Appendix A also includes the one-step transition matrices and stationary distributions of these systems when

3.1. Rate of convergence

First, we are interested in evaluating the rate of convergence of the Saudi BMS towards its steady-state condition, given that important BMSs evaluation tools assume that stationarity has been reached (see Lemaire and Zi (1994) for a survey on different evaluation methods). Defined by Bonsdorff (1992), the total variation is a measure of the degree of convergence of a BMS after transitions/years. More specifically, given a specific class of the BMS (typically the starting class of the system) and a number of steps the total variation is defined as

TV_n (i) = \sum_j\left|{p_{ij}^{(n)}(\lambda)}-{\pi_j(\lambda)}\right| \,.

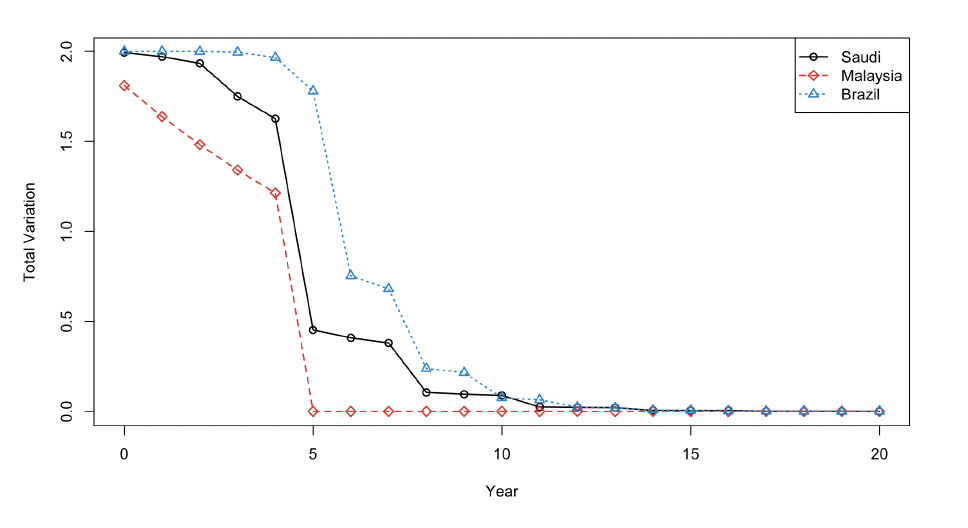

Figure 3, which is complemented by Table 3 , shows the behavior of over 20 years when is the starting class of the BMSs. We observe that for the Malaysian system, for all indicating that it reaches full stationarity after only five years. In fact, the Malaysian BMS is considered one of the simplest systems in the world, where just one claim reported yields the loss of all discounts achieved before (see Manan, Hashim, and Mohd (2013)). On the other hand, the total variation of the Saudi and Brazilian BMSs decreases towards zero over time. This confirms the observation in Lemaire (1995) that more sophisticated BMSs converge much more slowly than simple ones. Regarding these last two systems, observe that although the total variation of the Saudi BMS is lower in the initial years, the opposite happens in the late years. It is worth remarking that a slow convergence of a system can be seen as a drawback, given that the primary purpose of a BMS is to differentiate between safe and reckless drivers by having a classification system, which ideally stabilizes as early as possible.

To give an approximation of the number of years it will take these systems to stabilize fully, we find the minimum value of such that

\max_{i = 1, \dots, s} TV_n (i)

is below a given threshold In particular, we consider obtaining years for the Saudi system and for the Brazilian one. We note that a convergence period above years exceeds the expected driving half-life of most policyholders and the “life expectancy” of almost any BMS. This emphasizes our previous comment that fast convergence of a BMS is a desirable characteristic.

