Introduction

How does one determine if their actuarial department, specifically the reserving department, is best in class? An assessment of an actuarial reserving department can be obtained by an internal or external independent review of the department. In order to determine a reserving department’s effectiveness and if the department is meeting best in class practices, the review may include:

-

Appropriate Size and Structure

-

How should the department be structured?

-

Is the department appropriately staffed?

-

-

Efficiency

-

Is there sufficient governance and internal control around the various reserving processes (data, analysis, reporting, etc.) to provide reliability and to meet regulatory and audit requirements?

-

Are the appropriate early warning tests in place to highlight changing trends?

-

Are processes efficient?

i. Are too many tasks done manually?

ii. Is outdated software used?

-

-

Communication

-

Is sufficient conversation and knowledge transfer occurring between the actuarial department and other key departments (e.g., claims and underwriting) to inform the reserving process?

-

Are senior leaders and other business leaders receiving the information needed to make good decisions?

-

Are information, analyses and conclusions communicated in a way that both actuaries and non-actuaries can understand and take action on?

-

Is uncertainty of results and specific assumptions communicated effectively?

-

-

Adaptability

-

How are actuarial methods responding to the changing environment?

-

Are the actuarial leaders developing the appropriate new skills to effectively manage, especially in our ever-changing pandemic environment?

-

Does the actuarial team have the right skillsets to meet the evolving needs?

-

This paper provides examples of best practices with regard to many of the above points.

Background on Expertise and Industry Survey

Many of the observations and conclusions for best practices are based on the authors’ significant industry experience spanning several decades as well as the results of surveys periodically conducted by Milliman, Inc. (Milliman).

In order to provide benchmarks to evaluate how one company compares to other companies, Milliman periodically surveys insurance companies on their reserving departments and practices. Milliman conducted a survey in 2012 and subsequently in 2020. The survey results provide an overview of how reserving departments in property and casualty insurance companies are structured. It also surveys their overall concerns. The results of the survey helped the authors determine some specific areas to address regarding best practices.

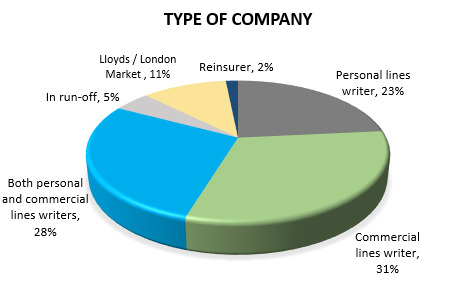

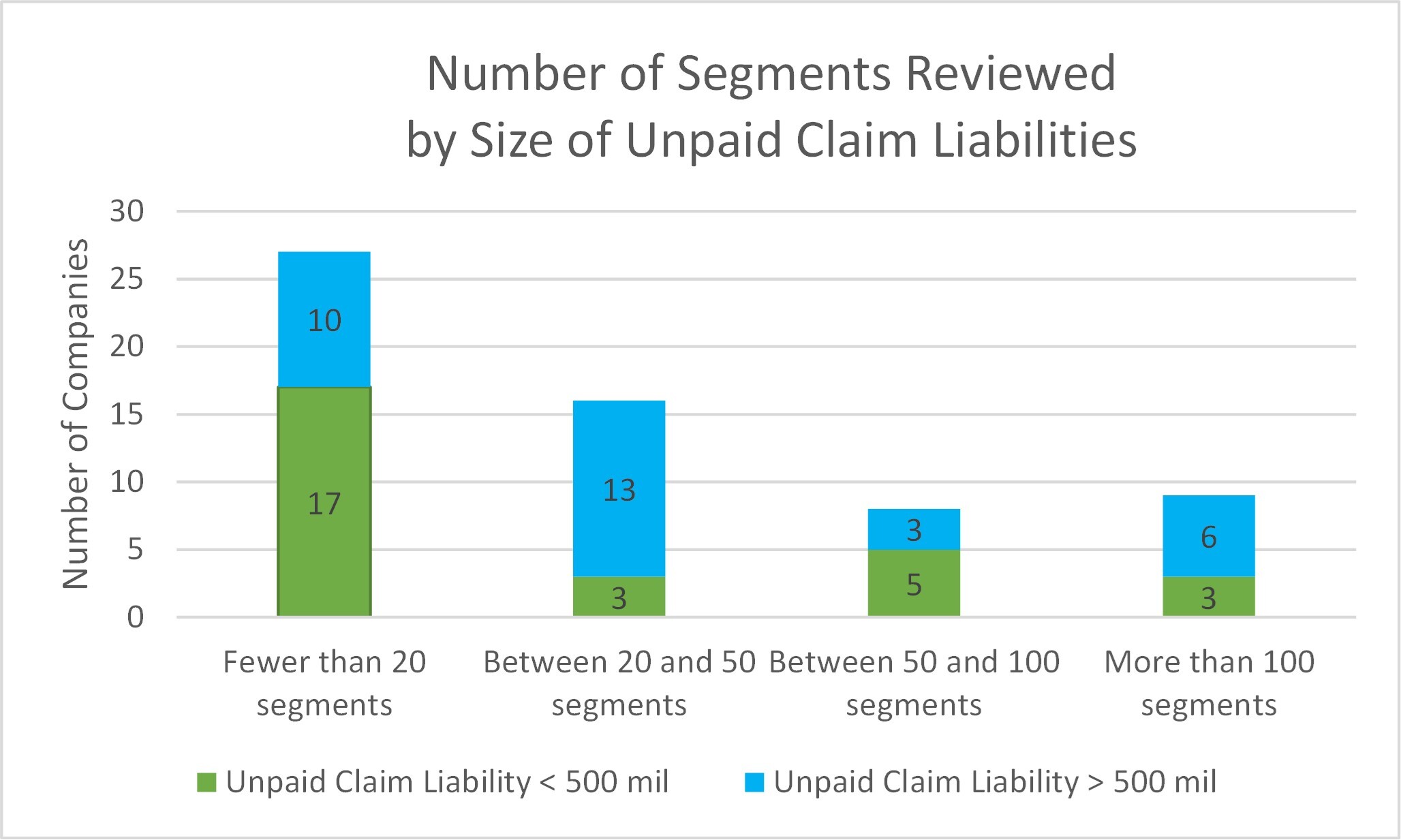

In total, 64 companies responded to the 2020 survey. One should note that not all companies responded to each question. In order to provide meaningful benchmarks, when appropriate, the results were separated by size of insurance company (based on size of unpaid claim liabilities) and type of insurance company (e.g., personal writer, commercial, both, or reinsurer). With regard to size of liabilities, 45% (29 companies) reported unpaid claim liabilities below $500 million and 55% (35 companies) reported unpaid claim liabilities above $500 million. Figure 1 summarizes the types of companies that responded to the surveys.

Appropriate Structure and Size of Reserving Departments

A key question regarding an organization is to ask about the staffing of various departments.

-

How should the departments be structured?

-

Is the department appropriately staffed?

Structure

Insurance companies have wrestled with the concept of how to structure their reserving teams for years. The two main questions that often arise are:

-

Should the reserving and pricing teams be combined or separate?

-

Should the actuaries be centrally located or decentralized?

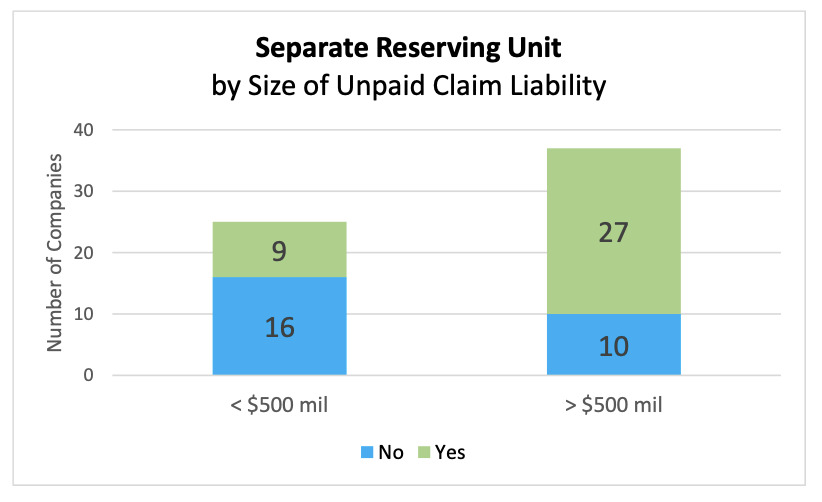

There are advantages and disadvantages for each option. There is not a clear “best practice” based solely on the structure. When we conducted our reserving survey in 2020, approximately 60% of the companies that responded had separate reserving and pricing units. This distribution was similar to the results of our 2012 reserving survey.

Not surprisingly, the size of a company is a key component for determining if reserving and pricing teams are separate. Thirty-six percent of the companies with unpaid claim liabilities below $500 million had separate pricing and reserving units, while almost 80% of the companies with unpaid claim liabilities above $500 million had separate pricing and reserving units.

