1. INTRODUCTION

Autonomous driving technologies have made significant progress in recent years. Autonomous Vehicles (AVs) have been deployed for ride-hailing and delivery services in many countries such as the United States and China. Assessing liability exposure presents a unique challenge for actuaries as there is little past experience to rely on. In addition, the traditional framework based on personal liability and tort that has long enabled insurance companies to act as a proxy for courts and efficiently resolve liability disputes involving human vehicle operators may evolve once at least one party in an accident is no longer human. The question of how to allocate liability following a collision involving an AV is an active area of discussion among legal professionals and scholars (Reed 2020). Additionally, a number of unprecedented challenges complicate the tasks of the actuaries, underwriters, and insurance professionals charged with quantifying these risks.

One important nuance is the potential blend of traditional product liability and personal liability exposures. As the manufacturer and operator of autonomous vehicles, AV companies will assume responsibility for both driving prudence and the proper design and maintenance of autonomous vehicles. An additional complication emerges from the varying AV regulations between states. Some states, like California, require AV operators to carry liability insurance with limits much higher than that for commercial auto insurance while others require limits more consistent with traditional commercial autos. Further, given the relative scarcity of AVs on public roads, the actuary is faced with a dearth of historical data on claim valuations from which to project future liability potential.

Aside from the very limited experience available for autonomous driving, there is also a question about the value of past experience in loss projection for future exposure periods. The software that drives vehicles is constantly improved to mitigate undesirable behaviors. That means past experience may potentially be less powerful or relevant in predicting future losses by comparison to human driving.

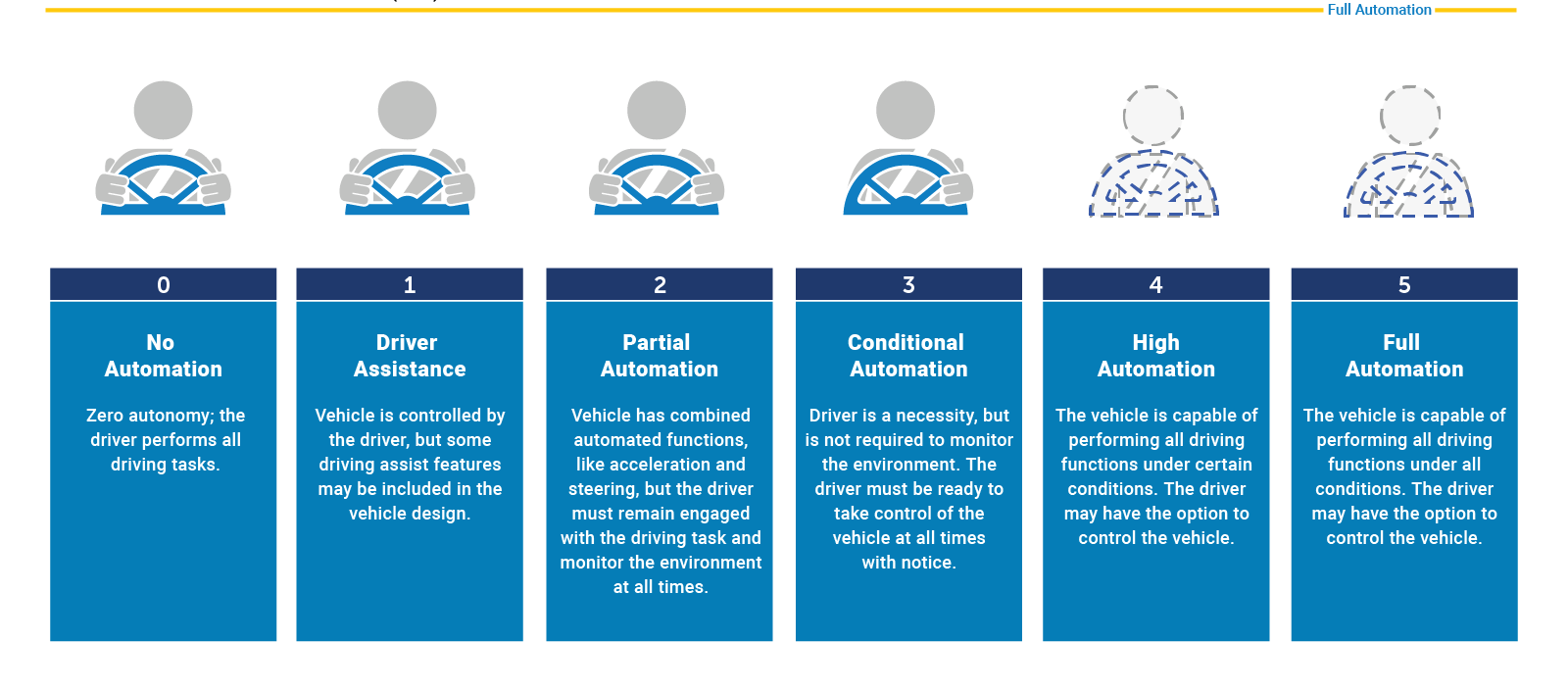

An additional complicating factor that the actuary must consider in determining their approach to evaluating AV liability is the varying levels of autonomy or various driver assistance systems on the market today. In partnership with the International Organization for Standardization (ISO), SAE International developed SAE J306 (SAE International 2021) to provide a taxonomy for six levels of driving automation in the context of motor vehicles and their operation on roadways:

_automation_levels.png)

-

L0 - No Driving Automation: Vehicle features are limited to providing warnings and momentary assistance, such as automatic emergency braking and blind spot warning.

-

L1 - Driver Assistance: Vehicle features provide steering or brake/acceleration support to the human driver, such as lane centering or adaptive cruise control.

-

L2 - Partial Automation: Vehicle features provide steering and brake/acceleration support to the human driver, such as lane centering and adaptive cruise control at the same time.

-

L3 - Conditional Automation: Vehicle features can drive the vehicle under limited conditions and will not operate unless all required conditions are met, such as traffic jam chauffeur.

-

L4 - High Automation: Vehicle features can drive the vehicle under certain conditions and will not operate unless all required conditions are met, such as driverless taxis in certain geofences. Pedals or steering wheels may or may not be installed in such vehicles.

-

L5 - Full Automation: Vehicle features can drive the vehicle under all conditions - everywhere and anytime.

