INTRODUCTION

1.1. Premium Audits: Defined

Premium audits are conducted in a variety of commercial property and casualty insurance lines, most commonly in workers’ compensation (WC). WC policies are customarily subject to mandatory annual audit. Therefore, this line has the highest volume of audit premiums. In other auditable lines, the insurer may have the right to audit the policy but will exercise this right on only a subset of its business.

In a premium audit, the insurer collects data on the insured exposures, by classification and in total, following the conclusion of the policy term. The exposure base may vary, but is most commonly payroll for WC and may be sales, square footage, or hours worked for commercial general liability. A common exposure base for commercial automobile liability is car-years, and in property insurance one may use the insured property value.

The audited exposure count is multiplied by a contractually specified rate per exposure to derive the final premium for the policy term. The premium audit adjustment represents the difference between the final premium and the previously estimated premium on the policy. The previously estimated premium is the deposit premium calculated at or before policy inception, increased or decreased for any midterm adjustments (see Section 2.3).

From the standpoint of the insurer’s revenue, the audit adjustment may be positive or negative depending on whether the final exposure count is greater than or less than anticipated. A positive premium adjustment would typically cause the policyholder to be invoiced for additional payment due. A negative premium adjustment would result in a rebate or credit to the insured.

1.2. Introducing the CAS RWG Survey

The CAS Reserves Working Group (RWG) recently conducted a small online survey of personnel with responsibility or oversight over premium audit forecasting at several commercial insurers. Results of this survey are mentioned throughout this paper for additional perspective.

All five respondents indicated that their companies conduct premium audits on WC policies. In addition, four out of five companies conduct audits on policies in at least one other line of business. The most common exposure base at all five companies was payroll. Four out of five respondents stated that their company’s total ratio of audit premium to written premium landed in the range of 0% to 5% in calendar year 2019, prior to the pandemic. One company had a ratio between 5% and 10%.

When asked about their companies’ calendar year 2020 audit premiums, two of five respondents indicated that the ratio of audit to written premium had fallen below 0%, indicating audit premiums had become negative overall. The other three responses were in the range of 0% to 5%. No responses were above 5%. Had shorter time periods been used in the survey, such as Q4 2020 or Q1 2021 when policies most severely impacted by the recession were being audited, a larger decline in audit premium would have been noted.

1.3. Aggregate Audit Premiums

When the economy is growing at a stable rate, one would expect audit adjustments to be positive when aggregated across an established book of commercial insurance policies or across a commercial insurer as a whole. This is because businesses are more likely to expand operations, sales, or payroll in such an environment than to contract them. The ratio of audit to estimated premium will be fairly stable in aggregate across policy periods, perhaps requiring little effort to forecast. The projections, and the assumptions underlying them, may be updated infrequently or receive a low level of scrutiny relative to other analyses such as loss and loss adjustment expense reviews.

However, when the rate of economic growth is in flux or especially difficult to predict, there is a pronounced risk that audit premiums will differ from historic norms or initial expectations. When the exposure base is expressed in units of currency, such as payroll or sales, then volatility in the rate of inflation or the value of the currency will add to the uncertainty.

The National Council on Compensation Insurance (NCCI) has compiled data from its Statistical Plan comparing audited premium to estimated premium (Lipton 2020). The data encompasses all the states where NCCI provides ratemaking services, including state funds. High deductible policies and mid-term cancellations are not included. The data shows that between 2006 and 2018, final audited premiums were consistently about 5% higher than estimated premium in nearly every quarter, with the notable exception of the Great Recession of 2007-2009. During this time, the ratio of audit premiums to estimated premiums reached a low around -3%, a decline of 8 percentage points from the pre-recession level. Negative ratios were seen in five consecutive quarters: Q2 2008 through Q2 2009. The size of the private WC market was about $30 billion annually at this time (National Association of Insurance Commissioners 2011), so one percentage point would have represented $300 million per year across the entire market — a very significant sum.

Since the COVID-19 pandemic began in 2020, the economy and financial markets have experienced significant volatility in both directions. Employment levels, interest rates, inflation rates, commodity prices, and other key economic variables have experienced rapid changes that have caught many by surprise. Although the widespread shutdown or curtailment of certain economic sectors due to COVID-19 is likely behind us, future events may occur which may cause significant economic disruption in particular regions or countries, such as pandemics, wars, or large-scale cyberattacks. Even absent such acute disruption, the high level of debt in developed global economies may increase the level of volatility in financial markets over a prolonged period of time, causing elevated risk to economies which depend on properly functioning financial markets.

Rapid and unanticipated changes in premium audit adjustments, for any of the reasons noted above or a host of others, will influence the revenue and net income of commercial insurance companies. More respondents to the RWG survey believed the aggregate amount of audit premiums was material to their company’s overall P&C revenue than did not. However, to the best of the author’s knowledge, there has been no actuarial literature to-date regarding the forecasting of audit premiums. This paper attempts to address the deficiency in the current actuarial research.

The remainder of the paper proceeds as follows: Section 2 provides an overview of the operational function of premium audit, as well as examples of operational changes that affect audit premiums. Section 3 discusses the impact of audit premiums on the financial statement, particularly the EBUB provision. Section 4 introduces an analytical framework that can be used to forecast audit premiums and thus to estimate the EBUB provision. Finally, Section 5 examines the impact of premium audit on measures of claim frequency which are integral to trend monitoring and to loss reserving.

2. Premium Audit Operations

2.1. Premium Audit Methods

An insurer may choose from a variety of methods to complete premium audits. High-touch methods, such as on-site field audits, are likely to be cost-prohibitive for all but the largest insureds unless there is reason to expect the exposures are meaningfully misstated. As in many areas of business, virtual meetings (e.g., videoconference or a virtual tour of company facilities) are emerging as an economical and safe alternative to physical audits. Insurers still use telephone calls for audit, as multiple survey respondents indicated this was the most common method at their companies. Paper mailings, email correspondence, and online web-based portals are also used, particularly for small business insurance policies which could be uneconomical to audit using other methods.

Half of the respondents to the RWG survey expressed uncertainty as to the most common audit method employed by their company, which suggests an opportunity for actuaries and analysts to benefit from more frequent communications with their premium audit operational teams.

When an insurer has multiple methods available, the choice of method for a given insured may be random or based upon simple rules. Many insurers would benefit from an analysis of their portfolio to look for certain characteristics that are shown to correlate with material understatement or overstatement of exposures at the policy level. The insurer may develop a predictive model to estimate the amount of additional accuracy it can expect to capture using each audit method relative to the cost of conducting the audit. Then the insurer can focus its most comprehensive audit efforts on the policies that are most likely to yield the greatest audit adjustment, whether positive or negative, for each dollar invested in the audit process.

For example, one of the objectives of premium audit in workers’ compensation is to identify instances in which the insured exposures are significantly misclassified, resulting in a mismatch between the rates and the propensity for loss. In WC, this may occur if an insured’s employees were placed into an incorrect classification. WC rates are expressed as dollars per $100 of payroll, varying greatly by class code. The class code is intended to capture the type of occupation performed by the employee, with high-hazard occupations requiring a significantly higher rate than low-hazard occupations to cover the elevated risk of occupational accident and injury in high-hazard occupations. A robust and effective audit department will be able to flag instances where there is a significant risk of underreporting or misclassification by using information obtained during the underwriting process or from other data sources as permitted by law and regulation.

The COVID-19 pandemic caused about half of the companies surveyed to make meaningful changes in premium audit methods. Most also anticipate that the changes will continue permanently. While details were not requested, in the author’s view it is likely these changes included a greater use of virtual audits enabled by technology such as videoconferencing. Travel restrictions and other public health orders that were enacted in 2020 made physical audits on the insurer’s premises more challenging to conduct. As with other areas of business, it can be inferred that companies found new ways to utilize technology to achieve their audit objectives at lower cost.

The small commercial market, defined as businesses with up to 100 employees and $100,000 of annual premiums, represents the largest segment of the U.S. commercial P&C insurance marketplace. Median annual premium is $1,000 to $5,000 (McKinsey & Company, Financial Services Practice 2016). Due to the relatively low premium per policy associated with these accounts, as well as the increasing deployment of digital direct-to-consumer marketplaces, an insurer may need to rely on the insured’s self-estimated exposures at the outset of the policy. The small business market is dynamic, with some companies experiencing rapid growth in a short time. Self-estimation of exposures, along with the potential for volatility in small businesses’ annual financial results, underscores the importance of the insurer being able to validate final exposures in an accurate and cost-effective way that provides as positive as possible of an experience for the customer.