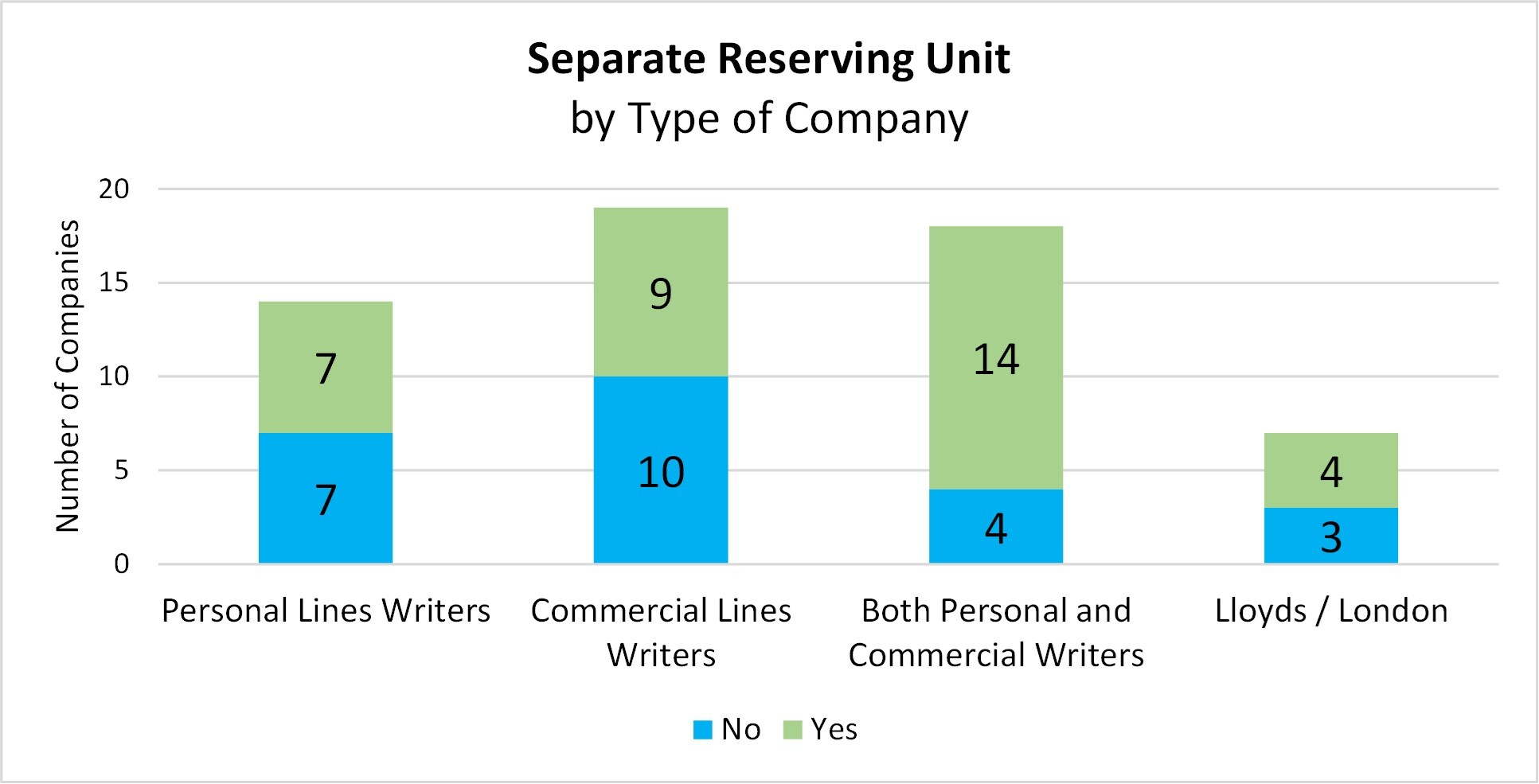

Size is not the only criterion for having separate pricing and reserving units. The complexity of the business is also a key consideration. Reinsurance companies and companies with both personal and commercial business tend to be more complex; therefore, they tend to have separate pricing and reserving units (see Figure 2). Companies also tend to have separate units if insurance is offered across multiple countries, as well as when the companies have multiple operating units (see Figure 3).

Over the course of more than 30 years, companies have moved actuaries from a centralized location to decentralized locations (whether that be in regional offices or within business units in a central main office) and back again to a centralized location. The results of our 2020 survey indicate that companies with separate reserving units currently tend to have centralized functions in a central location.

Advantages of a centralized location are that the actuaries can:

-

Have a consistent approach (whether it be in pricing, reserving, or advising business units on operations).

-

Optimize learning (tools/exhibits/key indicators) can more easily be shared within the actuarial team).

-

Seize process efficiencies gained by centralizing tasks such as data management, including both data input and output, and template management (e.g., rollforward analysis templates). These tasks can be performed by a few people so that analysts can focus their time on the actuarial analysis.

-

Mitigate risk when staff turnover occurs.

-

Be managed more efficiently under the chief actuary.

The disadvantages of actuaries in a centralized location include:

-

Potentially more difficult to communicate with other departments or business units which are decentralized.

-

Governance and uniform processes take precedence over agility.

The primary advantage of a decentralized location is that the actuaries can more easily interact and communicate with non-actuaries in other business units when located within or near the business units. This communication is necessary because:

-

Actuarial concepts can be complex and having the actuary be part of a business unit may help encourage education, communication, and understanding of the drivers of the insurance operations.

-

First-hand knowledge of changes in the operations can be ascertained.

-

Better pricing, risk selection and reserving may be achieved, which results in overall better business operations. This is especially true when rates and terms and conditions are changing rapidly.

Companies that choose a decentralized actuarial structure may find that they need more of an analytical focus in other areas of the company. Experienced actuaries can provide the needed analytical process and support. For example, an actuary in the claims unit could help develop and monitor key indicators and communicate changes in the claims process to other reserving actuaries. Sixteen percent of the survey respondents had a dedicated claims actuary.

The disadvantages of actuaries in a decentralized location include:

-

Greater difficulty in training the actuaries or sharing knowledge between the actuaries.

-

Challenges with maintaining a rotational program across units and/or locations.

-

The potential of a compromised or less independent view of the business due to pressure from business unit or regional management.

-

More complicated reporting relationships (the actuaries might have multiple customers/ bosses with the chief actuary being just one of them).

There is no optimal way or best practice to structure an actuarial department that works for all companies. It is important to incorporate a structure that meets the needs of an individual company while realizing the challenges with the selected structure.

Size

Just as there is no optimal way to structure an actuarial department that works for all companies, there is also no simplistic formula that dictates how many actuaries should be employed in the reserving unit.

Most of the companies surveyed (60%) have under 5 people in the reserving department. The smaller the unpaid claim liabilities, the smaller the size of the reserving department. But the size of the unpaid claim liabilities is not the only criterion for determining the optimal size of a reserving department. Other considerations include:

-

Frequency of analyses (monthly, quarterly, annually).

-

Number of segments reviewed.

-

Use of reserving software (whether it be homegrown or vendor provided).

-

Automation in retrieving reserving data.

-

Complexity of the reserve analyses.

-

Regulatory requirements.