While there is a large number of vehicles with partial autonomy features (L2 and L3) in circulation, these vehicles are often better characterized as vehicles with Advanced Driver Assistance Systems (ADAS), with a human operator required by law to maintain responsibility for the safe operation of the vehicle. While the emergence of partial autonomy ADAS features has presented a challenge for actuaries pricing insurance for these vehicles, there continues to be significant research into and development of methods for incorporating vehicle safety systems like ADAS into the largely human-centered risk evaluation frameworks used to price the required coverage (Baribeau 2019). By contrast, actuarial research is currently light on the methods and approaches needed for the evaluation of truly autonomous vehicles, i.e., those at L4 and L5 levels of autonomy. This paper is a contribution toward addressing this gap in the actuarial toolkit.

In Section 2 of this paper, we will discuss a number of considerations in evaluating the potential liability exposure for autonomous driving and a practical framework for allocating liability following a collision. We will then follow this in Section 3 with an actuarial modeling approach to quantify the potential liability exposures discussed in Section 2. Given the uncertainty in all actuarial models, Section 4 provides an overview of the approach to modeling AV loss distributions, and Section 5 develops a method for credibility weighting the exposure-based pricing approach developed in Section 3 with past experience. Finally, Section 6 concludes with a case study for robotaxis that will be used to illustrate the application of the full methodology.

AVs can be used for many different purposes: from robotaxis to goods delivery. This paper will focus on liability exposure for robotaxis. However, the principles and analytical approaches discussed herein are readily adaptable to other commercial uses of autonomous vehicles, though the actuary must carefully consider the extent to which liability exposure and coverage will vary for each new use case.

2. LIABILITY EXPOSURE AND ASSESSMENT

The development of an on-road liability loss model requires knowledge of what coverage an AV insurance policy provides and assumptions on how frequently Autonomous Vehicles will be held liable for collisions. Autonomous Vehicles operating as part of a commercially owned and operated fleet of robotaxis are exposed to many of the same risks faced by privately owned rideshare vehicles with human drivers. The involvement of an AV in a collision may add some uncertainty to the task of assigning liability given the current lack of legal precedents to inform these analyses.

This section will provide an overview of types of liability exposure and discuss a potential liability framework and some practical considerations relevant to assessing liability.

2.1. Liability Exposure

Despite the expectation that autonomous vehicles will reduce the number of crashes on public roads, on-road accidents are expected to continue to occur in the foreseeable future. AVs could eliminate many human driving errors such as speeding and distracted driving, but also introduce new risks, including software failure or sensor malfunction. When accidents happen, the two most likely outcomes are (i) damage to property; and (ii) bodily injury. From the perspective of insurance coverages that could financially protect the involved parties, it is expected that these will largely mirror and expand on the existing coverages available for traditional vehicles even though the causes of loss may be quite different. For a fleet of robotaxis, below are examples of the types of outcomes for which coverages would offer financial compensation:

In summary, the liability losses for autonomous driving can be modeled with the same coverages as those for commercial or personal auto insurance.

2.2. Liability Framework

Building an actuarial loss model requires an understanding of the liability framework that will apply. For traditional vehicles, actuaries can count on a large number of historical insurance claims, where a well-established legal framework allows for reasonably accurate predictions of liability loss outcomes. The introduction of autonomous vehicles may result in changes to the existing framework, which would have a significant impact on modeling assumptions.

The current automobile liability framework creates a distinction between the driver, who is responsible for operating the vehicle, and the manufacturer, which is responsible for producing the vehicle. If a collision is deemed to be the result of driver error, then driver liability applies; alternatively, if it results from the production or design of the vehicle, then product liability applies. Driver liability is assessed through the lens of negligence, essentially evaluating if parties exercised the duty of care of a reasonable and prudent person, guided by ordinary considerations. Product liability arises if a product is deemed defective or unreasonably dangerous. Such liability can extend to various parties involved in the manufacturing, distribution, or marketing of the product. Product liability claims can be based on negligence or strict liability.

In essence, Autonomous Vehicle technology replaces the role of the human driver, which is to control vehicle maneuvers – deciding how fast it moves, when and how quickly it stops, and steering it. For the purpose of on-road liability loss modeling, it is not unreasonable to assume that the existing negligence framework would evolve to apply to the operation of Autonomous Vehicles, as it has evolved to apply to a range of vehicle innovations in recent history. The tail risk of potentially expensive product liability allegations against autonomous vehicles can be contemplated in modeling the tail of the aggregate loss distribution (Section 4.3).

The evaluation of negligence in collisions involving at least one AV is assumed to be similar to that of collisions involving vehicles operated by human drivers. To the extent that the behavior of the involved parties is deemed to be imprudent, or not reflecting the appropriate level of care required by law given the circumstances, the involved party would be considered at least partially liable for a collision.

The liability framework to be applicable to collisions involving Autonomous Vehicles is a developing topic. Given its importance and materiality in on-road liability loss modeling, it is important for actuaries to remain informed and properly reflect changes in their projections.

2.3. Liability Assessment

Assuming that a negligence framework will apply to collisions involving AVs, the analysis of liability is similar to that of an event involving human drivers only. To derive an expected level of liability assigned to AVs, an evaluation of the behaviors of parties involved in collisions is needed. Such evaluation should rely on a set of considerations, including but likely not limited to the following:

-

Applicable Negligence System: Most jurisdictions in the United States use a comparative negligence system, in which parties are able to recover damages based on their individual share of contribution in a collision. Some jurisdictions use a contributory negligence system, in which parties partially negligent are not able to recover damages.

-

Obedience of Road Rules: Traffic collisions often result from at least one of the involved road users’ failures to obey road rules. When such failure is the proximate cause of a collision, the party who disobeyed rules will likely be negligent and liable.

- For example, if a driver fails to stop at a red traffic light and collides against cross-traffic, they would likely be considered primarily responsible for the collision, absent other contributory factors from the other involved party.

-

Exercise of Prudence: Traffic collisions may arise even when all involved parties follow the rules of the road. In such situations, it is likely that at least one of the parties performed a maneuver that is not considered prudent, in which case they could be considered responsible.