In lines of business not subject to mandatory audit, predictive models may be used to select a subset of policies for audit. Policies not selected by the model may be audited at a longer interval, such as once every five years, if deemed to be at a low risk of having a material audit adjustment. This type of process improves the insurer’s efficiency per unit of cost allocated to the premium audit function, allowing savings to be passed along to consumers while also minimizing the amount of audits experienced by policyholders who proactively and accurately report their exposures.

Given the dollars at stake in premium audit, there is a strong case to be made for utilizing the skills of actuaries and data scientists in developing models for these purposes. Publicly available data sets, web mining, or private data aggregations may be used to quantify the risk that an insured’s exposures are not in line with the nature of the business operations or job functions. Much of this data may already have been obtained by the insurer through the underwriting function.

2.2. Billing and Collections

Once a premium audit is completed, if the resulting final premium exceeds the estimated premium, the audit adjustment will be booked to the policy and the insured will be billed for the amount due. However, the company’s work is not complete. The insurer will need to consider the risk that the funds will not be fully collectible or that the timing of collection may be delayed.

A sampling of factors which may impact the share of audit adjustments that are collected, as well as the timing of cash flow, is as follows:

-

The amount of negative audit adjustments (i.e., rebates to the policyholder) across the book, since these do not require collecting any funds.

-

The state of the economy overall or in the insured’s sector.

-

The size of the audit adjustment relative to initial premium. Larger audit bills may be uneconomical for the insured and may cause the insured to seek a negotiated settlement or payment plan.

-

Whether or not the insured has an in-force policy with the company. Businesses who have lapsed or changed insurers have less incentive to comply with the request for payment.

-

The effectiveness of the insurer’s communication with the insured throughout the life cycle of the policy. A policyholder who does not understand the audit or feels it is unfair will be less motivated to pay.

Estimating the allowance for uncollectible accounts is not typically the responsibility of the actuary, as the RWG survey confirms. Finance, accounting, premium audit, or billing (or some combination of these functions) would be responsible. These areas may have access to more specialized tools for evaluating credit risk. That said, an actuary who is forecasting audit premiums will want to be in contact with those responsible for estimating uncollectible amounts to ensure that the assumptions underlying both analyses are appropriately consistent.

2.3. Midterm Policy Adjustments

A policyholder or their representative may request a policy change while the policy is still in force. One such change, called an endorsement, can encompass many possible revisions to insurance coverage. Some endorsements change the number or types of exposures, such as altering business operations, adding a facility, or closing a facility.

One type of midterm adjustment arises from an interim audit, which is an audit prior to policy expiration. The policy contract may allow for interim audits under certain circumstances, such as a change in the insured’s operations. A policyholder may request to revise their exposure estimate for other reasons if permitted by the contract.

Midterm adjustments to an in-force policy may also directly follow from the audit of the prior year’s completed policy. If the audit adjustment is above (if positive) or below (if negative) a certain threshold, the insurer may immediately endorse the in-force policy to bring its exposure estimate in-line with the audit. This will prevent the need for another large audit adjustment when the in-force policy reaches its completion.

Failing to consider shifts in the level or timing of midterm policy adjustments in an analysis of premium audit, particularly when the economy is contracting, will increase the error of resulting forecasts. If insureds become more likely to request downward premium adjustments due to economic disruptions, as seen at the height of the COVID-19 pandemic, there will be fewer negative audits than otherwise expected.

To provide another example: if the insurer narrows the thresholds it uses to determine whether a midterm endorsement will be applied as a result of an audit of the prior policy term, it will make more such endorsements to its in-force policies. The increase in endorsement activity will get the company out in front of what would otherwise have been adjustments at audit, causing aggregate audit premiums across the book of business to be closer to zero than would have been expected in the absence of such a change. This example underscores the importance of considering midterm endorsements in the audit premium forecasting process.

2.4. Audit Non-Compliance

Workers’ compensation policies are customarily subject to mandatory annual audit, as required by state statutes. Some insureds fail to respond to the audit request in the required timeframe or to provide complete information. NCCI national item Filing B-1429, effective for policies effective on and after January 1, 2017, established a uniform approach for carriers in dealing with audit non-compliance (ANC) in states in which the filing was adopted. The new ANC rules allow the insured to attach an endorsement to the policy at inception which establishes a charge for non-compliance. The charge varies by state, but is often 200% of annual premium and is booked as additional policy premium when the charge is applied to the noncompliant policy. The goal of the ANC charge is to encourage cooperation with the premium audit as required by the policy contract, not to create a lasting increase in revenue. If the insured subsequently complies with the audit, the ANC charge is refunded back to the insured.

Any analysis of premium audit must consider the propensity of insureds to comply with audits as well as the effects of non-compliance and delayed compliance to the insurer’s revenue and cash flow. ANC charges are substantial relative to total annual premiums on the affected policies. These charges are quite likely to get the attention of the insured when billed, motivating the insured to reopen and complete the audit.

Because reopened audits commonly result in audit adjustments that are smaller than the ANC charge, particularly in states with charges of at least 100% of annual premium, the reversal of ANC charges can be expected to decrease the insurer’s revenue relative to when ANC charge was booked.

In a steady-state environment, the amounts of ANC charges and subsequent refunds across an entire large book of business will likely offset. In other conditions, patterns may shift in a way that may be material to the insurer’s evaluation of EBUB reserves and thus its quarterly financial statements. Operational changes, shifts in the economic environment, and non-uniform premium writings across the calendar year, to name just a few factors, can disrupt historical patterns. Accordingly, it is critical to measure, monitor, and forecast audit response rates as part of the audit premium forecasting process.

3. FINANCIAL REPORTING

U.S. statutory accounting principles (National Association of Insurance Commissioners 2001) require reporting entities to “estimate audit premiums, the amount generally referred to as earned but unbilled (EBUB) premium” and to “record the amounts as an adjustment to premium.” The EBUB estimate, typically representing a positive premium receivable asset, “may be determined using actuarially or statistically supported aggregate calculations using historical company unearned premium data, or per policy calculations.”

All respondents to the RWG survey indicated that their companies carry an EBUB estimate in their statutory financial statements, with four out of five stating that they review the provision on at least a quarterly basis.

Four out of five respondents rely upon at least one actuary in the estimation of these amounts. In three of these four companies, the actuary’s primary duty is reserving rather than pricing.

Blanchard (2005) describes how the EBUB estimate, also sometimes called an Earned but Not Reported (EBNR) premium reserve, is quite unique in that it represents an accrual of premium earnings against premiums which have not yet been charged or booked on a policy-by-policy basis. Audit premiums, while reasonably estimable across the coverage period in aggregate, are not billable to individual customers until after the audit is complete. The EBUB asset primarily represents an estimate of future receipts from audit premiums. The EBUB, whether expressed as written premium or as an increase in unearned premium, earns in proportion with the coverage term.

As audits are performed, resulting in completed audit adjustments and/or ANC charges, the actual results are booked into written and earned premium and a portion of the EBUB asset representing the expected audit is reversed. The difference between the actual and expected audit is realized as revenue at the time of the audit. When the EBUB estimate is determined on an aggregate basis rather than on a per-policy basis, the amount of expected audit to reverse out of EBUB each month is determined in aggregate as well.

Statutory accounting principles also require that all of the requisite liabilities associated with the asset, such as commissions and premium taxes, also be established against the EBUB asset. Furthermore, “ten percent of EBUB in excess of collateral specifically held and identifiable on a per policy basis shall be reported as a nonadmitted asset”. In the event that more than 10% is anticipated to be uncollectible, which may be the case in a severe economic recession, an additional write-off must be made.

As might be expected, the COVID-19 pandemic and resulting economic volatility caused a majority of companies surveyed to allocate more staff resources (headcount, time, or both) to analyzing audit premiums. Four out of five made meaningful changes to their analytical approaches.

Establishing and updating the EBUB provision on the balance sheet increases the likelihood that revenue recognition resulting from premium audit occurs at the most appropriate time, as the underlying coverage is provided. This goal will only be achieved to the extent that the EBUB has been thoughtfully calculated using all reasonably attainable information. If economic conditions or outlooks, and therefore the expected audit premiums, have significantly changed, the EBUB provision should be updated in a timely manner. Otherwise, the resulting change in revenue will not be realized until final audit, which may be much later than when the underlying cause of the change became known.

The next section describes one approach the actuary may use to estimate the EBUB asset in light of the many diverse factors which influence audits.

4. A Method for Forecasting Audit Premiums

While a detailed review of various approaches to forecast audits, and thus to estimate the EBUB, is beyond the scope of this paper, this section describes one method that has been found to work well.

Abbreviated sample exhibits, containing only a subset of the number of policy effective periods and development periods that would be used in a real analysis, are provided in the Appendix to aid in understanding each step. The values shown in the exhibits are fictional and are solely for illustration.