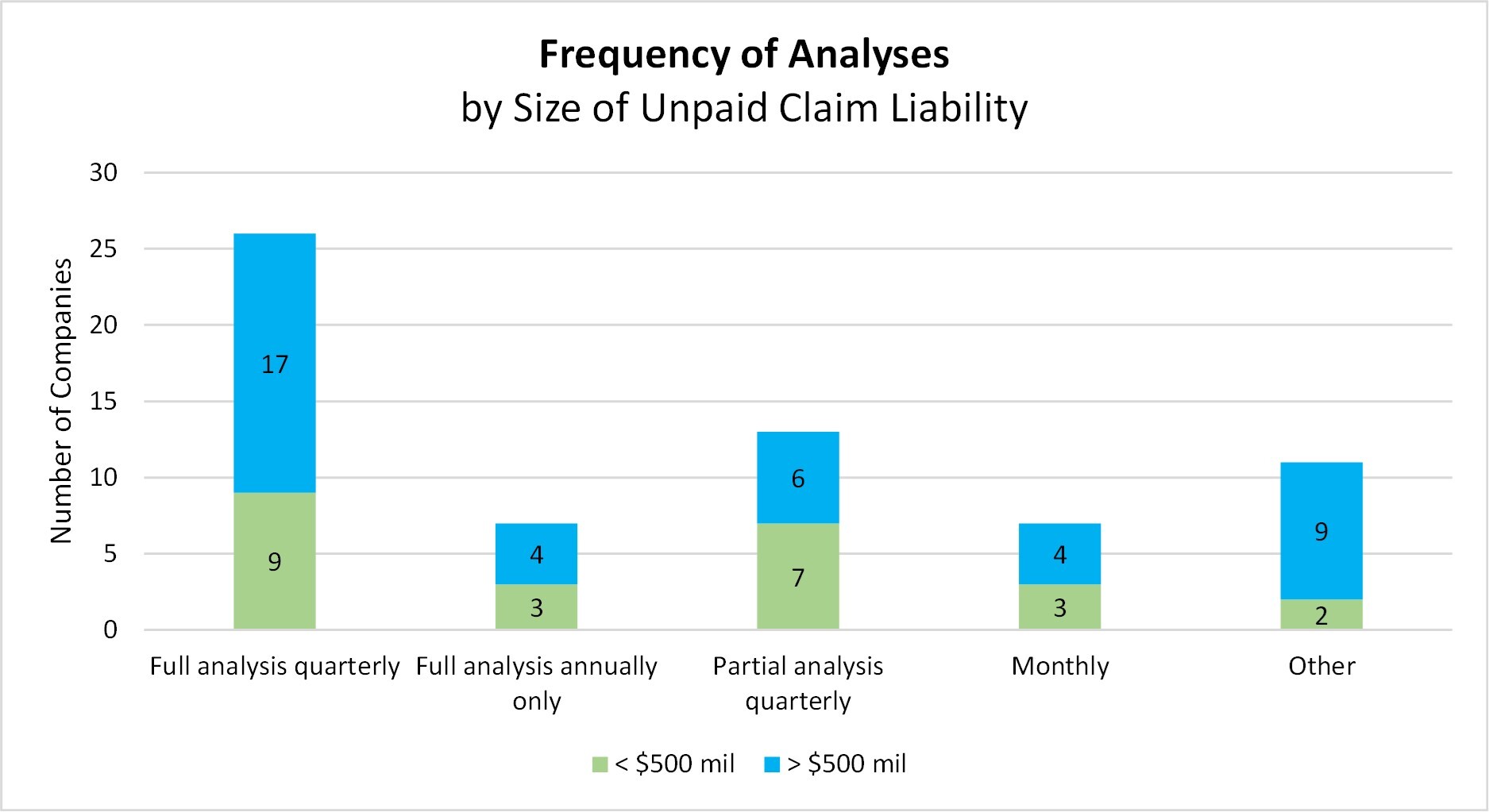

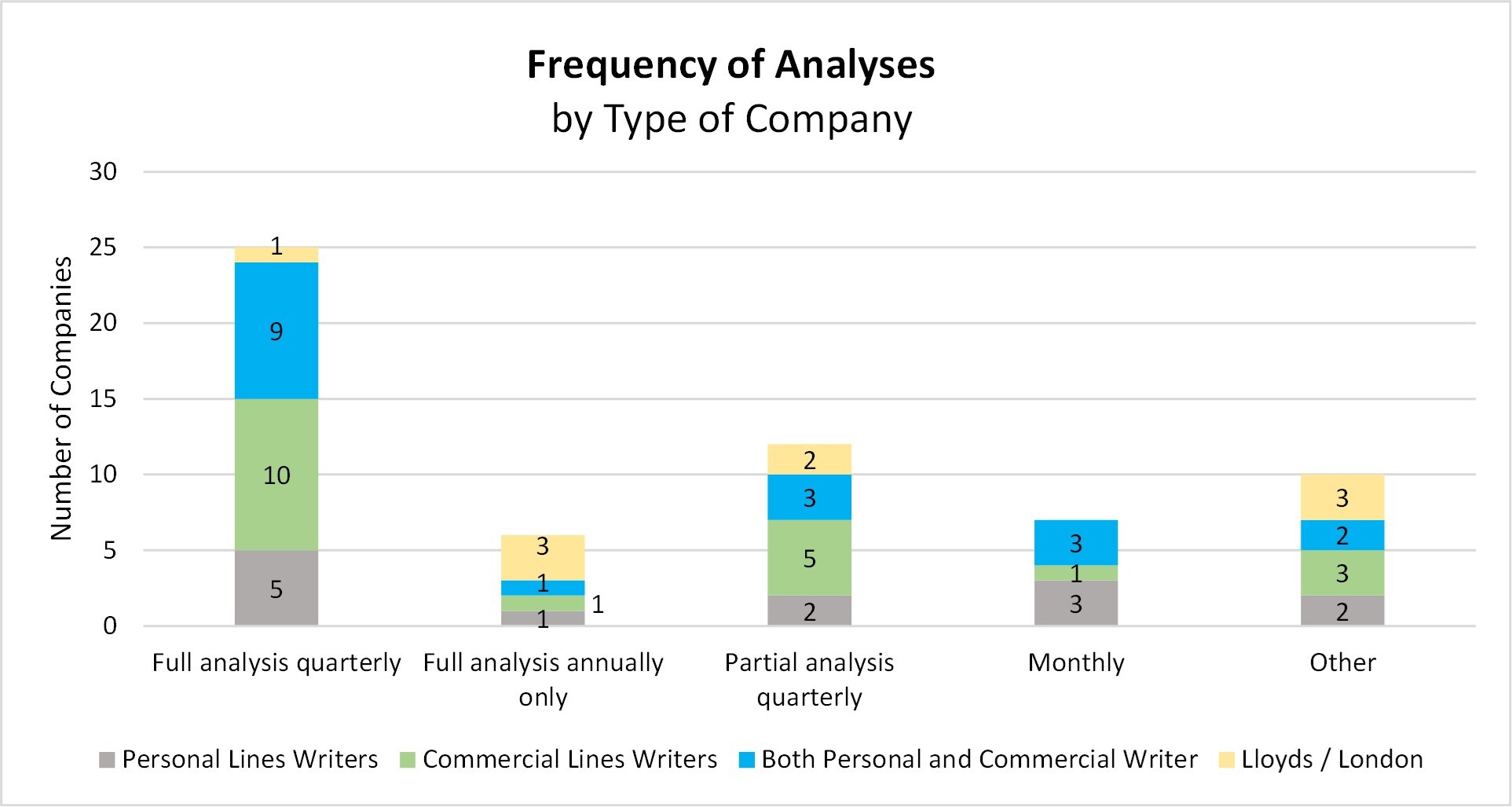

Most companies surveyed (60%) perform a full analysis quarterly or partial analysis quarterly (full analysis of some business segments and roll-forward analysis on other segments). Twelve percent of the companies performed semi-annual or tri-annual reviews. Ten percent of the companies performed only an annual analysis and 10% performed monthly analyses.

As shown in Figures 4 and 5, the size or type of company was not a key reason in determining the number of unpaid claim liability reviews.

Not surprisingly, the number of segments reviewed was correlated with the size of the unpaid claim liabilities. Segmentation is largely based on homogeneity and credibility of the data. Therefore, the larger the size of the unpaid claim liabilities, the more segments the data could be separated into while maintaining credibility. Generally, the more segments reviewed, the larger the reserving staff (see Figure 6).

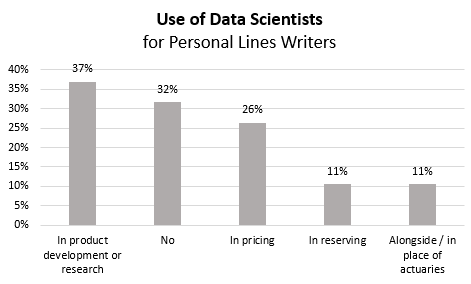

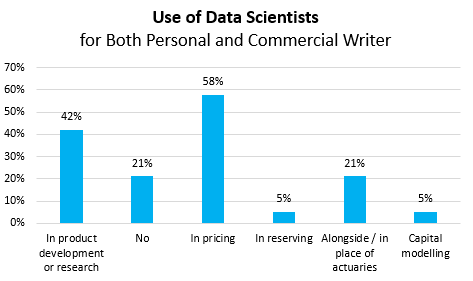

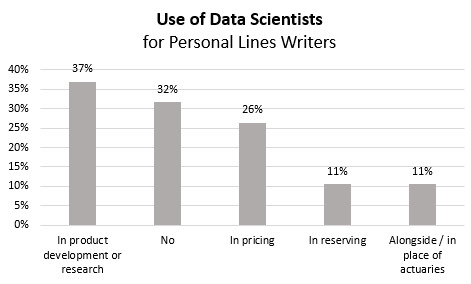

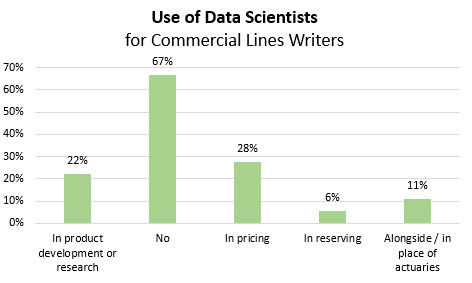

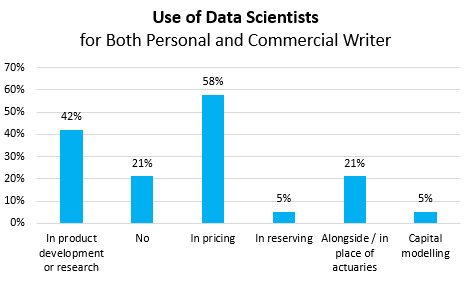

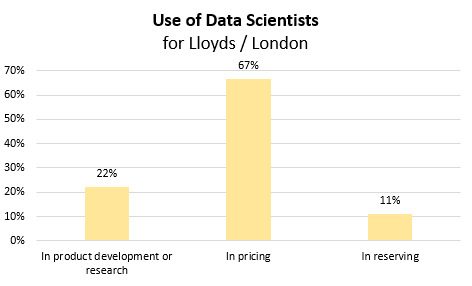

Data Scientists

One way in which insurance companies are trying to adapt to changes in the insurance market and be proactive is by hiring more data scientists in addition to traditional actuaries. Within actuarial departments, data scientists typically work on product development, research, and pricing, but currently rarely work in reserving (see Figures 7-10).