- For example, if a driver is following the vehicle ahead closely, such that they are not able to react to it suddenly stopping, they likely did not exercise sufficient prudence, even where there are no laws determining the distance from the vehicle ahead that a driver should maintain.

The derivation of the aggregate AV liability level for loss modeling purposes could be highly uncertain until statistically credible observations are available. The actuary may consider utilizing observations from AV behaviors in simulated or near-miss collision events to support the estimate of the AV’s accountability and potential liability claim frequency.

3. LOSS MODELING APPROACH

Autonomous Vehicle technology is expected to improve road safety, leading to an overall reduction in the number of collisions on public roads as AVs are programmed to observe speed limits and can never be distracted or impaired. Such expectation is supported by the prevalence of severe injury crashes caused by speeding and distracted or impaired driving (Blincoe et al. 2015).

The objective of this section is to develop an actuarial model of aggregate losses, the total amount paid on all liability claims occurring over an insurance contract period. A collective risk model (Klugman, Panjer, and Willmot 2019) is adopted for this purpose. With this modeling approach, the aggregate losses, are represented as a sum of a random number, of individual losses Hence,

L=S1+S2+⋯+SN,N=0,1,2,…

In this model, individual losses, are assumed to be independent and identically distributed random variables. The assumption of losses being independent could be vulnerable for autonomous driving since in principle, there is only one driver at play here. Further evaluation should be performed with the accumulation of more AV loss experience. In addition, the distribution of does not depend on the value of In other words, the number of losses and the amount of individual losses are independent.

Under these assumptions, the frequency and severity of claims can be modeled separately. The distributions of claim counts and individual losses can be used to inform the aggregate loss distribution. Section 4 will discuss specific distributions for claim counts and loss severities and a simulation approach to obtain the aggregate loss distribution.

3.1. Expected Number of Liability Claims

For financial forecasting and resource planning purposes, actuaries need to help organizations project the number of liability claims for a fleet of AVs operating in various markets. AV companies generally project revenues and expenses based on miles driven.

The number of liability claims can be informed by the safety performance of the AV, one of the most tracked and monitored metrics by AV companies, typically indicated as miles per collision. For a given safety performance target, it is expected that the number of collisions and liability claims increase as miles driven increase, though with the continuous investment of engineering resources in safety performance, this relationship is unlikely to be linear. In general, however, for a fixed period of time, the number of claims, can be expressed as a function of the miles driven, Hence:

N=f(m)

For example, the number of Bodily Injury claims can be projected as:

NBI=m/r∗Pr(IA>0%=1)∗pbi

Where is safety performance target as measured by miles per collision, is the proportion of collisions for which AVs assume non-zero liability, and is the probability of incurring bodily injury given the occurrence of a liability claim. Given that this model is focused on assessing the liability loss in a prospective exposure period, the safety performance target should reflect the expected improvement in safety performance in that period.

A similar approach can be used to project the number of claims for other coverages such as Property Damage liability and Uninsured/Underinsured Motorists’ liability.

3.2. Expected Loss Severities

Again, for financial planning purposes, actuaries will need to project expected loss severities to derive an overall loss amount. The expected loss severity will also help inform the parameterization of loss distribution to be discussed in Section 4.

Until sufficient experience is accumulated for autonomous driving, loss severities can be estimated using insurance industry data (e.g., commercial auto) with adjustments for unique characteristics of the company’s AV operations. Below are some, not necessarily an exhaustive list of, factors that the actuary may consider making adjustments:

-

Speed limit, : Autonomous driving generally has a lower average speed than human driving. As a result, the loss severity should be lower compared to that for commercial auto insurance. According to a study done by Institute for Road Safety Research (SWOV) (SWOV 2004), the probability of injury should reduce in proportion to the square of velocity relativity. Hence, the adjustment factor for velocity can be expressed as Dv=(VAVVCA)2 Where is the average speed of AVs, is the average speed of commercial automobiles.

-

Coverage limit, : AV’s auto liability coverage limit could be different from the coverage limit for commercial auto insurance in a market. DILF=(ILFAVILFCA) Where and are increased limit factors for the AV company in question and industry commercial auto factors, respectively.

-

Vehicle form factor, : The AV’s unique design, weight and additional physical safety features could also differ significantly from the typical vehicle in the industry commercial auto benchmark data.

-

Operational design domain, : The AV generally operates in certain geofences and hours of operation. A higher proportion of rides at night could indicate a higher claim severity, while restricting operations to safer routes and neighborhoods might decrease the claim severity.

-

Number of occupants, : AVs will have varying levels of occupants depending on the use case. Pooled ride-hail rides may have more occupants than a typical commercial auto vehicle does, increasing BI exposure. There will also likely be miles without passengers that will have a lower BI exposure.

-

AV behavior, : Collisions involving impaired and distracted driving generally have higher BI claim severities relative to other causes of collisions (Blincoe et al. 2015). Given that AVs are unable to exhibit these types of behaviors, this may lead to a lower overall severity for AV-liable claims.

The overall adjustment factor for AV is a product of adjustment factors for various AV characteristics:

D=Dv∗DILF∗DVFF∗DODD∗DNOC∗DAVB

Then the AV’s loss severity, can be calculated as

SAV=SCA∗D∗(1+f)

Where is the loss severity for the commercial auto insurance and is an appropriately selected inflation factor to bring the severity to a future exposure period.

To make proper adjustments for AV, actuaries need to have a solid understanding of AV behaviors and operations. Close collaboration with safety professionals, engineers and commercial deployment leaders is imperative for developing such knowledge.

4. LOSS DISTRIBUTION

Organizations with robotaxi or other AV fleets may need to explore risk financing options to transfer or retain risk on their balance sheets. Decisions such as these will depend on the varying risk appetite of the given organization. However, it is crucial for actuaries working at or on behalf of these organizations to develop a view of the distribution of losses to inform these decisions. This will help provide balance sheet stability through adequate pricing and reserving for retained risk and ensure a fair premium value is estimated for negotiations with the insurance market for risk transferred. The following sections provide a proposed simulation-based approach to model the loss distribution.