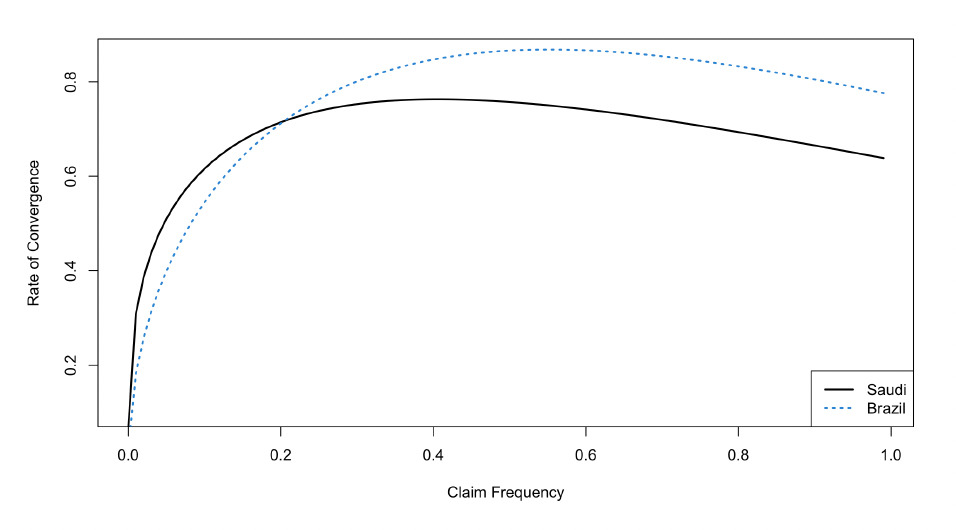

In fact, and as described in Lemaire (1995), the rate of convergence of (3.1) can be characterized by means of the eigenvalues of the transition matrix More specifically, we can define the rate of convergence as

\begin{aligned} r(\lambda) = \max \left( |\alpha_1(\lambda)|, \dots, |\alpha_{s-1}(\lambda)| \right) \,, \end{aligned}

where are the eigenvalues of different from 1 is always an eigenvalue of cf. (2.4)), and denotes the modulus of the eigenvalue. Note that all eigenvalues different from 1 lie inside the unit circle of the complex plane, implying that for all Moreover, a low value of indicates a faster convergence of a BMS (cf. (Lemaire 1995, vol. 19, chap. 9) for details). Figure 4 depicts the rate of convergence for the Saudi and Brazilian BMSs as a function of Note that the Malaysian system is not included since it reaches full stationarity after five years, which implies that all but one of the eigenvalues of its transition matrix are 0. We have that for for the Saudi system, and for the Brazilian one, indicating that the Brazilian BMS converges faster than the Saudi BMS, agreeing with the conclusions raised previously. Furthermore, note that for all values of below the rate of convergence of the Saudi system is above the one of the Brazilian system, which is worth remarking given that ordinary drivers are expected to fall in the range (cf. Lemaire (1995)).

3.2. Mean asymptotic premium level

We are now interested in studying the average premium level paid by policyholders in the Saudi NCD system over time. In what follows, we denote by the premium level in class of a BMS, Thus, for instance, the Saudi BMS has corresponding values and First, we note that the mean premium level for new insureds after years is given by