The actuarial function can be enhanced by adding data scientists to the team. By using machine learning or automated intelligence, data scientists may be able to identify patterns that the actuarial staff may not have been able to readily identify. While actuaries are familiar with generalized linear models and other traditional multivariate analysis, the use of machine learning with random forest and gradient boosted tree algorithms can enhance the analysis. This can be particularly useful in marketing, underwriting and discretionary pricing applications.

Also, data scientists can be very helpful in identifying claims that may significantly increase in value over time (the company can then take early steps to hopefully reduce the eventual size of the claim).

If a company is small or new to using data scientists, then the data scientists are all typically housed in one department. As the company becomes more accustomed to using data scientists, then the data scientists are typically housed in multiple areas (e.g. claims, underwriting offices).

The data scientists’ training should include some basic insurance knowledge. For example, for very long tailed lines, it is expected that all accounts will have low loss ratios at 12 or 24 months. This does not mean that the business is highly profitable.

Jessica Leong wrote an article titled “3 indicators that ensure data science models achieve the impact you were hoping for in commercial insurance” which highlights best practices for data scientists. Some of the criteria of models built by data scientists should include an analysis of:

-

Accuracy — accounts identified by the model as high risk should produce high loss ratios.

-

Execution — should measure if the end-users are using the model. If the model is not being used need to ask why.

-

Impact — the model should increase premium, reduce losses or reduce expense.

As indicated in the above table, data scientists are not widely used in the reserving function. However, that does not mean the reserving actuaries cannot use or incorporate the results of data scientists analyses in their reserving analysis. The reserving actuaries need to consider how their assumptions might change to reflect

-

enhance pricing and underwriting as a result of data scientist models or

-

change in claim reserve adequacy if models were developed to identify claims with the potential of large development.

Efficiencies of Reserving Departments

In addition to the staffing of various departments, it is also important to determine if the department and processes are efficient. One might ask:

-

Is there sufficient governance and internal control around the various reserving processes (data, analysis, reporting, etc.) to provide reliability and to meet regulatory and audit requirements?

-

Are too many tasks done manually or with outdated software?

-

Are the appropriate early warning tests in place to highlight changing trends?

Governance

For any reserving department, it is essential that the appropriate governance and internal controls are in place. One needs to review the following:

-

Who has access to data.

-

What methods are used for which segments of business?

-

Who selects the assumptions, how are the assumptions selected and how do the assumptions change?

-

Who makes the final selections?

A clear audit trail and version control process needs to be in place. This is necessary not only to ensure the quality of the analysis, but also to satisfy various regulatory and audit requirements.

Using automation is a key practice to assist with the governance process. Automation can minimize errors especially with loading of the data, calculations, exporting results and summarization of the data and analysis.

Automation

Stronger departmental quality controls can often be achieved or improved by automating many parts of the reserving process. Automation capabilities are often delivered by using vendor provided out-of-the-box quality reserving software solutions. Many can also be implemented with existing Excel-based reserving tools through the use of automation-specific computer programs (remote process automation, or “RPA”) or computer macros (e.g., Visual Basic macros, Python scripts, or similar platforms).

In the 2020 survey, 33% of the respondents use Excel only and 57% of the survey respondents use both Excel and specialized reserving software (either homegrown or externally sourced), while 8% of the companies rely solely on outside vendor reserving software.

Of the companies that do not use a reserving software tool, 55% responded that reserving is still mostly a manual process, while the remainder said reserving is somewhat automated.

Thirty-three percent of the companies that do not use reserving software believe their current process is appropriate. These companies generally did not have a separate reserving and pricing team and generally (75% of the time) had under 5 people in the actuarial department.

Automation has other advantages in addition to quality controls, such as:

-

Increased efficiency (reduction in time).

-

Cost reduction (fewer employees needed for the same analyses).

-

Increased productivity (time for other analyses or more in-depth analyses).

-

Consistency and hence confidence in the results and templates.

-

Reduction in human error.

In the long run, automation often leads to reduced cost due to efficiencies gained. However, there is an initial investment in automation, whether that is the time to create computer programs and macros or the cost of software along with the time needed to learn and incorporate the software in the reserving process.

Companies with automated reserving processes often perform their analyses more frequently, typically quarterly with a monthly roll-forward for actual verses expected analyses. A deep-dive analysis may not be necessary each month or quarter for every segment. Early warning dashboards allow companies to focus their attention on the lines of business with the most volatility, and an automated roll-forward approach may be sufficient for segments with greater consistency. Automated processes also allow the actuaries more time to perform more granular level reviews, where needed.

We note that based on a survey alone, it is hard to quantify the comparative complexity of individual companies reserving processes and their level of automation. However, we have summarized how companies view their processes in terms of automation.

Few of the companies surveyed believe their processes are very automated. Companies that are very automated are generally larger companies which perform monthly or quarterly reserving reviews and use internal or outside software tools to analyze over 100 segments.

Fifty-three percent of the companies surveyed believe their processes are somewhat automated. Unfortunately, there are few common characteristics of these companies to draw comparisons.

Forty-three percent of the companies view their process as still mostly manual, even though the companies perform either monthly or quarterly reserve reviews.

-

Interestingly, 50% of the companies that view their processes as mostly manual, also use either an internal or external software package.

-

Thirty-three percent of the companies view their current process as appropriate with no need for improvement, while 66% of the companies have an expectation of either gradual improvement or a demand for creating greater efficiencies.

-

Approximately 25% of the companies review less than 20 segments, 50% of the companies review between 20 and 50 segments, and 25% of the companies review over 50 segments.

We would expect companies that perform monthly and quarterly reserve analyses and analyze more than 20 segments would invest in automation to make their processes more efficient.

A benefit to automation is that companies can increase the quality and quantity of reserving reviews. Compared to the survey conducted in 2012, commercial insureds appear to be increasing the number of segments reviewed for reserving. This is not surprising as more products are offered by various companies and a more refined analysis can be done in reviewing more segments.

Automation is often a challenge for insurance companies, especially due to legacy systems and historical mergers. In our survey, over half of the companies responded that lack of resources including time, staff, and budget are among their major challenges. Other challenges include incompatible systems. Some companies might not have invested in automation because they believe their reserve process changes frequently which does not lend itself well to automation.

Although we believe it is best practice to utilize automation in the reserving process, we also recognize that establishing reasonable reserves cannot be done solely through purely mechanical processes. Data gathering, input, initial methods, initial assumptions, actual to expected tests and benchmarks can be automated. Additionally, the aggregation, reporting, and allocation of results as well as documentation can be automated. However, input, assumptions, and results need to be evaluated by a trained professional to ascertain the reasonableness of the results and make modifications as needed, especially in certain lines of business (long tail lines or lines without credible historical data) as well as in a changing environment in which the past may not be as predictive of the future as the automation might imply. Early warning flags or benchmark reports can be created with the automated process to help the actuaries identify emerging trends and areas that might need additional review.

Commercial Compared to Homegrown Reserving Software

Commercial reserving software,[1] homegrown reserving software as well as Excel with automation can bring consistency to the analysis process. This is accomplished by not only providing more consistent analysis across various coverages, lines, and businesses, but also among analysts. This allows for more efficient use of actuarial time and streamlines the process for the manager review.

Given the sophistication and flexibility of modern commercial reserving software, there are many additional advantages to using commercial reserving software packages. Commercial reserving packages:

-

Are developed and tested by software engineers working closely with experienced actuaries, to provide a more reliable platform and results.

-

Offer easy and immediate access to ready-made analyses, including approaches that reserving teams may not have the time to develop on their own.

-

Incorporate the ideas and experience of many actuaries in many other companies and environments.

-

Are continually maintained and improved, with little involvement in a company’s reserving team.

-

Have access to a potentially larger pool of technological expertise than a company, in areas such as process automation, cloud computing, and machine learning.

-

Provide structure and security to add significant governance around many of reserving work processes. These governances are much more challenging to incorporate in an Excel with automation environment.

For homegrown software, often there is insufficient documentation, and the software is developed by subject matter experts which may lead to challenges in making it sustainable, especially if the subject matter experts leave the reserving area or the company. This challenge can lead to less automation in order to make the software more understandable and easier to maintain, but slower and simpler. Actuaries are not necessarily trained software experts, so depending on the complexity of the software or automation, companies may need to hire additional staff to maintain and update the homegrown software.

A key in best practices in reserving departments is to ensure that information and process governance are in place, including appropriate documentation. This is important for both homegrown and commercially purchased reserving software. However, as stated above it can often be more easily achieved with a commercially purchased reserving software package.

When using Excel, it is tempting to use the flexibility of the software to allow agility. The benefit of Excel’s agility is its weakness with regard to governance. There is the opportunity to corrupt formulas and ‘hard code’ numbers which lead to incorrect results and lack of consistency. For governance purposes, it is important to put a proper peer review process and lock down the ability to alter the spreadsheet without the proper oversight. This then dilutes the benefit of the Excel spreadsheet.