4.1. Aggregating the Data

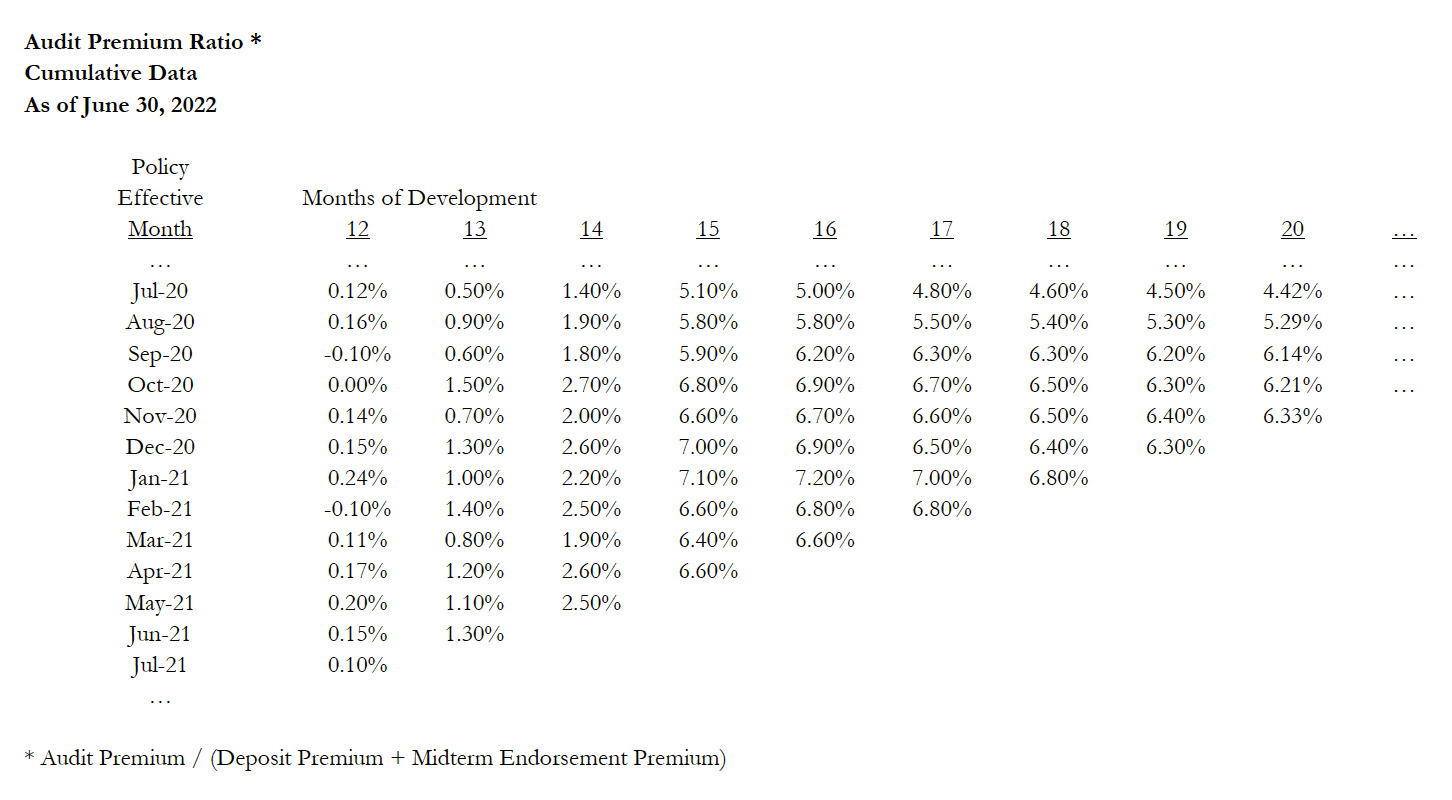

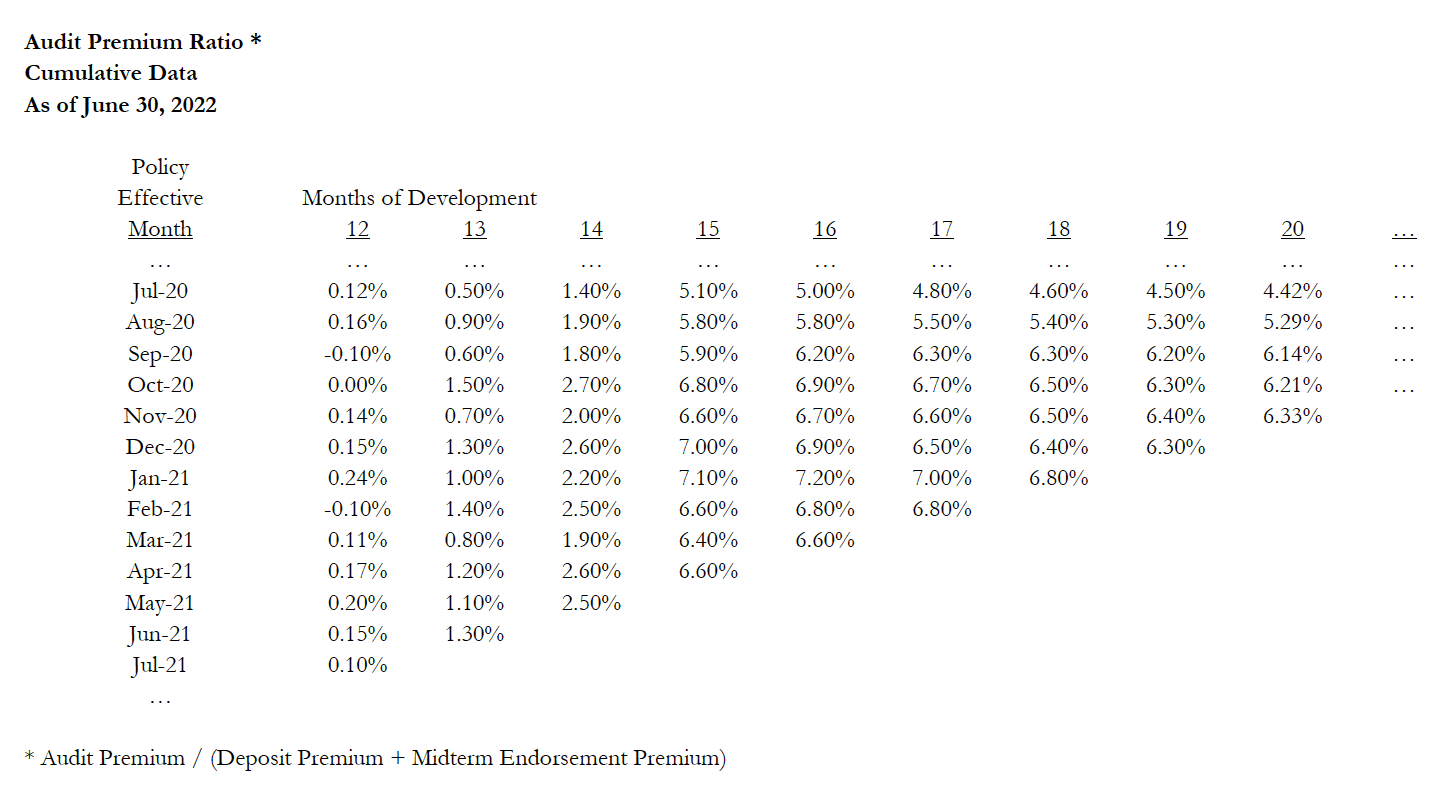

Since the audit premiums are directly related to the latest estimate of premium on auditable policies, representing deposit premium plus midterm endorsements, the actuary may wish to begin by building a triangle of historical data representing the ratio of audit premiums (inclusive of any ANC charges) to the sum of deposit and midterm endorsement premiums, organized by policy effective month and months of development since policy inception. (See Exhibit 1 of Appendix) Quarterly intervals may be used in place of monthly.

The cumulative value in development month 12 represents interim audits and audits on policies that were cancelled midterm.

Most premium audits are closed out within 30 to 90 days of policy expiration. This timeframe approximately corresponds to development ages 13 through 15 in the triangle. There may be a further processing or booking lag depending on the efficiency of the insurer’s systems.

Some audits, whether completed or closed out with ANC charges, will be reopened if the insurer permits. There may be a time limit after which the audit cannot be reopened. The reopening of an audit is generally initiated by the insured or its representative. A reopen involves providing new information regarding the insured exposures, correcting information previously provided, or otherwise disputing the result of the audit. Once reprocessed, these reopened audits are more likely to result in refunds back to the insured than in additional premium due. The impact of these transactions on the sample data can be seen as decreases in development ages 16 and subsequent.