4.1. Frequency Parameterization

Since AV companies may have limited liability claim data to model claim frequency distribution directly, actuaries can start by modeling the collision frequency, and then model the AV’s liability level for collisions to derive claim frequency. For example, a partially or fully liable collision may give rise to a Bodily Injury or Property Damage liability claim, while a not liable collision may give rise to an Uninsured/Underinsured Motorist liability claim. The following parameters are proposed to estimate AV claim frequency in this section:

-

Collision frequency (4.1)

-

Property damage collision frequency (4.2)

-

Bodily injury collision frequency (4.3)

-

Liability allocation (4.4, 4.5, 4.9)

-

Property Damage claim frequency (4.6, 4.7)

-

Bodily Injury claim frequency (4.8)

-

Non-liable collision frequency (4.10)

-

Uninsured collision frequency (4.11)

-

Underinsured collision frequency (4.12)

-

Uninsured/Underinsured claim frequency

A number of distributions such as Binomial, Negative Binomial, and Poisson, may be suitable for the distribution of collision counts. For simplicity, a Poisson process is utilized here to model collision frequency for a given prospective time period. The probability of an AV fleet with collisions is:

Pr(K=k)=λkce−λck!, for k=0,1,2,3,…

With mean and variance

The Poisson mean for collisions, can be derived from the expected number of collisions based on the projected mileage driven and selected miles per collision rate (see Section 3.1). Depending on the amount of data available, it is possible to select different Poisson parameters for collisions in different operational domains.

Every collision could result in property damage to the parties involved. Thus, the number of collisions with property damage losses, is defined as:

Kpd=K

As not all collisions result in injuries, a bodily injury indicator, can be defined to reflect whether an injury occurs – with referring to a collision with at least one injury and referring to a collision without any injuries. Then is parameterized with a Bernoulli distribution as follows:

Pr(Ibi=1)=pbi and Pr(Ibi=0)=1−pbi

The probability of bodily injury, can be further refined based on the vulnerability to injury of the other parties involved in the collisions. For instance, a collision with pedestrians could have a high probability of injury, close to 100%; while a curb strike could have a low probability of injury, close to 0%. A probability distribution of the other parties involved in collisions would then need to be specified.

The liability allocation for each collision between AVs and other parties (Section 2.3) is modeled to determine the appropriate coverage and liability proportion for a collision. This can be modeled using a continuous distribution to capture various levels of liability or using a multinomial distribution, where liability assigned to AV can be (for the sake of simplicity) either 0%, 50%, or 100%, with a probability assigned to each[1] (as used in this illustration). The number of collisions with liability level is indicated as represents the random variable while represents a realization of the random variable) and each collision has a probability to have liability level where represents the three chosen liability levels, Then, given a total number of collisions, the probability of having and collisions with a respective liability level of 0%, 50%, and 100%, can be modeled as follows:

Pr(A0%=a0% and A50%=a50% and A100%=a100%)=k!a0%!a50%!!a100%!pa0%0%pa50%50%pa100%100%, where k∈{0,1,2,…}p0%+p50%+p100%=1, and a0%+a50%+a100%=k

With mean and variance

The multinomial probability for each liability level, can be projected based on relevant historically observed liability outcomes, prospective operations, and assumed future safety improvements.

The overall liability percentage for a set of collisions, can be obtained by calculating the average liability level across all collisions:

ˉA=1k∑i(i∗Ai), where i∈{0%,50%,100%}

For collisions where the AV is fully or partially liable, liability exposures such as Bodily Injury (BI) and Property Damage (PD) need to be considered. Define an indicator, to determine whether the AV is at least partially liable for a given collision – with referring to a collision with non-zero liability and referring to a collision with 0% liability:

Pr(IA>0%=1)=p50%+p100% and Pr(IA>0%=0)=p0%

The number of PD claims, is then calculated as the product of the total number of collisions with property damage, and the probability of having a collision with non-zero liability, :

NPD=Kpd∗Pr(IA>0%=1)

The number of BI claims, follows a Binomial distribution given PD claims:

Pr(NBI=nBI)=CnPDnBIpnBIbi(1−pbi)nPD−nBI,where nBI∈{0,1,2,…,nPD}and pbi∈[0,1]

With mean and variance

Then the overall liability percentage for a set of claims consisting of only collisions with non-zero liability, can be obtained by calculating the average liability level across the number of partially liable collisions, and the number of fully liable collisions, combined:

ˉAA>0%=1a50%+a100%∑i(i∗Ai), where i∈{50%,100%}

Finally, for collisions where the AV is not liable, there could still be Uninsured or Underinsured Motorist Bodily Injury (UM/UIM BI) exposures. Uninsured or Underinsured Motorist Property Damage (UM/UIM PD) is not considered in this paper. The number of non-liable collisions, is:

KNL=K∗Pr(IA>0%=0)

The number of claims where the third-party drivers are uninsured can be defined using a Binomial distribution, with the probability of a third-party driver being uninsured as given non-liable collisions:

Pr(NUM=nUM)=CkNLnUMpnUMUM(1−pUM)kNL−nUM,where nUM∈{0,1,2,…,kNL}and pUM∈[0,1]

With mean and variance

To model the UIMBI liability exposure, the BI coverage limits that third parties carry need to be considered first, and then compared to the modeled loss amounts to determine the presence of underinsurance for each non-liable collision. The distribution of the number of collisions where the third party is carrying BI out of possible limits can be modeled using a multinomial distribution given non-liable collisions as follows:

Pr(CLimit 1=cLimit 1 and … and CLimit y =cLimit y)=kNL!cLimit 1!…cLimit y!pcLimit …pLimit yLimit 1,where pLimit 1+⋯+pLimit y=1,and cLimit 1+⋯+cLimit y=kNL

With mean and variance

Then the number of UIMBI claims, can then be determined after comparing the loss amount of each non-liable collision, to the BI coverage limit, that the liable parties carry.

The probabilities for encountering uninsured motorists, and underinsured motorists carrying various coverage limits, can be estimated using institutional studies and industry data for AV’s operational domain.