Challenges of Reserving Departments — Data, Analysis and Reporting

Milliman’s survey indicated that companies are using the same general methods as they were 10 years ago. Despite the fact that methodology for setting reserves has been stable over time, companies still face challenges. The most common challenge is obtaining timely and reliable data for the analysis. Approximately 50% of the companies have difficulty. Half of these companies struggle with obtaining reliable data for every analysis period and find it takes longer than it should. While the other half just struggle with obtaining specifically requested data.

Not surprisingly, the difficulty in obtaining data often leads to the next major challenge: meeting deadlines for financial reporting.

Companies also indicated that rolling up the results, allocating the results to the appropriate business units and producing final reports also present challenges. Lastly, keeping costs to an acceptable level is always a concern.

A modern reserving system should ease the data burden, be cost effective, allow meeting deadlines (faster analyses), and simplify rolling up and/or allocating the results relatively automatically.

We note that modernization of the actuarial process might not often be used in reserving departments that are small due to the cost to transition and the need for business benefit realization. However, both large and small companies should consider utilizing a modern reserving system. A cost-benefit analysis needs to be done to determine if increasing automation or investing in reserving software would increase efficiency and improved governance to offset the cost of the investment, as well as allow for actuarial resources to be diverted to non-traditional reserving exercises (e.g., machine learning, deep-dives, more advanced/responsive models, etc.)

Communication

As stated above, communication is another source of inquiry when determining the effectiveness of the actuarial department.

-

Is sufficient conversation and knowledge transfer occurring between the actuarial department and the other key departments (e.g., claims and underwriting) to inform the reserving process?

-

Are senior leaders and other business leaders receiving the information needed to make good decisions?

-

Are information, analyses and conclusions communicated in a way that both actuaries and others can understand and take action on them?

-

Is uncertainty of results and specific assumptions communicated effectively?

Proper communication is essential. Unfortunately, at times and in some companies, the actuaries do not communicate clearly and concisely. In our survey, we asked how often the reserving actuaries interact with claims, underwriting, pricing actuaries, and the audit committee. As with most of our questions, the best practices cannot simply be measured by the amount of interaction, but also have to be determined based on the quality of the interaction. Has knowledge and information been gained and transferred?

We note that about 20% of the companies we surveyed responded that they communicate with claims, underwriting, pricing, and the audit committee only when necessary. We do not believe limited communication is best practice and it will certainly not result in the best outcome.

Interaction with Claims

The actuaries in most companies have some interaction with the claims department. Approximately 45% have monthly interactions, 23% daily, 15% quarterly, and 18% only when necessary. Interaction with the claims department is essential in order to understand changes in claim trends that the claim examiners are seeing or discuss changes in case reserve practices or initiatives. It is important, however, for the actuaries to listen and not to unintentionally influence.

The actuary should listen to the claims department and independently evaluate their observations/initiatives. For example, if a claims department has an initiative to close claims faster, can the actuary verify this in the data? If so, what types of claims are closing faster, small dollar claims that have little impact on the development triangle or larger dollar claims that may reduce the paid tail? The actuary could discuss unusually large claims with the claims examiner to determine if and what level of additional IBNR might be needed for the large claims.

It is not appropriate for the actuary to influence the claims department. For example, a reserving actuary should not tell a claims handler “We noticed there appears to be a slippage in case reserve setting and we are going to evaluate who isn’t setting appropriate case reserves.” In this instance, the actuary should have a conversation with the claims manager to discuss potential case reserve methodology changes to determine if the perceived slippage is backed by actual changes in process.

Interaction with Underwriters/Pricing Actuaries

Apart from companies with a combined reserving and pricing unit, reserving actuaries tend to interact with the pricing/underwriters in a similar frequency as the interaction with the claims department. Interaction with the pricing/underwriting department is essential in order to understand changes in pricing, changes in retentions and attachment points, changes in the terms and conditions and overall changes in the business. However, it is important that the reserving actuaries again attempt to independently quantify changes in data consistent with the messaging from underwriting as opposed to relying solely on the impact the pricing actuaries might believe their changes will have.

Interaction with the Board Audit Committee

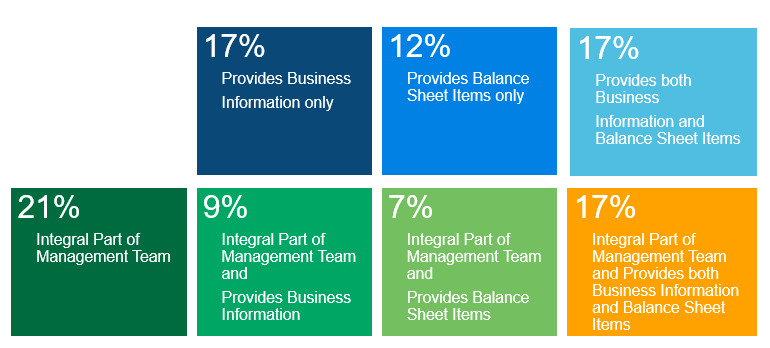

Figure 11 displays how the actuarial department is viewed by the companies.

As shown above, most companies responded that the chief actuaries/reserving departments are a part of the management team and provide the necessary information. Only 12% of the companies perceive their department provides balance sheet estimates only.

It is important for the chief actuary at the company to be an integral part of the management team as well as have the reserving department provide essential business information in addition to balance sheet items. If the chief actuary is an integrated partner, then they can link the information from all of the areas together with the pricing and reserve analysis to provide valuable color commentary. Anecdotes and stories are often far more compelling than figures. When the narrative is backed by facts, it can be even more effective and persuasive. For example, telling the Board or audit committee that the unpaid claim liabilities were short and additional reserves were added to the financial statements is useful, but pointing out the areas the reserves were short, the causes for the adverse development and the impact on profitability is also important.

With the appropriate reporting of analysis at the various levels of detail, the reserving actuary can provide important observations of changes in various business practices that the remainder of the leadership team might not observe. This can particularly be true when a change is across the entire company, but each individual business unit believes it is anomalous. The reserving actuary can connect the observation across the units and provide the observation which can then be understood at each individual business unit. The questions that they bring forward can illuminate such events and business process changes.

Forty percent of the reserving teams surveyed interact with the audit committee on a quarterly basis. Another 20% interact on an annual basis. This interaction is necessary and appropriate. However, it is crucial to emphasize that it is not just the amount of interaction, but what and how the actuaries are communicating to the audit committee.

We view it is best practice for the chief actuary or chief reserving actuary to have one-on-one educational sessions with any new board members. As previously stated, actuarial concepts can be complex, and a new board member may be more inclined to ask questions if they have a background on the reserving process and historical company uncertainties. It is also good practice for the Board Audit Committee to meet one on one with the Chief Actuary without the Chief Executive Officer (CEO) and Chief Financial Officer (CFO). This will allow the Board to ask pointed questions and the actuary can address concerns.

As insurance professionals with a broad and far-reaching professional organization, and a vast thirst for knowledge, it is generally expected that the reserving actuary and actuaries in general are well versed in the industry trends. This includes economic changes, regulatory changes and competitor results. The board and senior management count on this from actuaries and specifically the reserving actuaries.

The best practice in communication is to communicate regularly and often with other actuaries within the company and outside, other business units and all levels of leadership. The communication is meant to teach and convey information. It is also to intentionally impact processes, but not unexpectedly alter results.

Use of Visualization Software

It is not only important to have regular communication with departments outside the reserving unit, but also vital to be able to communicate concepts and trends effectively. Utilizing visualization software (interactive displays of data) can often help communicate trends and explain changes in the underlying data.