\begin{aligned} \sum_{i=1}^{s}p_{1i}^{(n)} b_i \,. \end{aligned}

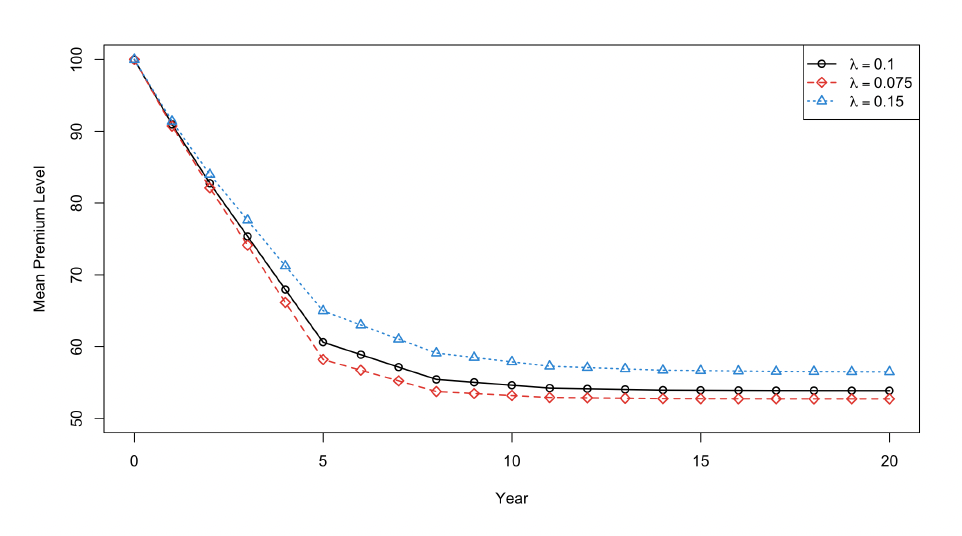

The evolution over time of the mean premium of new policyholders in the Saudi Arabian, Malaysian and Brazilian BMSs is presented in Figure 5. We observe that the Brazilian system has the highest mean premium level value at all times while the Malaysian system takes the lowest values in the first seven years, and from year eight, the Saudi system becomes the system that has the lowest value of the average premium level. Note that the Malaysian BMS reaches its lowest value in the fifth year, given that the stationary distribution is obtained after five steps. On the other hand, the other two systems converge slowly to their minimum values.

3.2.1. Mean stationary premium level

In the long term, the yearly average premium level to be paid by the insureds is determined by the mean stationary premium level given by

\begin{aligned} P(\lambda) = \sum_{i=1}^{s}\pi_i(\lambda) b_i \,. \end{aligned} \tag{3.2}

The corresponding values of for the Saudi, Malaysian, and Brazilian BMSs are 53.85, 56.58, and 65.65, correspondently, which are somewhat close to their minimum premium levels (50, 45, and 65, respectively). Note that a low mean stationary premium level may be seen as a drawback since the premium level of the entry class is substantially higher than the average stationary premium level, meaning that new policyholders pay considerably higher premiums than long-term customers.

3.2.2. First-year surcharge

The effect of new insureds paying substantially higher premiums than existing customers can be more accurately assessed through the first-year surcharge, which is computed as

\begin{aligned} \frac{\text{Entry premium level} - P(\lambda)}{ P(\lambda)} \,. \end{aligned}

Note that this measure takes into account the premium levels of a system and therefore is better suited for comparing different BMSs. We have that the first-year surcharges for the Saudi, Malaysian and Brazilian systems are and respectively, indicating that the Saudi BSM penalizes new policyholders the hardest. This is particularly relevant given that we have an exceptionally large group of new drivers in the Saudi market, which will pay a high premium compared to pre-existing drivers. In fact, it is worth noting that in Saudi Arabia, new female drivers have been penalized more in their base premium (a priori) than males by some insurance companies because they are seen as potential high-risk drivers due to their lack of claim history, further aggravating the difference in premiums paid by new and long-term costumers.

3.2.3. Relative stationary average level

Given that different BMSs have distinct premium levels, their mean stationary premiums are not directly comparable. Hence, we next consider the relative stationary average level (RSAL). This measure specifies the relative position of an average policyholder when the lowest premium is set equal to zero and the highest to 100 and is found via the expression

\small{ \mbox{RSAL}(\lambda) = \frac{\text{Stationary mean premium level} - \text{Minimum value of}\ b_i}{\text{Maximum value of}\ b_i\ - \text{Minimum value of}\ b_i} \,. }

A low value of RSAL suggests a large concentration of policies in the BMS class with the highest discount. On the other hand, an efficient spread of policies among the BMS classes is achieved with a high value of RSAL. For the three systems considered here, we have that the Malaysian BMS has the larger RSAL followed by the Saudi BMS and ultimately, the Brazilian BMS