4.2. Severity Parameterization

Claim severity is modeled separately for Property Damage Liability (PD), Bodily Injury (BI), and Uninsured/Underinsured Motorists (UM/UIM). This section describes how the ground-up severity for each claim by coverage is parameterized:

-

Property Damage cost per collision (4.13)

-

Property Damage claim severity (4.14)

-

Per injury cost severity (4.15, 4.16)

-

Liable per injury cost severity (4.17)

-

Number of injuries per collision (4.18)

-

Bodily Injury claim severity

-

UM/UIM BI claim severity

Property damage cost per collision, is assumed to follow a lognormal distribution with a probability density function:

fSpd(spd)=1spdσ√2πexp(−(lnspd−μ)22σ2)

With mean and variance

The PD claim severity, is then calculated by applying the average liability level for collisions with non-zero liability, to the property damage cost per collision, :

fSPD(sPD)=¯AA>0%∗fSpd(spd)

With mean and variance

The lognormal distribution parameters, and can be derived by setting the mean and variance functions of the PD claim severity to the industry’s severity and variance adjusted for company-specific characteristics as shown in (3.7).

Bodily injury cost per collision is modeled with two components: the cost per injury and the number of injuries per collision.

The bodily injury cost per injury can be modeled using a mixed exponential distribution by injury severity level or scale. The Abbreviated Injury Scale (AIS) (Hayes, Erickson, and Power 2007) is selected for this paper to differentiate injury types, but the general methodology can be applied to any scale:

The cost per injury at each AIS injury severity level is assumed to be identical regardless of whether the AV or human is liable. However, the contribution of each AIS level to the overall per-injury severity distribution could be different depending on which party is liable for the collision. Three liable party types are considered here: AV, human (human driver, pedestrian, bicyclist, etc.), and AV/human; corresponding to AV liability levels 100%, 0%, and 50% respectively. The distinct AIS level distribution for different types of liable parties is due to the differences in on-road behaviors between AVs and human road users (Section 3.2).

Each injured party in a collision has a probability to sustain an AIS level injury given liable party type following a Categorical (also known as a Generalized Bernoulli or Multinoulli) distribution:

Pr(AISi∣j)=pAIS,j for i∈{1,2,…,6} andj∈{AV,human,AV/human},where 6∑AISipAISi,j=1

With mean and variance

The probability distribution by AIS level for human-liable collisions can be determined using industry data such as the police-reported crashes, while the probability distribution by AIS level for AV-liable collisions may be developed based on the AV company’s experience or estimated safety improvement targets by AIS level. For AV/human mutually liable collisions, the AIS-level probability distribution may be selected based on the AV company’s experience or a weighted average of AV-liable and human-liable probability distributions by AIS level.

For each AIS level the cost per injury is parameterized with an individual exponential distribution, Exp with probability density function as:

fSAISi(SAISi)=λAISe−λAISisAISi for i∈{1,2,…,σ}

With mean and variance

The exponential parameter, can be derived by setting the mean and variance functions of the cost per injury at AIS level to the industry’s severity and variance at AIS level Exponential parameters can be further adjusted for other factors that may impact future severity (Section 3.2).

The cost per injury distribution given a liable party type, can then be derived by summing the product of each AIS level’s exponential distribution, and its respective conditional probability, :

fSPer Injury ∣j(SPer Injury ∣j)=6∑AIS[pAISi,jfSAISi(sAIS)]=6∑AISi(pAISi,jλAISie−λAISisAISi) for i∈{1,2,…,6} andj∈{AV,human,AV/human},where6∑AISipAISi,j=1

Human-liable collisions are more likely to result in AIS 4+ injuries than AV-liable collisions due to speeding, distracted and/or impaired driving, resulting in a higher average cost per injury than that for AV-liable collisions. However, in the context of AV-human collisions, the average cost per injury for human-liable collisions could be lower due to AV’s potentially greater liability exposure to vulnerable road users such as pedestrians and bicyclists. These vulnerable road users tend to sustain higher-severity injuries when colliding with a motorist (AV in this case). In other words, in the AV company’s interest, AV can be liable for injuries to vulnerable road users and AV passengers while humans can only be liable for injuries to AV passengers who are protected by the physical vehicle during an AV-human collision.

To calculate the BI severity per collision, the number of injuries also needs to be estimated. The total injury count for a collision consists of both the injured AV passengers and third parties. The number of injuries is parameterized with a Zero Truncated Poisson (ZTP) to exclude the outcome of 0 injuries. The ZTP distribution for the number of injuries, can be defined as follows:

Pr(U=u∣U>0)=λuie−λiu!(1−e−λi)=λui(eλi−1)u!, for u=1,2,3,…

With mean and variance

The ZTP mean for the number of injuries, can be derived based on the company’s expected mix of operation modes and the industry data. For example, monetized rides have passengers while empty rides do not. The number of third-party injuries can be estimated from industry data such as police-reported car crashes.

By summing up the cost per injury across all injuries and applying the liability allocation, the ground-up claim severity for BI and UMBI can be obtained. For UIMBI ground-up claim severity, the amount of the non-liable loss severity over the third party’s BI limit (4.12) needs to be further quantified.

4.3. Aggregate Loss Distribution

Given the complexity of frequency and severity distributions assumed above, an analytical distribution for the aggregate losses cannot be easily derived. Instead, a Monte Carlo simulation is employed to simulate all the frequency and severity components to create the aggregate distribution of ground-up losses. The following coverages to the underlying losses are simulated in the process:

-

Property Damage Liability

-

Bodily Injury

-

Uninsured/Underinsured Motorist Bodily Injury (UM/UIM BI)

Using a programming language like Python or R, the following steps can be executed:

-

Simulate the number of collisions using the Poisson frequency distribution (4.1).

-

Simulate the AV’s liability for each collision - 100%, 50%, or 0% (4.4).

-

For all collisions, simulate the property damage loss amount using the lognormal distribution (4.13) and apply the simulated liability level from Step 2 to obtain the PD loss amount.

-

Simulate whether the collision involves at least one injury (4.3).

-

Simulate the number of injuries for each collision involving injuries (4.18).

-

For each injury, simulate the AIS level from the AIS-level injury distribution depending on the liable party type - AV, human, or AV/human (4.15). The cost per injury is then simulated using the severity distribution by AIS level (4.16).

-

The loss amount for a BI claim is then calculated by summing up the costs for all injuries and applying the simulated liability level for the collision from Step 2.

-

Simulate whether the other parties are adequately insured, uninsured (4.11), or underinsured (4.12).

-

The loss amount for an UM/UIM BI claim is then the uninsured/underinsured loss amount calculated as the non-liable loss amount over the other parties’ simulated BI limit.