A reasonable alternative to the aggregation described in this step would be to include audit premiums in the denominator, alongside the deposits and endorsements. This would create a triangle of audit premiums to ultimate premiums. The remainder of the steps in the forecasting method would be revised slightly to reflect this change. One advantage to the alternative framework would be that the audit-to-ultimate ratio can directly smooth out any shifts in the under- or over- estimates of the initial deposit premium, possibly resulting in better predictive value without having to make adjustments for operational changes. One disadvantage is that the denominator would no longer be final after 12 months due to the presence of audit premiums, which would introduce estimation error and a degree of circularity into the process.

4.2. Estimating Premium Development

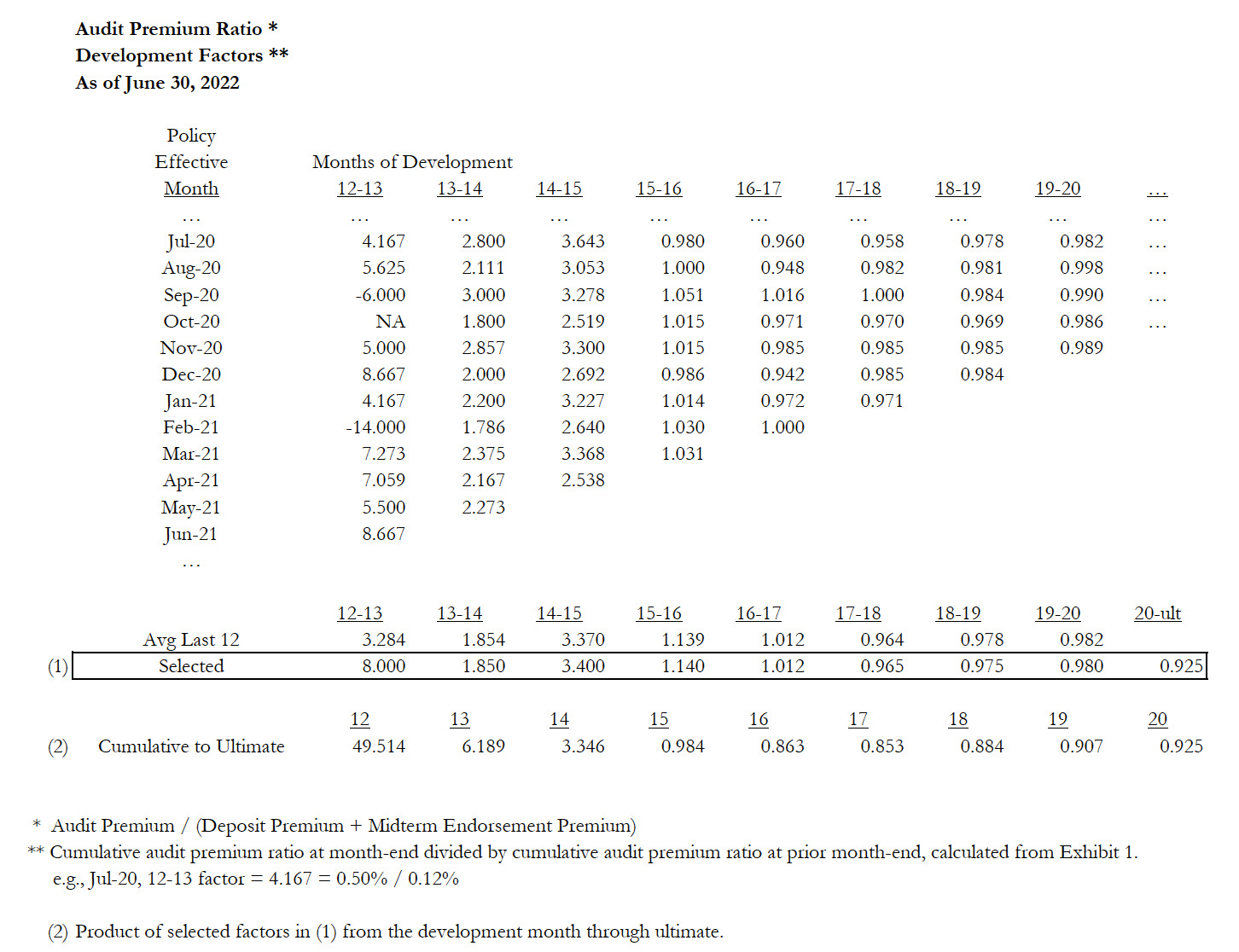

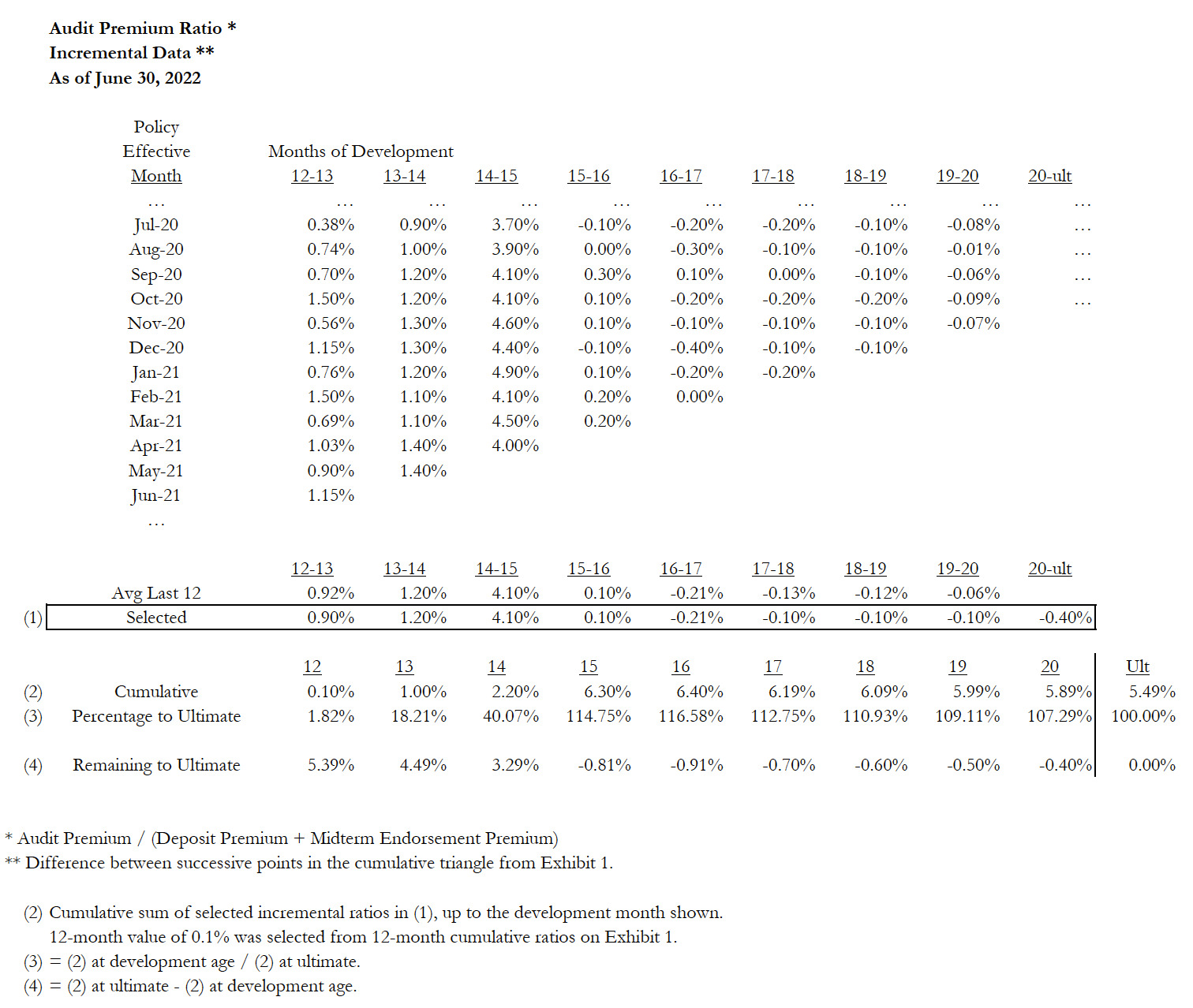

Once the triangle is ready, the actuary can estimate premium development patterns from the triangle. The patterns can be expressed as ratios of cumulative values (Exhibit 2 of Appendix) as in the chain ladder method, or as differences between development ages as in the incremental loss development method (Exhibit 3 of Appendix). The incremental approach is easier to work with when the sign of the data (positive or negative) varies across a given row or column.

To the extent that operational changes have occurred, such as those discussed in section 2 of this paper, the actuary may need to develop and apply adjustments to the historical data in an attempt to bring older data points to a basis that is more consistent with current operations. These adjustments may be substantial and critical to the proper performance of the method if operational changes have been significant across time. Alternatively, a shorter-term average may be used in the selection of the premium development pattern or the ultimate audit ratio if the volume of data is sufficiently large to rely upon.