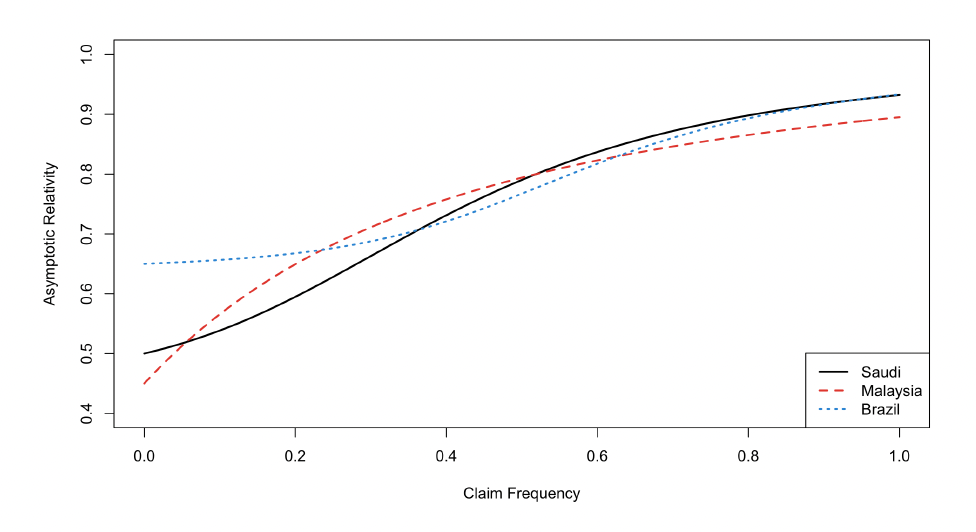

3.2.4. Asymptotic relativity

To conclude our study on the mean asymptotic premium, we present a plot of (3.2) as a function of in Figure 6. Note that in this last plot, we have considered as a percentage; in such a case, (3.2) is also known as asymptotic relativity. In particular, observe that for the three curves, there exists a value such that and only drivers with this claim frequency will eventually pay a fair premium. The corresponding values of for the Saudi, Malaysian and Brazilian BMSs are 0.92102, 0.87829, and 0.92039, respectively, which are very large values.

3.3. Elasticity

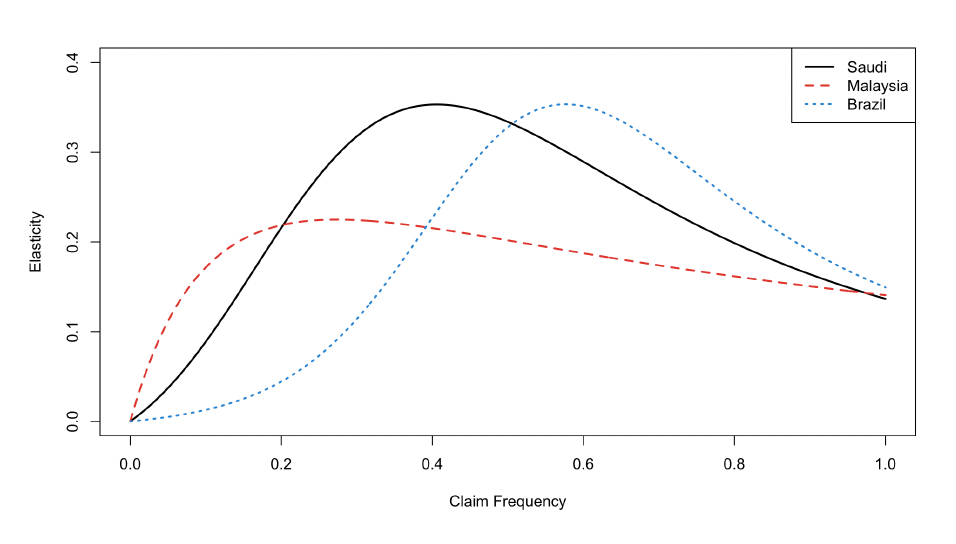

Introduced by Loimaranta (1972) under the name of efficiency, the elasticity of a BMS is a measure of the relative change in the mean stationary premium level with respect to a relative change in the claim frequency More concretly, the elasticity is given by \eta (\lambda) = \frac{ dP(\lambda) }{P(\lambda)}\frac{ \lambda }{d\lambda} \,. Ideally, an increment of should lead to an equal change of that is, In such as case, we say that a BMS is perfectly elastic. On the other hand, a low value of is an indication that those who drive safely (low-risk policyholders) subsidize those who drive unsound (high-risk policyholders). For the considered claim frequency of the Malaysian BMS has a larger elasticity than the Saudi and the Brazilian BMSs. Figure 7 gives the elasticity of these three systems for values of between 0 and 1. We observe that for values of below the Malaysian BMS presents the largest elasticity. For values between and the Saudi BMS has the highest efficiency, and finally, for values above it is the Brazilian BMS the one with the largest Moreover, note that the maximum elasticity of the Saudi system is attained with Overall, all three NCD systems have an efficiency of less than 1, indicating that they are not perfectly elastic. However, the Malaysian NCD system is the most efficient compared to the Brazilian and Saudi systems for the range of claim frequencies where most policyholders are expected to fall This suggests that the Malaysian system is relatively more responsive to changes in claim frequencies.