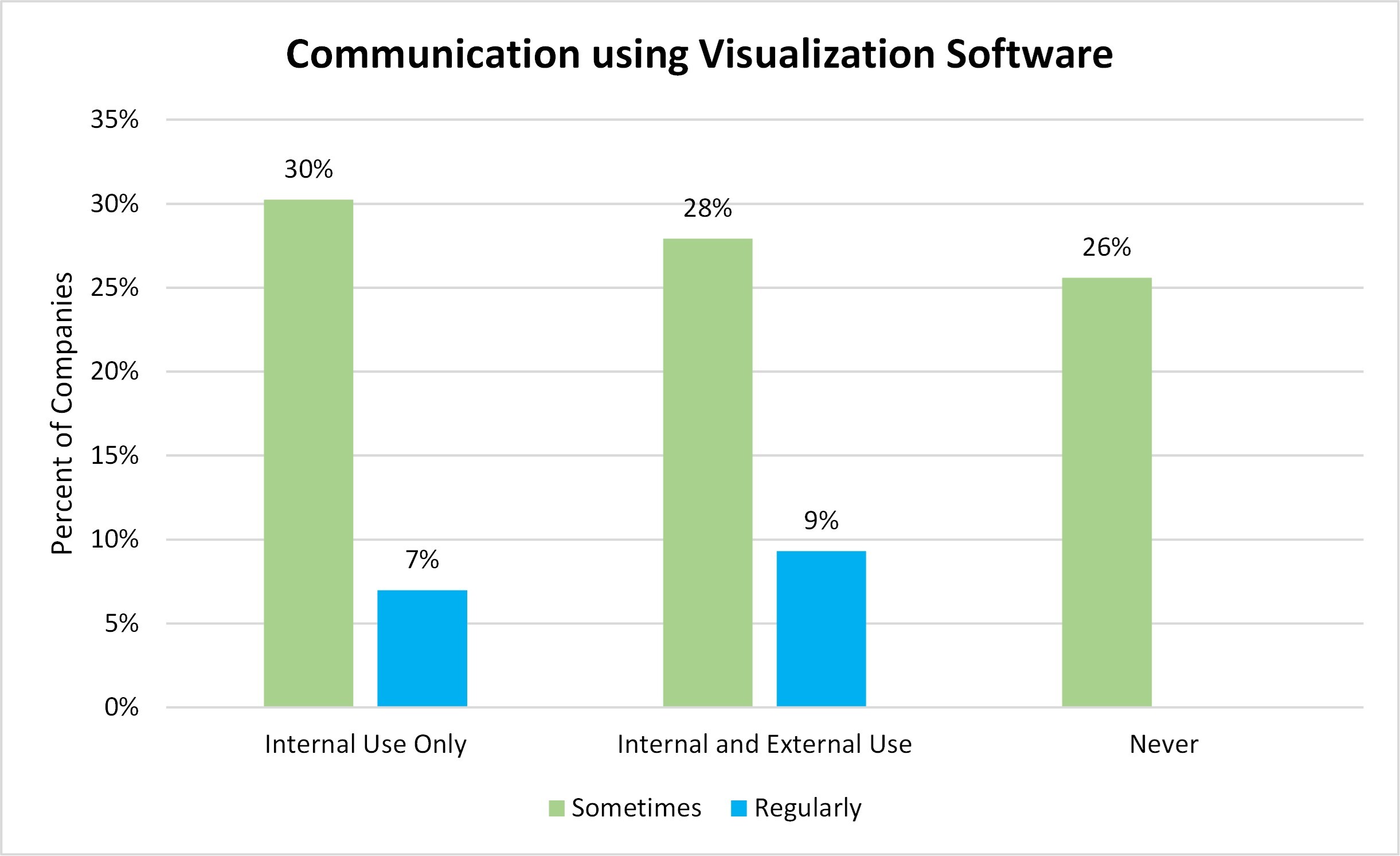

However, visualization software is not as widely used as expected. As shown in Figure 12, only 9% of the companies use visualization software as a fundamental part of their communication and communicate both within and outside the actuarial function. Twenty-six percent of the companies do not utilize visualization software. These companies tend to have smaller unpaid claim liabilities.

If effectively used, visualization software and techniques can allow a chief actuary, CEO/CFO or business leader to review high level results (loss ratios, frequency and severity information) and drill into any level of detail to decern what might be the drivers of the results. Management could easily review results by line of business, geographical location, individual claims etc. without making ad-hoc requests for the information. Training on visualization software/reports is essential in order for the information not to be misused or misinterpreted.

Visualization software can allow users to more easily see and investigate trends in data, have improved access to data, and provide additional and more complete information to management.

Communicating Uncertainty

Reserving actuaries estimate unpaid claim liabilities. These estimates, by their nature are uncertain, as the estimates reflect future contingencies. Changes in assumptions or underlying industry trends such as inflation rates or litigation trends contribute to the variability of results. Changes in a company’s internal practices or procedures add additional variability and uncertainty to the indications. Internal company changes include changes in settlement rates, case reserve adequacy, and new types of losses that are not sufficiently represented in historical experience. It is important for the actuaries to communicate not only the uncertainty associated with global influences but also company specific influences.

It is often helpful when actuaries are communicating to the board or audit committee to illustrate the uncertainty by changing assumptions. For example, the actuaries could quantify the change in unpaid claim liabilities under various situations, such as:

-

An increase to the claim cost trends by 1% or 2 % than what was reflected in the analysis.

-

If adjustments were not made to the settlement rate.

-

If new types of losses continue to emerge at a particular rate.

If the reserving department determines a distribution of unpaid claim liabilities, it is often helpful to illustrate where in the range the unpaid claim liabilities would fall if a certain assumption is realized. For example, one could explain that if medical inflation increases by 3% (from 4% to 7%) then unpaid claim liabilities would increase 20% and this would be equivalent to a 70% confidence level. It is important not to just display a range of results but explain and illustrate under what circumstances a higher or lower result might be reached.

Not only is it important to illustrate, explain and provide sensitivity testing on known drivers of uncertainty, but it is also key to communicate unknown uncertainty. Although unknown uncertainty is harder to communicate, it is essential to acknowledge that it exists and is not quantified. Unknown uncertainty could include future changes in tort reform, judicial attitudes, COVID claims, etc.

Adaptability of Reserving Department

In addition to evaluating effective communication, it is also important if the reserving department is adaptable. One might ask:

-

How are actuarial methods responding to the changing environment?

-

Are the actuarial leaders developing the appropriate new skills to effectively manage, especially in our ever-changing pandemic environment?

-

Does the actuarial team have the right skillsets to meet the evolving needs?

Actuarial models work very well when underlying conditions stay relatively constant. However, historical actuarial models, without adjustment, work poorly when underlying conditions change rapidly. In the late 1990s conditions changed rapidly (e.g., rate decreases, coverage expansions) and actuarial projections were biased low. In the early to mid-2000s conditions rapidly changed again (e.g., significant rate increases, low claims inflation) and actuarial projections were biased high. Appendix A provides some specific examples in more detail.

COVID has had a dramatic direct effect on the insurance market. Some coverages have experienced significant direct losses (e.g., event cancellation, export credit, business interruption in the U.K.), while other coverages have seen reduced claims (e.g., personal auto and workers compensation in non-essential businesses, general liability).

COVID is also having an indirect impact on some companies and coverages:

-

The economy suffered due to lock down restrictions resulting in financial difficulty for some companies (e.g., a record number of bankruptcies) — this may lead to more D&O (Directors & Officers) and professional liability claims against advisors;

-

The work from home situation resulted in a significant increase in the number of cyber incidents and insurance claims.[2]

-

The courts are back-logged and claims are remaining open for long time periods, which eventually may result in higher indemnity cost and legal and other adjusting expenses associated with the claims.

The economy, travel etc. are returning to normal, although a “new” normal. This may cause a strain in several ways that may lead to more insurance claims. For example, individuals traveling more for work and pleasure will lead to traffic congestion. At the same time freight shipments in the U.S. are accelerating and there is a shortage of commercial truck drivers. In addition, people are less likely to use public transportation due to the residual uncertainty around the pandemic. Each of these factors imply more accidents.

Many believe that the pent-up demand will result in a boom for the hospitality industry. The restaurants, hotels, etc. will be more crowded. At the same time, there is labor shortage in the U.S. and several businesses are hiring new workers. Historically both these factors generally result in higher claim costs.

In addition to the above factors, inflation is at the highest level in 30 years and insurance claim costs seem to be increasing at a higher rate.[3] Also complicating reserving and pricing analyses is how to treat the COVID outlier years of 2020 and 2021.

The above factors will require best in class reserving departments to:

-

Develop key metrics to identify trends (e.g., early warning systems). This will entail analysis of company data and industry data. For example, company data could be analyzed more granularly such as monthly analysis of claim counts and trends in claim counts, premium changes, changes in retention, change in policy wording etc. Visualization software can help identify trends. Industry data could include for example the number of public cyber events by month and trends in industry frequency and severity. Industry data can include reviewing competitors’ results, press releases and industry analyses of various markets.

-

Increase interaction with claims and underwriting to make sure assumptions underlying the analysis are appropriate. Discuss judicial delays and claims delays due to pandemic related staffing complications. Understand expansions or contractions of coverage terms and new exposures for new types of business. Finally, account for the impact of a hard market for Commercial Lines and the complicated market for Personal Lines with a dramatic increase in social inflation.

-

Communicate effectively with senior management, claims, and underwriting departments the underlying assumptions and their impact on the resulting conclusions. Management should expect to understand the actuarial work and how to take action based on their work and should be asking:

-

How has the actuarial departments most recent work changed the profitability estimate of various books of business?

-

What are our “early warning systems” telling us — what should I be concerned about?

-

What is our market knowledge telling us?

-

How uncertain are our estimates?

-

How do prior year reserves affect current reserves and profitability? (Are there any prior year reserve issues?)

-

Adapting to the Changing Work Environment Due to the Pandemic

The COVID pandemic has affected actuaries both personally and professionally. The working environment of the insurance industry has also changed in ways we previously did not contemplate. The following provides our observations of changes and how actuaries may need to adjust in order to provide the same level of analyses, business insights and observations and professional training, as in the past.

Prior to the pandemic, 50% of the companies surveyed had no reserving staff working remotely, not even 1 day a week. Many companies have and will continue to allow a significant percentage of the workforce to work remotely at least part of the time.

In addition to reserving staff working remotely all or part of the week, the in-person office dynamics are likely to change as:

-

Office space is reorganized to allow for more social distancing.

-

Workspace is retrofitted to provide more separation between workstations;

-

The number of people at in-person meetings is smaller or limited.

-

The reserving team is separated into groups and working in the office on a rotating basis.

What new hurdles will this create?

Some believe that in-person meetings are more productive than virtual meetings. A study published by the Journal of Neuroscience[4] highlighted that in person meetings stimulate the brain differently, yielding stronger and faster connections.

Working remotely is convenient for many reasons, including:

-

Reducing or eliminating commute time.