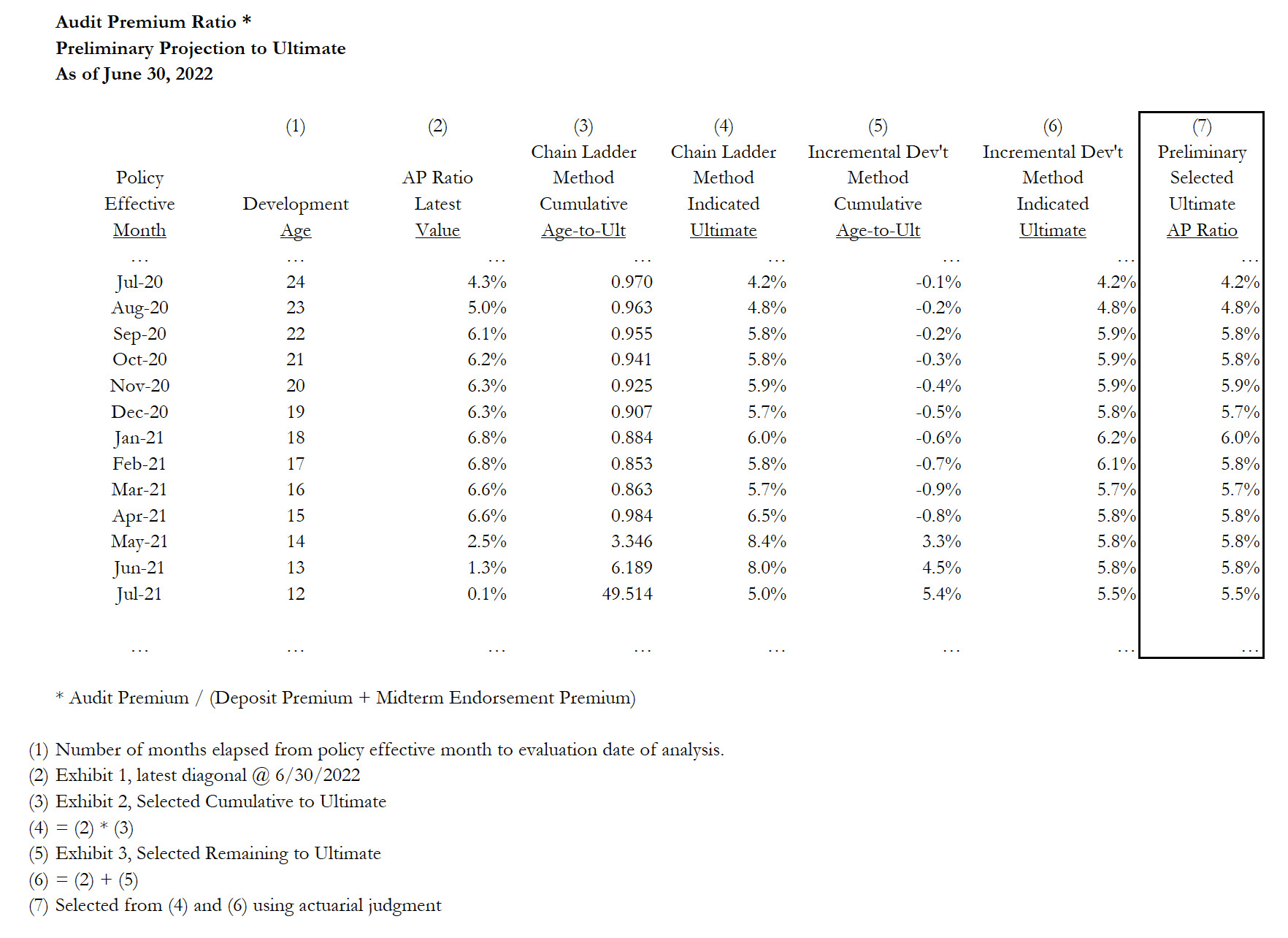

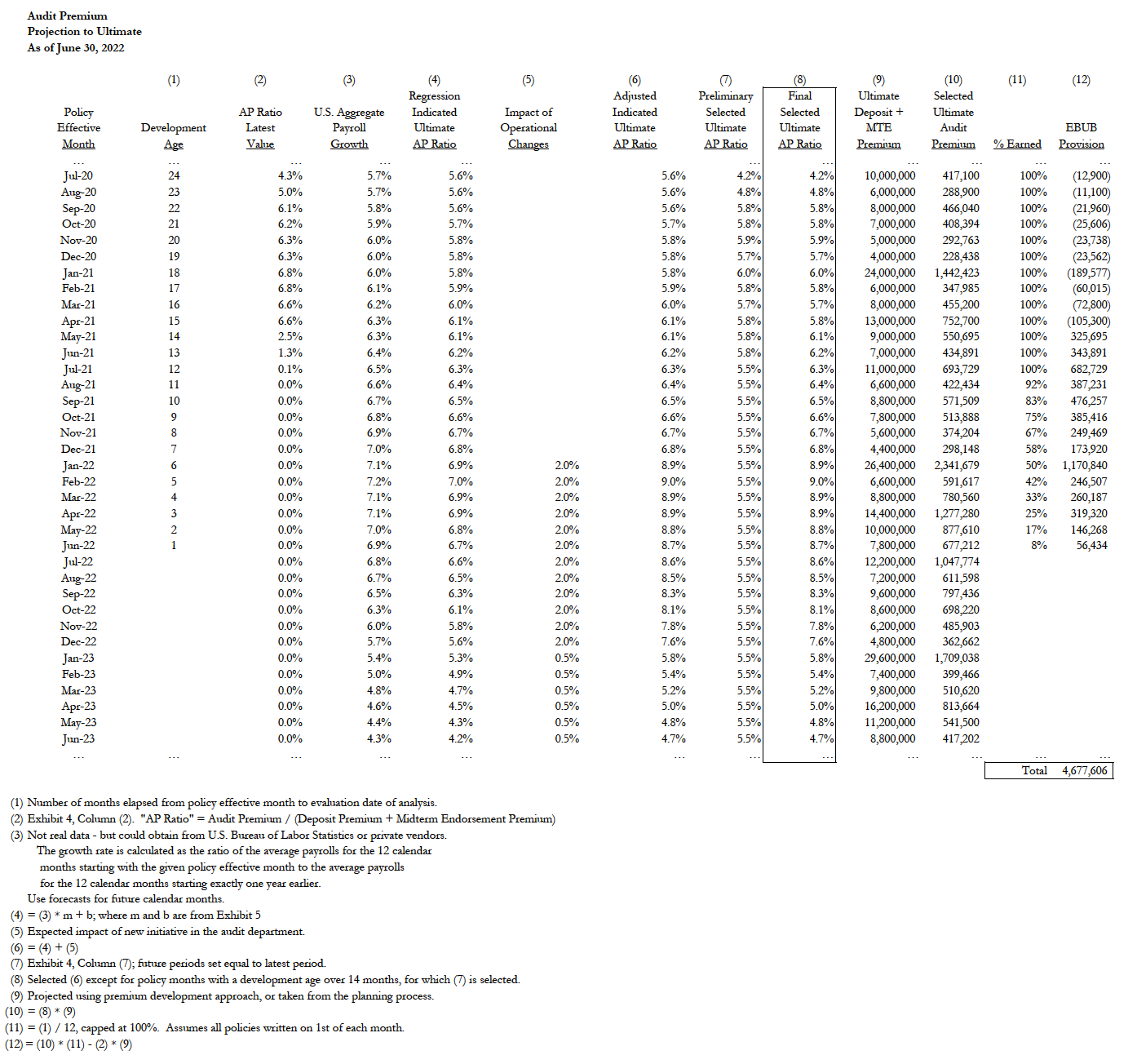

The patterns resulting from the previous step can be used to directly estimate the ultimate audit ratio for policy effective months up to the evaluation date of the analysis (Exhibit 4 of Appendix).

4.3. Incorporating Economic Data and Forecasts

The approach taken thus far has a substantial shortcoming. For policy month cohorts in which most or all policies have yet to be audited, the forecast will be a simple average or other selection that does not vary across policy months. This implies a consistent exposure growth rate across the entire forecast period, rather than considering economic factors that influence exposure growth.

The quantity being estimated, the ratio of audit to deposit plus endorsement premiums by policy month, is a measure of the growth of the exposure base among the company’s policyholders. This growth rate can be expected to correlate with the annual growth rate of a similar exposure base that is measured in economic statistics on a national or regional level and is forecasted by economic research firms.