4. Possible claim frequency scenarios when women drivers are considered

For the year 2021, the ASIG dataset is constituted of active policyholders, of which only are female drivers. Hence, given the relatively low number of female drivers currently in Saudi Arabia, there is still insufficient evidence to support our previous assumption of for this group of new insureds. Hence, we now investigate how the Saudi BMS responds to changes in the drivers’ claim frequency. First, we consider two base scenarios, a low claim frequency of and a high claim frequency of and compare our results with the findings in the previous section. Next, we consider a scenario where we assume improvements in the driving patterns of this cohort of novice drivers and give some conclusions regarding the effects of this assumption in the Saudi BMS.

We start by calculating the one-step transition matrices associated with the two base values of :

\small{ \boldsymbol{P}(0.075)= \begin{bmatrix} 0.07226 & 0.92774 & 0 & 0 & 0 & 0 \\ 0.07226 & 0 & 0.92774 & 0 & 0 & 0 \\ 0.07226 & 0 & 0 & 0.92774 & 0 & 0 \\ 0 & 0.07226 & 0 & 0 & 0.92774 & 0 \\ 0 & 0 & 0.07226 & 0 & 0 & 0.92774 \\ 0 & 0 & 0 & 0.07226 & 0 & 0.92774 \end{bmatrix} }

and

\small{ \boldsymbol{P}(0.15)= \begin{bmatrix} 0.13929 & 0.86071 & 0 & 0 & 0 & 0 \\ 0.13929 & 0 & 0.86071 & 0 & 0 & 0 \\ 0.13929 & 0 & 0 & 0.86071 & 0 & 0 \\ 0 & 0.13929 & 0 & 0 & 0.86071 & 0 \\ 0 & 0 & 0.13929 & 0 & 0 & 0.86071 \\ 0 & 0 & 0 & 0.13929 & 0 & 0.86071 \end{bmatrix} \,. }

Next, we compute the corresponding stationary distributions:

\begin{aligned} \pmb{\pi}(0.075) = [0.00132, 0.00635, 0.01065, 0.07093, 0.06581, 0.84493] \end{aligned} and \begin{aligned} \pmb{\pi}(0.15)= [0.01065, 0.02709, 0.03874, 0.12864, 0.11072, 0.68416] \,. \end{aligned}

Note that even in the case with high frequency, over half of policyholders will end up in the class with the minimum premium level and less than 2% in the class with the highest premium level. This means that in the current Saudi BMS, new policyholders will pay considerably higher premiums than a big proportion of pre-existing clients, even if the latter group has a substantial number of claims.