-

For each simulated claim, aggregate losses across all coverages (PD, BI, and UM/UIM BI), to calculate the loss per occurrence.

-

For all simulated liability claims, sum up the loss per occurrence to obtain the aggregate losses.

-

Repeat steps 1-11 number of times for each prospective period and apply the selected inflation factor. is the number of simulations chosen by the user. A larger would produce estimations that match more closely with the theoretical distributions.

4.4. Risk Measures

Once the loss per occurrence and aggregate loss distributions are established, key risk measures can be derived to inform financing decisions. Here are a few examples:

-

Volatility of cash flows with and without risk transfer. Measures such as Value-at-Risk (VaR), Tail-Value-at-Risk (TVaR), and standard deviation can be used to show the level of volatility to key organizational stakeholders.

-

Per occurrence loss costs - Depending on the organization’s strategy, this can inform the decision to retain or transfer liability exposures to varying extents.

-

Aggregate stop-loss - The organization may wish to cap the overall exposure to loss and the distribution can help inform the cost around this.

-

Risk Load - The risk load will generally be a large component of any excess layer premium. The volatility in the aggregate loss distribution can be a key influencer of the magnitude of the risk load to the expected losses in the layer.

5. DETERMINING THE CREDIBILITY OF PRIOR EXPERIENCE

Traditional automobile insurance pricing models rely on a combination of claims experience and a priori estimates to develop a prospective view of frequency and severity. This is achieved through credibility theory, which defines standards for the volume of historical observations needed to enable full reliance on a dataset for predictions of future outcomes. To the extent that the historical observations are not fully credible, the actuary selects an a priori estimate to complement the prediction.

The use of credibility theory relies on the premise that historical performance is predictive of the future. It basically assumes that driving behaviors of the past will persist into the future. Projections can then be adjusted to account for technological advancements, such as driver assistance systems, and general and social inflation, to reflect expected changes in frequency and severity, respectively. This can be reliably achieved through exponential trend selections, for example, as changes in traditional vehicle fleets take place gradually over time and inflation can be measured using macroeconomic indicators.

Autonomous vehicles have seen rapid technological advancements over a short period of time. A collision involving an AV a few months ago may no longer be expected, due to both hardware and software improvements. At the current state of AV development, in which rapid month-over-month safety improvement is the norm, historical claims frequencies may carry weak predictive power and could lead to overestimations of future claim counts. The phenomenon is similar on the severity side, as autonomous vehicles become more effective at attenuating the impacts of collisions that cannot be avoided. The resulting frequency and severity distributions must be carefully considered in developing a credibility standard.

In this section, we will examine two prevalent credibility standards in Commercial Auto Liability and propose an enhanced approach for the projection of on-road liability losses for AVs.

5.1. Classical Credibility

Classical credibility is widely utilized in automobile liability ratemaking. The number of claims required for full credibility can be obtained by solving the following equation for :

P=2√2π∫k′√μ0e−x22dx

Selections for and are made arbitrarily, although and are typical in automobile liability, resulting in a full credibility standard of This approach, however, has two important shortcomings:

-

It develops a credibility standard for claims frequency and is applied, in practice, to pure premium estimation. As a result, it does not reflect the volatility in severity in the resulting number of claims required for full credibility.

-

Specifically for Autonomous Vehicles, frequencies, and severities are expected to change over time, due to the rapid improvement of the technology. As a result, observations of historical losses may warrant a lower weight than the credibility standard would typically suggest, provided the actuary can substantiate evidence of significant safety improvement.

A potential solution to the aforementioned shortcomings would be to simply select and differently, which could yield a wide range of alternative full credibility standards. However, a method that could provide theoretical support for a standard that adapts to future distributions of frequencies and severities is more desirable.

5.2. Mayerson, Jones, and Bowers Formula

Mayerson, Jones, and Bowers (Mayerson, Jones, and Bowers 1968) proposed a full credibility standard that reflects the underlying severity distribution. The number of claims required for full credibility is described by the following equation, assuming that frequency follows a Poisson distribution:

k′λ=ze⋅√λ⋅√1+μ2μ2+z2e−16⋅1+3⋅μ2μ2+μ3μ31+μ2μ2

Where:

-

is equivalent to the definition in the Classical Credibility equation;

-

represents the percentile of the standard normal distribution for a given

-

represent the first three moments of the observed severity distribution.

Similarly, to the Classical Credibility equation, it depends on parameters and with the result that the observed pure premium should be within of the expected pure premium with probability

Liability books with greater severity skewness will require a larger number of claims for full credibility, which is more adequate than employing a method purely based on frequencies when utilizing the methodology to project pure premiums. The downside of the method is that a larger number of observations is required to reach the standard for full credibility. While a credible database of historical claims for AVs is not yet available, the existing Commercial Auto Liability experience is the best available proxy for this measure and is readily available through insurance industry aggregators in the United States.

Mayerson, Jones, and Bowers provide an example where and where the number of claims required for full credibility is which is substantially larger than the 1,084 claims required based on the Classical Credibility standard. While we believe that the formula is more adequate to establish a full credibility standard for AVs, as it incorporates the volatility inherent to severity distributions, it does not sufficiently address the rapid change in frequency and severity distributions expected for a book of AV claims. As a result, further adjustments are required to address the issue for Autonomous Vehicles.

5.3. Adjustment of Credibility for Autonomous Driving

In the projection of the on-road liability loss for a prospective policy period, it is typical to employ a combination of historical loss observations and a priori loss estimates, with the objective of credibility weighting pure premium projected by the two sources. As AV technology continues to improve significantly in the avoidance of collisions, historical claims data should have reduced influence over predictions, which can be accomplished through the adoption of a decay factor, applied to the credibility standard derived using the Mayerson, Jones, and Bowers formula.

The decay factor applies a reduction to the credibility level assigned to historical claims and depends on the expected level of safety improvement of autonomous driving. The faster the improvement, the greater the decay factor. For a given decay factor, the further apart the historical experience and the projection are, the less credible the historical experience will be. In addition, the application of the decay function would ensure that the historical experience would never reach 100% credibility, which is reasonable in a period of rapid safety improvement. The adjusted credibility weight assigned to historical pure premiums is derived as follows:

CRAV=CRCA ∗ e−bt

Where is the credibility developed for commercial auto insurance, is the credibility for autonomous driving, is an exponential decay constant (where and is the time in years between the midpoint of historical experience and the midpoint of the projection period.