Publicly available economic data such as: the number of employed persons, aggregate hours worked, average hourly earnings, or gross domestic product — or some combination of the above — are likely to correlate with changes in the exposure base for the insurer’s portfolio. If the portfolio is skewed towards a particular economic sector, such as manufacturing, one may seek data specific to that sector. Some private firms also provide specialized economic data which could be a better match to the portfolio.

One possible approach to integrate economic data into the analysis is outlined below.

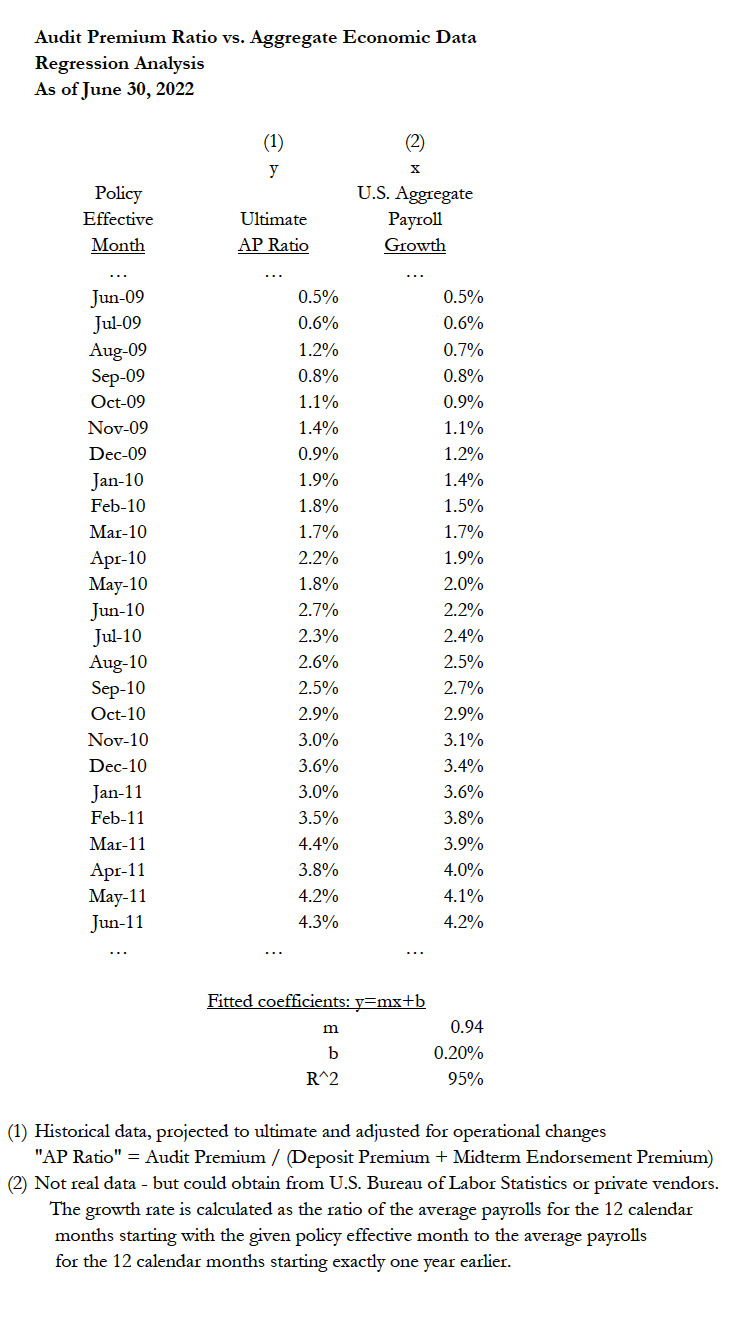

First, conduct a simple linear regression of the ultimate ratio of audit to deposit plus endorsement premiums against the economic series to assess correlation across time. The historical time period utilized should be as long as reasonably possible, covering at least one complete recession and recovery, as well as a wide array of economic conditions. Otherwise, the results are likely to lack predictive power.

Exhibit 5 of the Appendix contains an example, showing only a small subset of policy months.

If a good fit is obtained, then proceed to gather monthly forecasts of the economic series for future calendar periods. The forecasts could be point estimates representing the outcome believed to be most likely, or could be a range of outcomes under various scenarios (e.g., accelerating growth, steady growth, or recession). Three of five respondents to the RWG survey indicated they use multiple scenarios in their audit premium forecasting process.

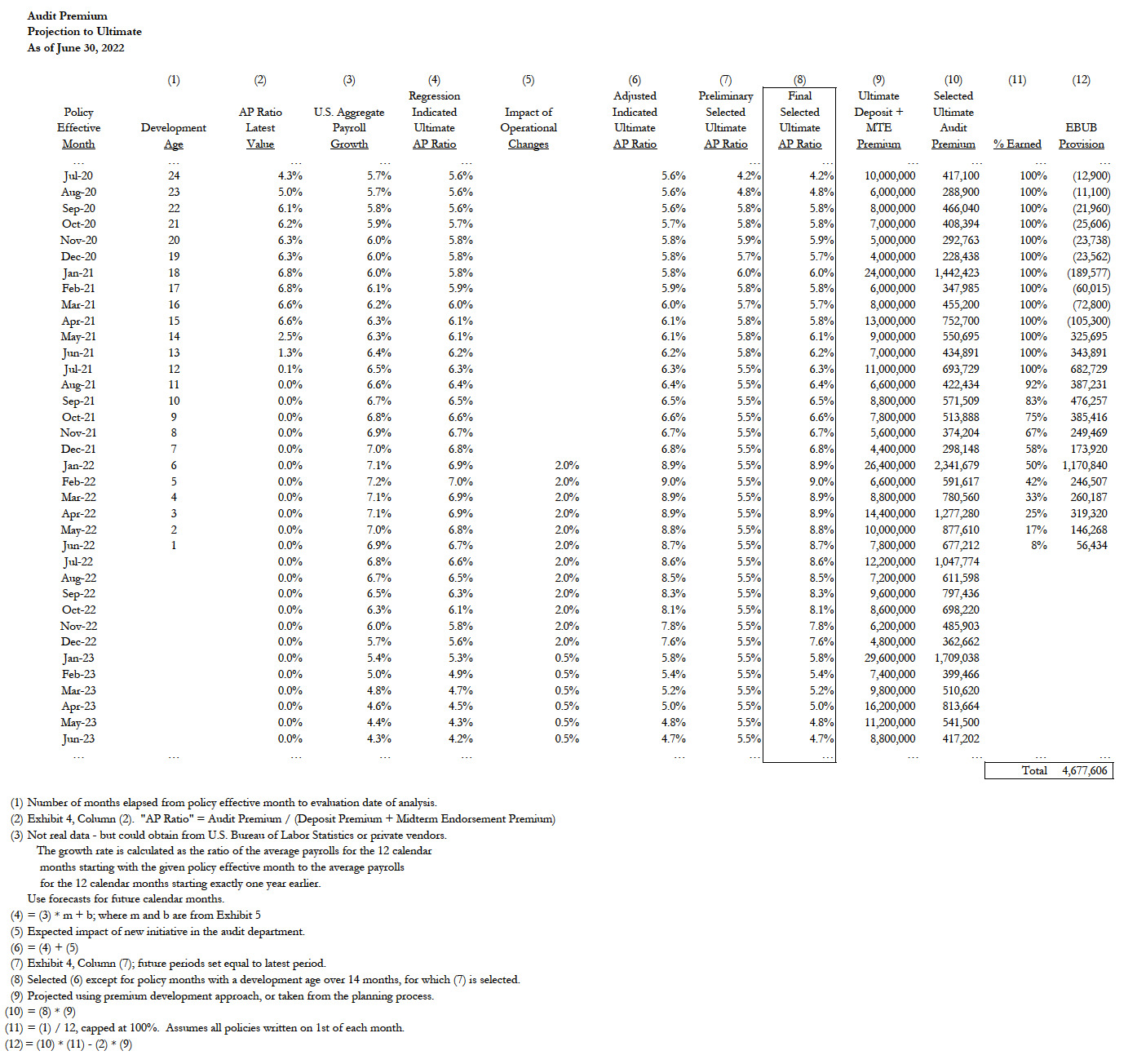

Then, apply the regression model to the forecasts to derive an estimate of the ultimate audit ratio by policy effective month. Exhibit 6, Columns (1) through (4), of the Appendix illustrates this approach.

In the example, the premium audit department has scheduled an operational change to begin on January 1, 2023 with any policies written on or after January 1, 2022. An example of such a change could be implementing a new predictive model with the goal of identifying policies in need of a more comprehensive form of audit and thus to more accurately capture the true exposure. The impact of this initiative on the ultimate audit ratio is assumed to be +2.0%. Once a full calendar year has elapsed, the impact is assumed to diminish to 25% of its initial value. The insurer believes the other 75% of the impact will then be applied to in-force policies as an endorsement. Column (5) of Exhibit 6 displays the impact on audits, which is then combined with the forecast from the regression model to produce the indicated ultimate audit premium ratio in Column (6).