-

Hiring from outside a company’s geographical area without the need for employees to relocate.

-

Retaining employees that want to relocate to a different geographical area.

Some disadvantages include:

-

Computer issues/sound quality due to personal bandwidth.

-

Workers being distracted by their surroundings.

-

Increased screen fatigue.

-

Missing important casual encounters such as conversations that occur at the coffee station or during lunch.

-

Reduced natural or spontaneous opportunities for mentoring and networking.

-

Greater difficulty in training / performance evaluation.

Since remote work has been embraced and is a reality, best in class actuarial departments will need to adjust.

We note that challenges moving to an all or part time virtual office during this pandemic might have been mitigated because companies were able to capitalize on:

-

A rapport developed from years of working together in the office.

-

Training and work responsibilities previously established.

As new members are added to the team and existing staff settle into a virtual work environment, actuarial managers will need to learn new skills to help them manage a remote workforce efficiently. An actuarial manager is no longer able to walk through the office reassigning work or answering questions on a casual basis. More formal planning will need to be done to ensure proper training and education, work is distributed equitability, staff are mentored, and professional opportunities are provided.

This will require developing guidelines and tips to help managers, increased interaction with human resources and other forms of education (e.g., webinars).

Several studies and articles have been published regarding making remote work more efficient. One publication is Gartner’s — 9 Tips for Managing Remote Employees.[5] Actions based on our reading and experience that seem to be effective include:

-

Encourage staff to conduct meetings with their camera on so that they can see the other individuals on the call. This seems to create stronger working relationships.

-

Have clear expectations and understanding of remote working; including specific hours to be working (or flex hours), dress code for in-office meetings verses meetings with those outside of the company.

-

Have some virtual meetings with all team members so the group feels connected, but not so often that they are a burden. The appropriate frequency may depend on the amount of change the company is going through.

-

Have occasional virtual social meetings to celebrate anniversaries, promotions, etc. Once a month or quarterly depending on the amount of other interaction occurring.

-

Have newer staff give an occasional presentation. This will allow the staff to meet new employees and give the new employee some public speaking experience. It can be a simple presentation such as a current assignment the employee worked on.

-

When the environment allows, have occasional meetings in the office on important topics. If possible, have all of the staff on the team in the office one day a week and meet during that day to update each other on work activities.

Technology Issues-More Working Remote

At the start of the pandemic, many companies needed to scramble to quickly enable employees to work at home. Some companies allowed their employees to take home computer equipment, monitors, printers etc. in order to work effectively from home. Other companies allowed employees to use their home equipment. In order to be effective at home, some employees needed multiple screens to allow people to look at the data and people at the same time. Companies had to deal with internet / bandwidth problems, security / confidentiality of data concerns, etc.

The initial communication challenges that may have plagued the reserving process within the reserving departments at the onset of the pandemic have been largely overcome by most companies. Now as working remotely becomes more permanent, companies will need to standardize their remote working policies and procedures. What is the standard equipment for an at home office? Does the company or employee provide the equipment? Does the company provide a duplicate set of equipment for in-office use when the employee comes back into the office even if it is just a day or two a week? Do employees who return to the office on a part-time basis share equipment with other part-time in office employees?

The policies and procedures will vary from company to company and could also vary from department to department.

Off-shore Versus Working from Home

As we have transitioned to working from home to overcome the impact of the global pandemic and the initial communication challenges have been reduced, this situation leads to the question about the ability to near shore or off-shore for the savings. Companies have effectively been able to utilize remote employees. Does this expand the talent pool of workers? Can employees be hired in areas with lower costs of living and essentially have lower operational costs? Can work be outsourced/off-shored resulting in lower operational costs?

Our survey was conducted in the summer of 2020. At the time only 12% of the companies responding were considering increasing the use of off-shore / outsourcing arrangements. At the time of the survey, most people probably did not expect the pandemic to last as long as it is and its continual impact on the working environment. In this new working environment, more companies might reconsider the benefits and shortcomings of near shore, off-shore or outsourcing arrangements.

The challenges are about repeatable processes in the quantity that can replace higher cost workers performing manual tasks. Conceptually this allows higher cost on-shore actuaries to complete more value added analysis. Challenges include the communication challenges with potential English as a second language and multiple time zone differences. Finally, the number of repeatable processes may be limited, hence the benefit might not be worth the cost of off-shoring but may be worth the investment in greater automation. For many, better reserving software may be more reasonably priced and provide more overall comfort and control throughout the analysis process.

Conclusion

As discussed above, there is no optimal way or best practice to structure an actuarial reserving department that works for all companies. It is important to incorporate a structure and size that meets the needs of an individual company in consideration with complexity of business, number of analyses (both frequency and segmentation) and use of automation.

Best practices in reserving departments have sufficient governance and internal control around the various reserving processes. This is often obtained by using reserving software and greater reliance on automation to reduce human error.

In order to provide quality actuarial work, best in class actuarial reserving departments need to effectively communicate with claims and pricing/underwriting. It is important for the reserving department to obtain and independently verify information without unintentionally influencing the other departments.

Best in class actuarial departments often use visualization software to more easily and effectively communicate and investigate trends in data and provide more complete information to management. This will allow business leaders to help make better business decisions.

Best in class actuarial reserving departments have implemented actual to expected tests and benchmarks to identify trends more quickly in the data. They then investigate the trends and modify their actuarial analyses as deemed appropriate.

As working environments change, it is essential that actuarial departments continue to focus on quality actuarial work including training and mentoring younger actuaries as well as effectively communicating with other departments and business leaders.