For example, with three selected exponential decay constants, the relationships between the exponential decay factors and time, can be illustrated below:

From the graph above, observe the time it takes to reach 50% decay factor (green dotted line) decreases exponentially as the exponential decay constant increases. In other words, with a larger exponential decay constant, a larger discount would be applied to the credibility of past experiences, arguably justified by a strong belief in the accelerating pace of safety improvements.

6. CASE STUDY

To illustrate the methodology discussed above, the following case study with simplified assumptions is executed.

Suppose actuaries want to derive the credibility-weighted prospective ground-up Bodily Injury liability losses per mile as well as the aggregate BI loss distribution in 2023 using limited historical data for a fictitious company called Fictitious Autonomous Vehicle Company (FAV) that operates robotaxis in the state of New York only. FAV has been operating its robotaxis since 1/1/2021 and has data available as of 6/30/2022. For the upcoming year of 2023, FAV plans to drive 125 million autonomous ride-hailing miles in New York.

6.1. Assumptions

Based on FAV’s historical robotaxi performance as of 6/30/2022 and relevant industry data adjusted for company-specific operations (Section 3), FAV’s actuarial and engineering teams have agreed on the following assumptions for 2023 ride-hailing in New York:

-

FAV expects a collision for every 100,000 ride-hailing miles driven.

-

FAV is expected to be liable for 40% of all collisions. The liability level (0%, 50%, and 100%) is parameterized with a multinomial distribution based on observation of FAV’s most recent near-miss and simulation data: A ∼ Multinomial(k,p0%=0.4,p50%=0.4,p100%=0.2) where represents the expected number of collisions.

-

It is assumed that only 20% of collisions are expected to result in injuries. The injury probability is parameterized with a Bernoulli distribution:

-

For any given collision with injury, the number of injured parties is parameterized with zero-truncated Poisson distribution with

-

The expected per injury ground-up losses based on the liable party type where {AV - AV 100% liable; human - AV is 0% liable; AV/human - joint 50% liability} with company-specific adjustments is parameterized with separate exponential distributions as follows:

-

-

-

For simplicity, all injured parties in a claim are assumed to have the same cost per injury.

-

-

From 1/1/2021 to 6/30/2022, FAV has experienced 200 BI claims with an estimated trended ultimate BI ground-up loss cost per mile of $0.15. FAV’s actuarial team has decided to use the Mayerson, Jones, and Bowers Formula with the same parameters given in Section 5.2 to arrive at the full Commercial Auto credibility standard of 4,713 claims. They have also decided to apply an exponential decay factor approach (Section 5.3) with an exponential decay constant of 0.2 to derive the credibility for Autonomous Driving.

-

for full Commercial Auto credibility standard

-

Historical BI Losses per Mile = $ 0.15

-

Historical BI Claims Count

-

for exponential decay

-

6.2. Calculation of Expected Losses

Formulas and variables outlined in Section 3 and Section 4 are utilized to complete the following calculations in order to derive FAV’s expected ground-up Bodily Injury on-road liability losses in 2023 for ride-hailing in New York.

(3.3) can be broken down into three pieces to calculate the expected number of Bodily Injury Claims:

- The expected number of collisions in 2023 can be derived by dividing the planned mileage by the miles per collision:

E[K]=mr=125,000,000100,000=1,250

- The expected number of PD claims can be calculated by multiplying the expected number of collisions by the expected proportion of collisions with non-zero liability as:

Pr(IA>0%=1)=p50%+p100%=0.4+0.2=0.6E[NPD]=E[K]∗Pr(IA>0%=1)=1,250∗0.6=750

- Out of these 750 expected PD claims, 20% of the claims are expected to be associated with a Bodily Injury claim:

E[NBI]=E[NPD]∗Pr(Ibi=1)=750∗20%=150

For each BI claim, calculate the expected number of injured parties by taking the expected value of the zero-truncated Poisson with per (4.18):

E[U]=11−e−1≈1.582

The expected BI claim severity is therefore calculated by multiplying the expected number of injuries by the liability level, probability of having the liability outcome given non-zero liability and the cost per injury given the liable party, as follows:

E[SBI]=E[U]∗{100%∗p100%/Pr(IA>0%=1)∗E[SPer Injury ∣AV]+50%∗p50%/Pr(IA>0%=1)∗E[SPer Injury ∣AV/ human ]}=1.582∗[100%∗0.2/0.6∗$175,000+50%∗0.4/0.6∗$150,000]≈$171,381

Multiply the expected number of BI claims by the expected BI claim severity to obtain the aggregate ground-up BI on-road liability losses in 2023:

E[BI Losses ]=E[NBI]∗E[SBI]=150∗$171,381≈$25,707,121

Finally, the expected ground-up Bodily Injury on-road liability losses per mile driven in 2023 can be calculated as:

E[BI Losses per Mile]=E[BI Losses]/m=$25,707,121/125,000,000≈$0.21

6.3. Simulation Results

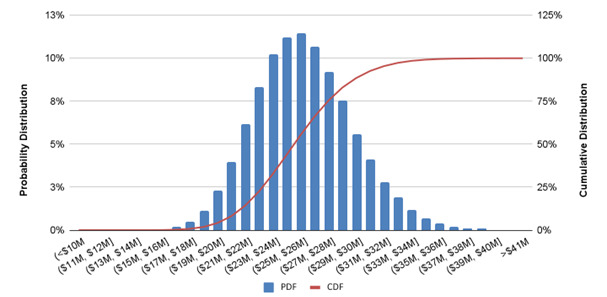

Below is the distribution of Bodily Injury ground-up losses in 2023 from 100,000 simulations done in Python:

Selected summary statistics for the simulated aggregate distribution are:

With 100,000 simulations, note that the sample averages of the simulated distribution match the expected values of the population distributions very closely, providing a reasonable estimate of the spread of population distributions.

Also with the simulated loss distribution, the spread of the aggregate losses and the exceedance probabilities at various loss amounts can be easily estimated. Additional analyses can then use the simulation results to price by layers as well as inform reserve decisions.