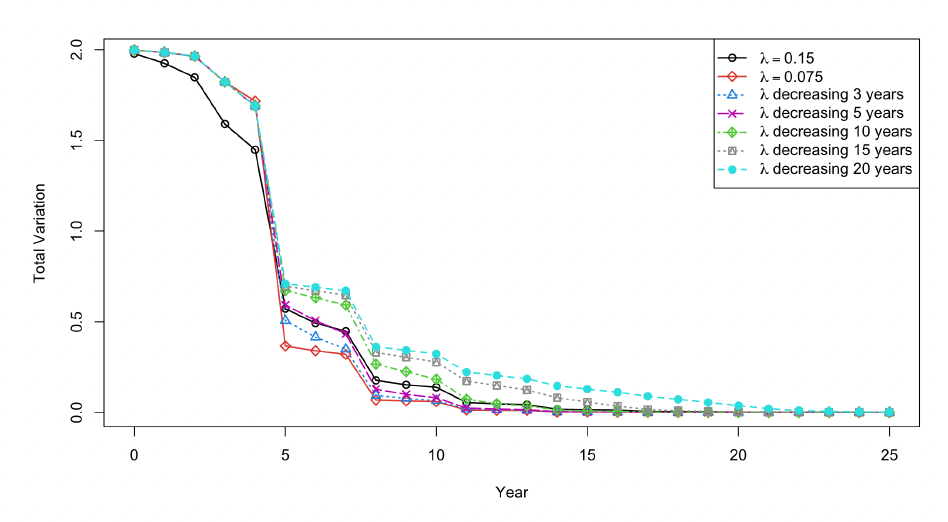

Next, we study the evaluation tools presented in Section 3 in the two scenarios considered. We start by giving a plot of the evolution of the total variation in a 20-year period for these two claim frequencies (Figure 8).

We notice that, although the total variation under the high-frequency case is lower in the first five years, the opposite happens in the subsequent years, indicating a slower convergence. This is confirmed by looking at Figure 4, where we observe that the rate of converge for is which is lower than the corresponding rate for of implying faster convergence of the former case. Furthermore, we approximate the number of years for the system to completely stabilize under these two claim frequency scenarios by finding the minimum value of such that (3.1) is below obtaining 38 years for the case and 52 years for the scenario. Hence, new insured groups with high claim frequencies will take longer to reach full stationarity in the Saudi BMS.

Regarding the mean asymptotic premium level, we first note that is an increasing function of the claim frequency (see Figure 6). For the specific values of under study, we have that and which are very close to the previously computed value of . In fact, the relative difference is only -2.10% in the former case and 4.85% in the latter. Note that these small changes in are expected given that, and as described in Section 3.3, the Saudi BMS exhibits a very low elasticity. Figure 9 shows the evolution of the mean premium levels for new policyholders. Additionally, observe that the first-year surcharge in both cases is still quite high, being 89.69% for and 77.12% for indicating that the Saudi BMS severely penalizes new insureds even if they are hazardous drivers. Likewise, we have that the RSAL with is 5.43% and with is 12.92%, leading to similar conclusions.

Finally, the elasticity in both scenarios is relatively low, as shown in Figure 7. More specifically, we have a value of 0.06138 for the first scenario with and 0.15103 for the other scenario with

We now consider a scenario where we allow for improvements in the claim frequency in a cohort of policyholders over time. This is particularly relevant given that gradually lower claim frequencies for a group of novice drivers may be expected due to, for example, more experience. However, here we assume that the driving patterns of a group reach a plateau after a specific time. Our primary goal is to determine how the time (in number of years) it takes a cohort of policyholders to reach this plateau impacts the convergence of the Saudi BMS. To this end, we assume that a group of novice insurers has an initial claim frequency of and that after years of driving experience, it reaches with Moreover, for computational purposes, we assume that the decrement in the claim frequency is linear. Thus, for instance, Table 4 shows the values of the claim frequency from a starting value of to in 3 years.

We first note that under this setting, we now have a time-inhomogeneous Markov chain. However, after years, the one-step transition probabilities can be computed as in a time-homogeneous chain. In particular, we have that for the -step transition matrices can be written as

\begin{aligned} \boldsymbol{P}^{(m)} \boldsymbol{P}^{n - m}(\lambda_{end}) \,. \end{aligned}

Taking limit when in the expression above yields

\begin{aligned} \boldsymbol{P}^{(m)} \boldsymbol{P}^{n - m}(\lambda_{end}) \to \boldsymbol{P}^{(m)} \pmb{1} \pmb{\pi}(\lambda_{end}) = \pmb{1} \pmb{\pi}(\lambda_{end}) \,, \end{aligned}

implying that the stationary distribution of this Markov chain exists and coincides with the one associated with the time-homogenous Markov chain obtained with This means that all our previous analyses with evaluation tools based on the steady-state condition, such as the mean stationary premium level, hold under this setup.