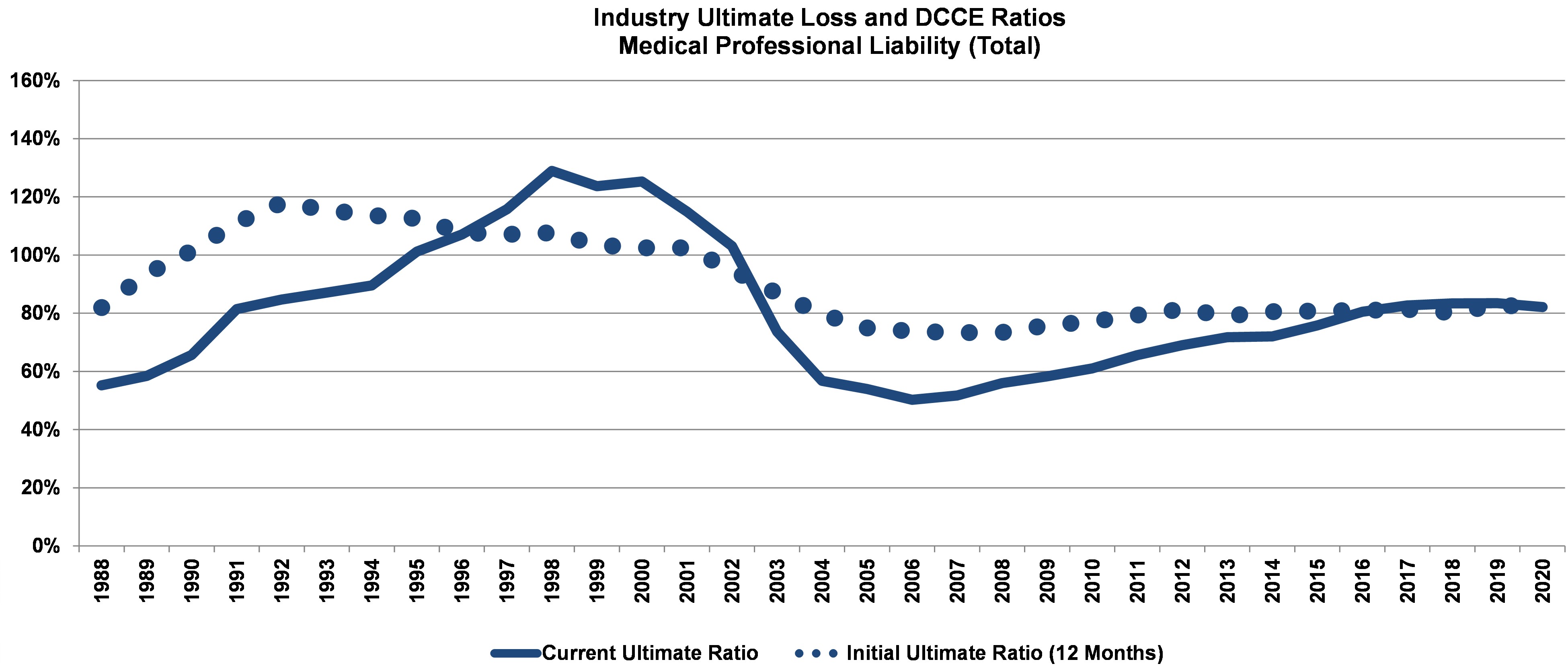

Appendix A — Historical Perspective of Changing Environments

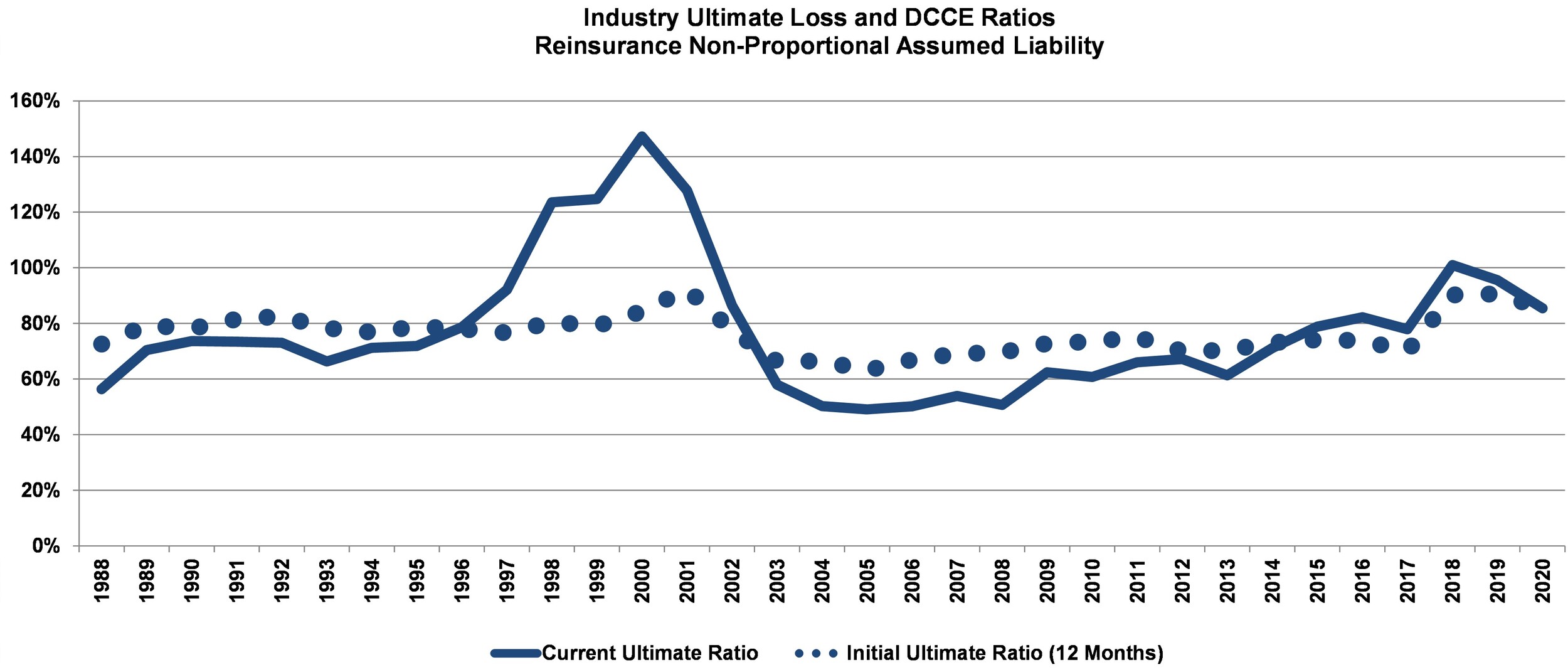

To provide some perspective, let’s look at accident years 1998 to 2001 for the casualty excess reinsurance market (the same pattern was also observed for many other markets during this time period). Figure 13 shows Schedule P Reinsurance - Nonproportional Assumed Liability loss ratios by accident year for the casualty reinsurance market for accident years 1988-2020. In this graph we displayed not only the latest available ultimate loss and DCCE ratio (as shown by the solid line), but also the initial indicated ultimate loss and DCCE ratio (as shown by the dots).

As illustrated, the 1998 through 2001 loss ratios are outliers with loss ratios above 100%.

The initial estimates for the 1998 through 2001 accident years (all about 80%) developed significantly over time. These initial reserves were substantially misestimated. Let’s consider some possible reasons.

-

The 1988 through 1996 accident years had relatively favorable loss ratios. Looking in our rearview mirror indicated that we would expect a priori loss ratios for 1998 through 2001 to be similar.

-

The good underwriting results of the early 1990s and the expanding economy that followed led to a feeling of optimism. This led many underwriters to expand terms and conditions which increased claim costs. Many actuaries were aware of these changing exposure trends, but it is doubtful that the actuaries fully understood the magnitude of the changes and the ultimate impact on the loss ratio.

-

Finally, inflation exceeded expectations.

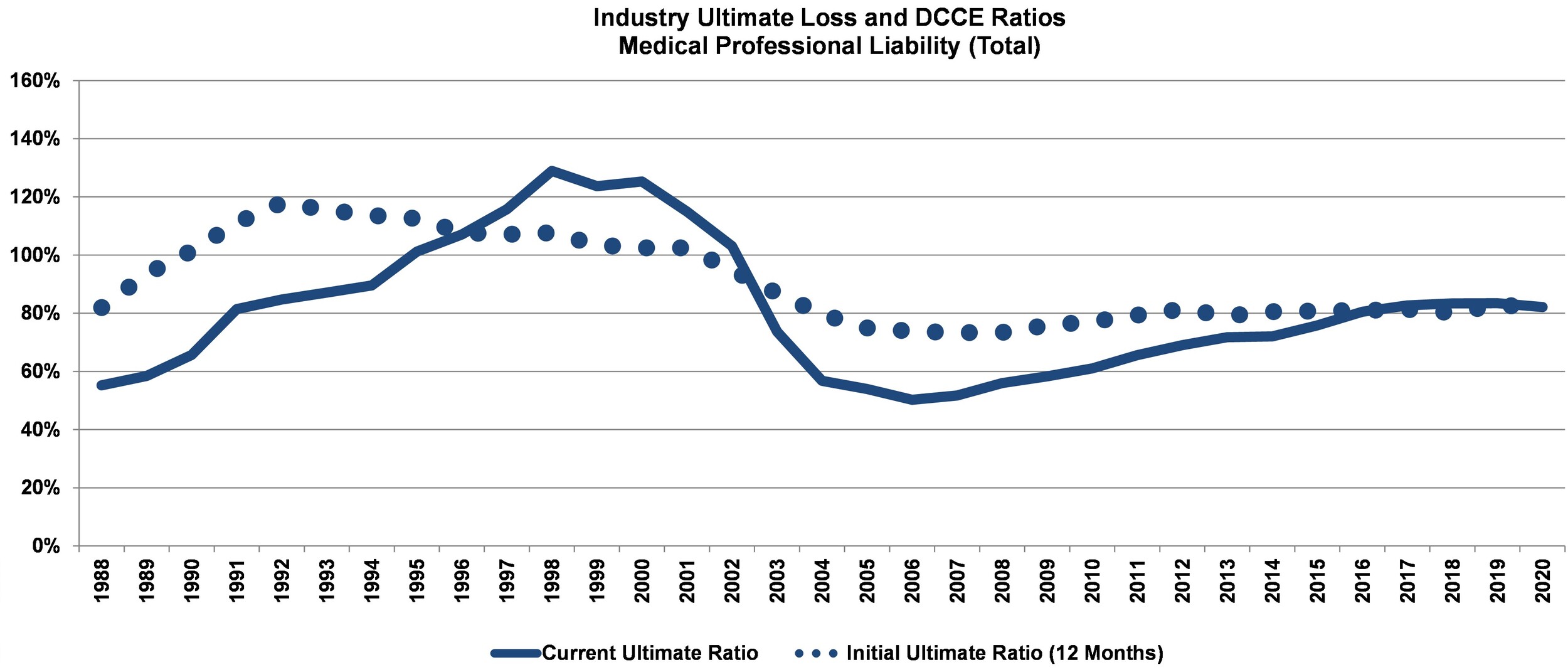

A similar situation occurred in the Medical Malpractice market from 2003 to 2014. See Figure 14.

The 2004 through 2010 ultimate loss ratios were far better than initially indicated and much lower than the 1995 through 2002 years. Some of the factors contributing to this favorable development were:

-

Significant rate increases which may not have been fully reflected by actuaries in their work due to uncertainty in claim frequency and severity trends.

-

Looking in the rearview mirror and relying on the older years for a priori loss ratios.

-

Significant increases in self-insured retentions for hospitals which reduced losses more than expected by reducing both frequency and severity.

-

Very effective risk management procedures implemented by insurers that significantly reduced claim costs.

-

Tort reform.

Best in class actuarial reserving departments have implemented actual to expected tests and benchmarks to identify trends in the data more quickly. They then investigate the trends and modify their actuarial analyses as deemed appropriate.

The changes and impact to ultimate loss ratios were not as obvious in these historical examples when they began, but are clear in hindsight. The significant impact of the COVID pandemic was nearly immediate. As our economy emerges from the COVID pandemic, the world will rapidly change, and actuaries will need to be able to adjust to these changes.

It should be noted that Milliman, along with other actuarial companies sell commercial reserving software packages. Questions regarding specific commercial reserving software packages were not part of this study.

“The WFH impact on the cyber insurance market” NU Property Casualty 360 July 22, 2021

“Inflation for P&C Insuers: Managing Risk to Both Sides of the Balance Sheet” Conning March 14, 2022

Referenced in “Why face-to-face gatherings till matter” by Matt Villano, CNN June 8, 2021

“9 Tips for Managing Remote Employees” Gartner January 4, 2021