6.4. Credibility Calculation for Autonomous Driving

Given the full Commercial Auto credibility standard of 4,713 claims using the Mayerson, Jones, and Bowers Formula (Section 5.2), the Commercial Auto credibility for the historical period from 1/1/2021 to 6/30/2022 with 200 BI claims can be obtained:

CRCA=√2004,713≈20.6%

The exponential decay factor applied to the credibility for Commercial Auto, with an exponential decay constant, can be calculated per (5.3) as:

e−bt=e−0.2∗1.75≈0.7047

Where is calculated as the time in years between 10/1/2021, the midpoint of historical experience (1/1/2021-6/30/2022), and 7/1/2023, the midpoint of the projection period (1/1/2023-12/31/2023).

Then, calculate the credibility of historical experience suited for Autonomous Driving, as follows:

CRAV=CRCA∗e−bt=20.6%∗0.7047≈14.5%

Finally, calculate the expected credibility-weighted prospective ground-up Bodily Injury on-road liability losses per mile driven in 2023 as:

E[ Credibility Weighted BI Losses per Mile ]=CRAV∗ Historical BI Losses per Mile +(1−CRAV)∗E[BI Losses per Mile ]=14.5%∗$0.15+(1−14.5%)∗$0.21≈$0.20

This exponential decay credibility approach offers a balance between the relevance of the historical data and sensitivity of the prospective rate with safety improvements in mind to come up with an indicated rate per mile for AV operations.

6.5. Further Considerations

This case study above has simplified most of the assumptions in order to illustrate the methodology more efficiently. In practice, further considerations may include:

-

Conducting the analysis using shorter time periods. For example, instead of projecting the exposure on a yearly basis, actuaries could project on a quarterly or monthly basis. Some benefits include allowing the flexibility to project safety improvements across shorter periods of time and deriving insights on a more granular level to more closely track management decisions on operations.

-

Setting a miles per collision rate, for each operational domain. For example, operations in a denser city environment (and/or a more complex driving environment, or with significantly skewed age distributions of road users - e.g., college towns or retirement communities and other location-specific factors of relevance to the difficulty of the driving task) may have a higher frequency than in a suburban or rural environment. This distinction will help further distinguish the inherent differences in frequency exposures across operational domains.

-

Varying the liability distribution by severity levels (i.e., AIS levels). For example, since AVs are more attentive “drivers” than humans, perhaps AVs are less likely to be fully liable for minor collisions, such as a fender-bender rear-ending collision. Recognizing this variation may inform the company’s prioritization of engineering efforts on which types of performance to focus on for future safety improvements.

-

Using a continuous distribution to model the liability levels as opposed to a discrete distribution. This paper used only 3 liability levels (0%, 50%, 100%) for simplicity. In practice, one can be found anywhere between 0% and 100% liable and a continuous distribution would more accurately reflect the liability allocation.

-

Varying the probability of injury by collision types. For example, the injury probability for a head-on collision could be higher than that of a side-swipe collision. This variation will more accurately reflect the claim severity by different collision types, resulting in a more precise model.

-

Further defining the number of injuries by operation modes. For example, a shared/pooled ride may have a higher occupancy than an unshared ride during ride-hailing operations, thus a higher number of injuries in shared/pooled rides is expected, given a sufficiently severe collision. This segmentation will more accurately inform the company about its risk exposure with different operation modes.

-

Varying the per-injury loss by severity level. For example, a fatal collision should have a significantly higher cost per injury than an AIS-1 minor collision. This will result in a heavier right-tail and higher variance in the modeled aggregate distribution, thus reflecting the on-road BI and UM/UIM BI exposures more accurately.

-

Using a claim or miles-driven volume-weighted average accident date instead of the midpoint of the historical period/prospective period for the exponential decay factor calculation. As an AV company might be rapidly growing and driving more miles later in the year, using a claim or miles-driven volume-weighted average accident date can more accurately reflect the time difference to determine relevance, resulting in higher credibility applied to the historical period data if the historical experience is disproportionally made up of data collected during the latter half of the period.

7. SUMMARY

This paper provided an overview of liability exposure for autonomous driving and an actuarial modeling framework to assess major elements of potential AV liability losses. Given the limited experience available for autonomous driving, the authors suggested a pragmatic approach to project claim frequency and loss severity based on safety performance analytics and commercial auto insurance experience. In addition, viable distribution functions for key components in the calculation of aggregate losses such as the number of collisions, liability allocation, cost per injury, and the number of injuries are explored in this paper.

Many of the assumptions and approaches discussed in this paper will be subject to change as more data becomes available and regulatory and legal environments evolve around autonomous driving. Actuaries who practice in the AV industry need to develop deep knowledge of how the AV’s behavior changes with the evolution of AV technologies and assess how AV behaviors affect claim frequency and loss severity. Close collaboration with safety professionals and AV engineers is essential for actuaries to develop credible loss projections. Lastly, beyond the assessment of on-road liability exposure, it is plausible for actuaries to significantly impact their company’s strategy and operational excellence by developing and sharing insights into the correlation between AV behaviors, loss potential and other elements of operational relevance for any commercial AV company.

It is the authors’ hope that this paper will shed some light on major challenges actuaries at AV companies are facing and will generate more discussions among the actuarial community about how to quantify and manage on-road liability exposure as autonomous driving becomes more prevalent on public roads.

Biographies of the Authors

Tetteh Otuteye is Vice President of Risk Management at Cruise.

Corey Rousseau is Actuary Partner at Cruise.

Rafael Costa is Actuary Partner at Cruise.

Jiayi Huang is Sr. Actuarial Analyst at Cruise.

John Xu is Director of Actuarial & Risk Analytics at Cruise.

The selected probabilities can be derived from the analyses of the AV’s relative contribution in actual collisions and near misses using the framework as outlined in Section 2.3.

In the context of AV-human joint liability collisions, due to the AV’s lower expected contribution to low-severity events, the average conditional per injury severity given AV liability exposure is likely to shift upwards compared to the average conditional per injury severity given human liability exposure (Section 4.2) - though the aggregate effect here is an expected reduction in total expected liability for AVs due to the expected lower frequency of AV liability claims given the AV’s expected safety performance. The numbers here are for illustrative purposes only. The actuary will need to estimate these herself and verify empirically over time.