We are now interested in the effects of our assumption on the convergence of the Saudi BMS. We start by providing Figure 10, which shows the behavior of over 25 years when and for different improvement periods We observe that longer claims frequency improvements lead to larger values of the total variation or, in other words, slower convergence of the Saudi NCD. To quantify this effect, we approximate the number of years it takes the system to completely stabilize under some claim frequency improvement scenarios. More specifically, we consider three combinations of and to to and to with five different values of 3, 5, 10, 15, and 20. Table 5 shows the total number of years to reach convergence on these scenarios and the additional years compared to the number of years obtained with a constant clam frequency assumption. Recall that for constant values of of and we previously obtained 38 and 43 years to convergence, respectively. Thus, for instance, for and we get 49 years to convergence, which is 6 years more than using constant This supports our previous conclusion that longer claims frequency improvements lead to slower convergence of the Saudi BMS.

As previously mentioned, most countries utilize BMSs with rules based only on the number of accidents/claims without considering the severity of such claims. This may be considered unfair because a policyholder with some small (less severe) claims may have to pay a higher premium than another who reports only one costly claim. Consequently, policyholders are encouraged to search for more affordable premium prices in other insurance companies. For example, the annual statistics SAMA (2021) shows that from 2018 to 2020, the percentage of policyholders who continued their insurance coverage with the same insurance company after their initial term expired declined from 94% to 92%.

According to the Ministry of Justice’s statistics (Saudi Gazette 2019), in 2019, around 20% of the traffic accidents involved women drivers, and 40% of them were rear-ended collisions mainly due to issues with parking or breakdowns. Additionally, the recent studies by Al-Garawi, Dalhat, and Aga (2021); Al-Garawi and Kamargianni (2021b, 2022) found that approximately 17.40% of novice women drivers in Saudi Arabia are involved in property damage accidents while about 0.72% in minor/serious-injury road traffic accidents due to the general high fear of driving. Moreover, no fatal accidents among these drivers were reported in the periods studied. This may be due, up to a certain degree, to the rigorous training program required via Public Driver School in Saudi Arabia. In general, studies by Hellman (1997); Butler (1996) suggest that women drivers are usually involved in low-risk accidents compared to men drivers. A particular case where this occurs is in long-distance driving, which is more likely to have high-severity claims than city/town driving and is more commonly performed by men (Santamariña-Rubio et al. 2014; Butler, Butler, and Williams 1988; Butler 1996). However, there is still insufficient information to support any claim frequency hypothesis for these novice female drivers. Nevertheless, and as argued previously, for several claim frequency scenarios, the premium level to be paid by these new customers will be high compared with the premiums of drivers with more time in the system. Moreover, the convergence of this group to the stationary distribution will be slow. Hence, the current Saudi NCD system may not be fully ready for the new group of novice women drivers.

5. Conclusion

We have presented and analyzed the current Saudi no-claim discount system. We employed several evaluation tools for our analysis, such as the rate of convergence, mean stationary premium level, and elasticity, all using an initial claim frequency of Based on these measures, we concluded that the Saudi BMS convergences slowly towards its stationary distribution, severely penalizes hard new insureds, and does not adapt well to claims frequency changes. Moreover, this selection of allows comparison of the results presented here with similar investigations of other BMSs worldwide, such as the ones given in Lemaire and Zi (1994). Subsequently, we performed a sensitivity analysis of the Saudi BMS regarding changes in the claim frequency, which is particularly relevant to determining the system’s suitability for the new group of novice women drivers, given that they are generally involved in more accidents (although less severe), and do not have much driving history.

In summary, this work shows the necessity of designing a new BMS for the Saudi insurance market, which may be fairer for these novice drivers. In this line of thinking, we would like to mention that a feasible approach/option could be to develop a new BMS which incorporates claim severity into its rules. Nevertheless, a thoughtful analysis of a potential new BMS with these characteristics is outside the scope of the present paper and represents a promising line for future research. However, we can point out that a good starting point could be to analyze the suitability of a system similar to the Korean BMS described in Lemaire and Zi (1994).

Acknowledgement

Asrar Alyafie would like to acknowledge financial support from the Ministry of Education (Kingdom of Saudi Arabia) and the University of Jeddah.

We want to thank Allied Cooperative Insurance Group for providing us access to the mentioned dataset and especially Mr. Mohammed A. Al-Gadhi for sharing his expertise in the Saudi Arabian insurance market.