This forecast will be preferable to the development methods for policy months in which most audits have not yet been completed. In the example, this is development months 14 and below. For older policy months, the development-based estimates shown in Column (7) will be more accurate because most of the remaining activity will be reopened audits. The development methods directly utilize the data on the completed audits to-date, which are likely to correlate with the outcomes of subsequently reopened audits on that same policy month. Column (8) illustrates the final selections.

The ultimate deposit and endorsement premiums, Column (9), will be known at or slightly after 12 months of development. Prior to that point, they can be estimated using various approaches such as a monthly chain ladder method. The product of the audit premium ratio and the ultimate deposit and endorsement premiums gives the indicated ultimate audit by policy effective month in Column (10).

4.4. Calculating the Premium Audit Component of the EBUB Provision

Multiplying the ultimate audit premium for each policy effective month by the percentage earned as of the evaluation date, then aggregating across all policy effective months that have incepted, will produce an estimate of the EBUB provision as of the evaluation date. See Exhibit 6, Columns (11) and (12).

In the example, it is assumed that all policies begin on the 1st of each month. As a result, the percentage earned is 1/12 for the most recent policy effective month, 2/12 for the next, and so on up to 12/12. One could instead use a mid-month assumption or a more precise calculation.

It is recommended to extend the forecast period to policy effective months beyond the evaluation date, as has been done in Exhibit 6. This allows the forecasting of audit premium by calendar month for future years, in the next step of the process. These forecasts may be useful in the insurer’s financial planning exercises.

In practice, there may be other components of EBUB besides audit premiums, such as processing lags related to cancellations. Those are outside the scope of this paper.

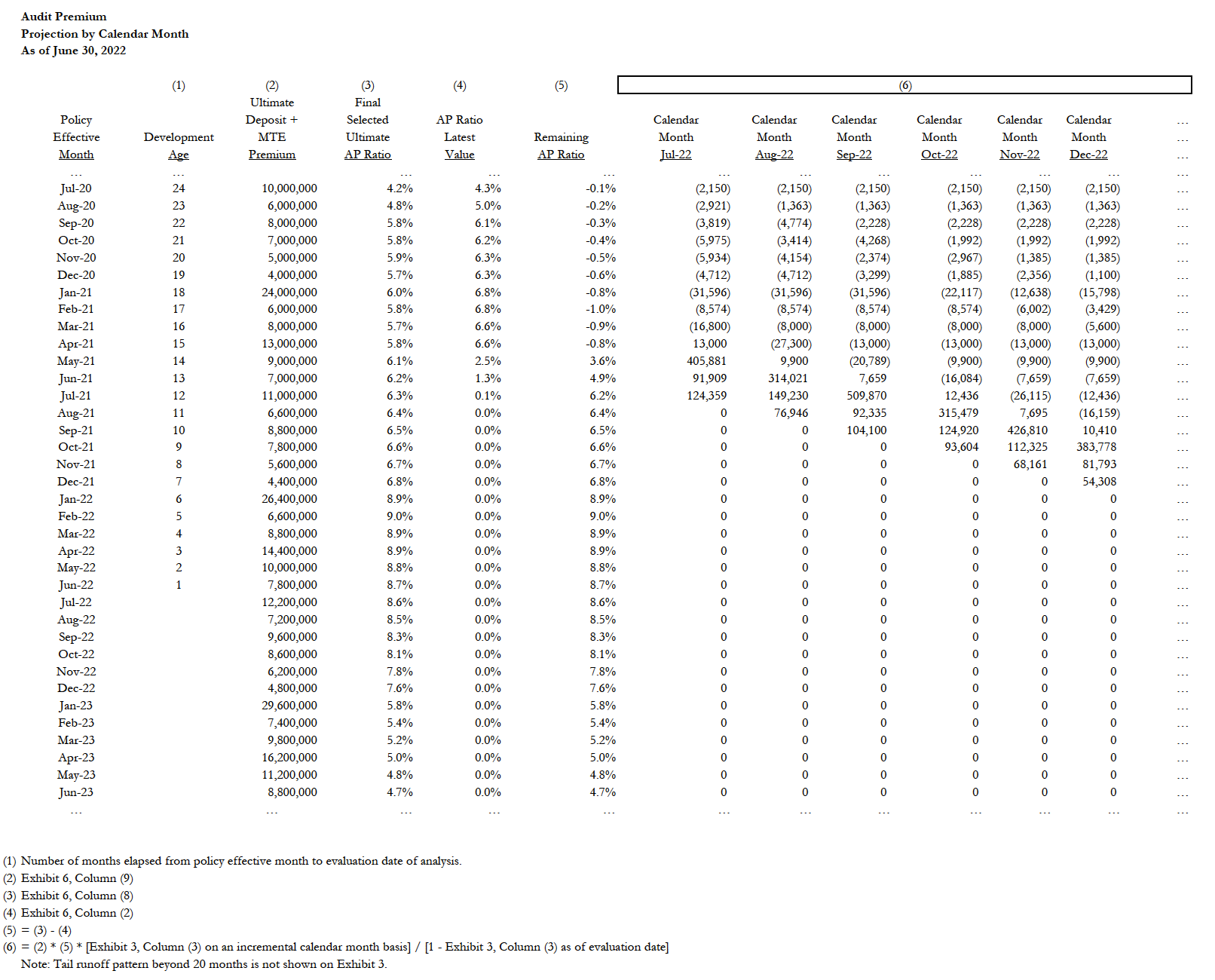

4.5. Calendar Month Forecasts

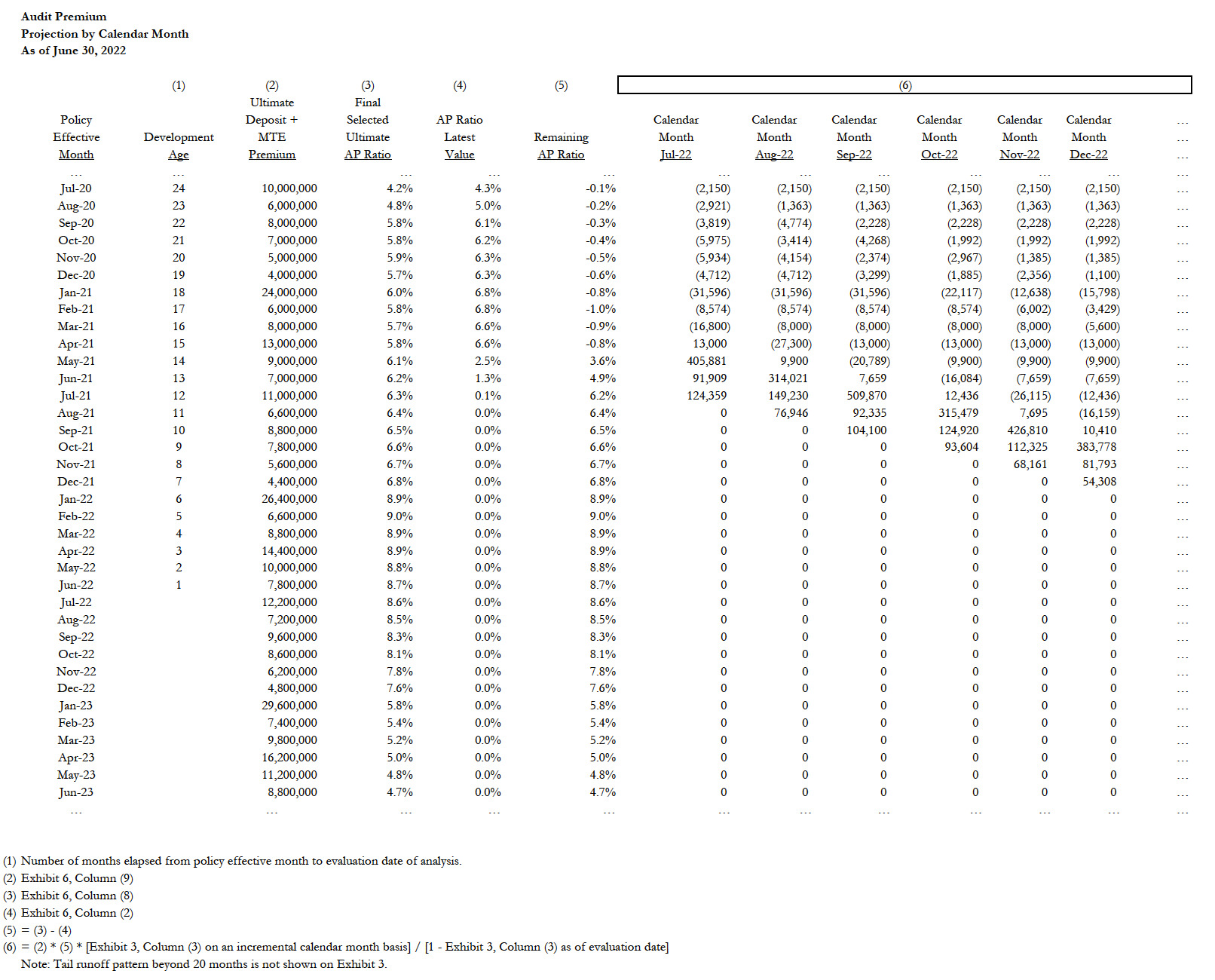

The estimates of ultimate audit premium produced in the prior step can be allocated to calendar months using the development patterns selected earlier in the analysis. See Exhibit 7 of the Appendix for an example.

The resulting forecasts by calendar month can be used in an actual-to-expected method to monitor monthly audit receipts against expectations. The difference between actual and expected can be used to help refine or update assumptions the next time the actuary completes their analysis. Calendar months beyond the next analysis date will have value in the insurer’s financial planning framework.

5. IMPACTS ON LOSS RESERVING AND TREND MONITORING

Changes in premium audit will impact the loss reserving process to the extent that metrics involving exposures or premiums are used. One such metric commonly in use is claim frequency, which can be expressed as the ratio of claim counts to exposures or to premium.

When policies are subject to audit, exposures and premiums are not known with certainty until well after the completion of the policy term. An insurer that waits until exposures or premiums are fully audited and final to get reliable estimates of claim frequency will not be able to react in nearly as timely a manner to emerging trends as an insurer that evaluates its claim frequency on a monthly or quarterly basis using a good quality forecast of audited exposures. Therefore, it will be subject to a competitive disadvantage in the marketplace.

Furthermore, if the insurer relies upon the frequency/severity method to estimate loss reserves for the most recent accident year or two, it will be critical to have accurate claim frequency statistics. If audit premium forecasts miss the mark, additional error will have been introduced into the reserving process.

5.1. Illustration

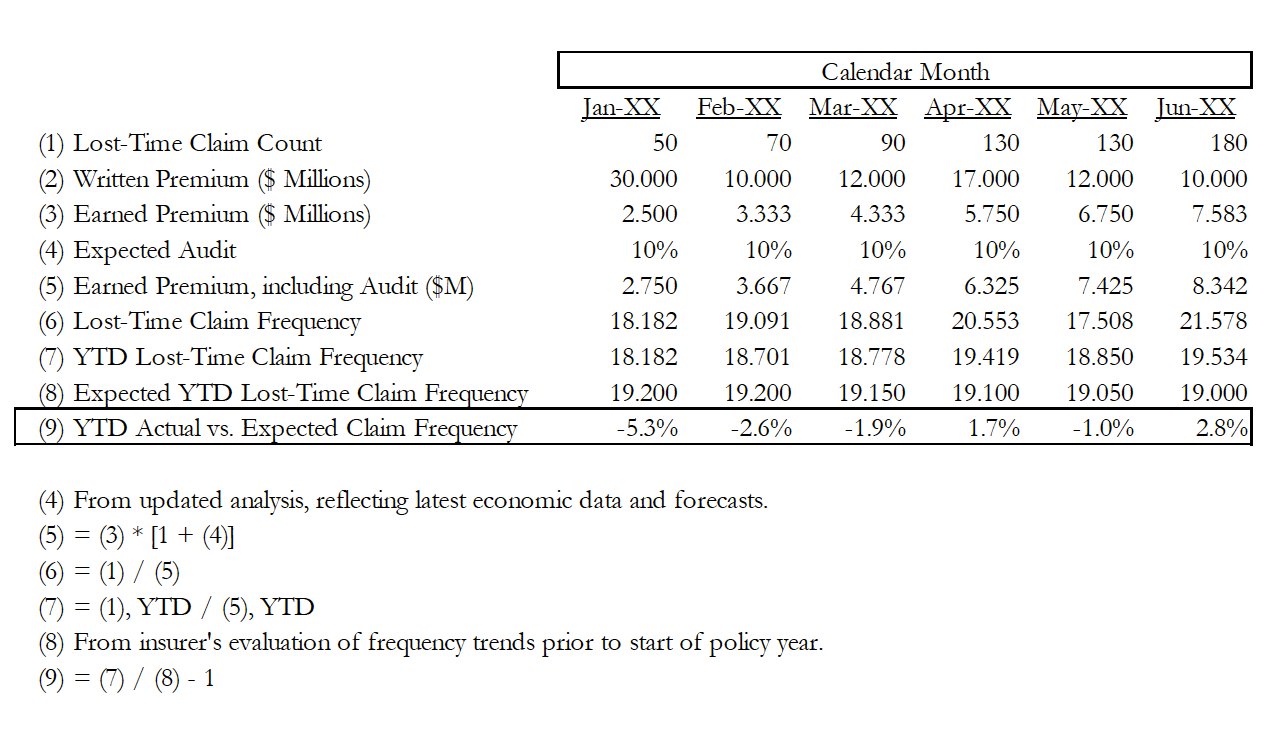

The following illustration highlights the pitfalls of drawing conclusions from claim frequency without an accurate forecast of audited exposures.

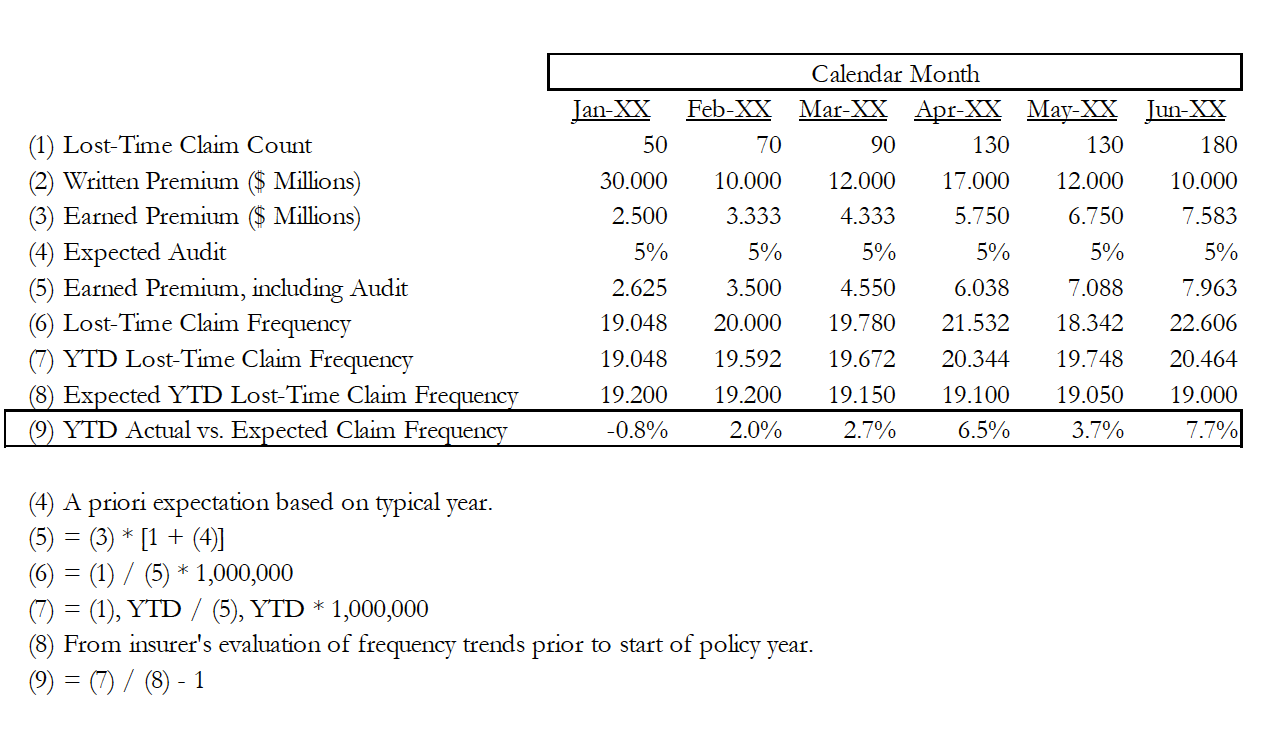

In Table 1, the actuary has calculated the company’s WC lost-time claim frequency for policy year 20XX and has compared it to an a priori expectation. They have loaded in a 5% audit factor to the earned deposit premium without giving it much thought, because they have seen audits come in at this level for many years in a row.

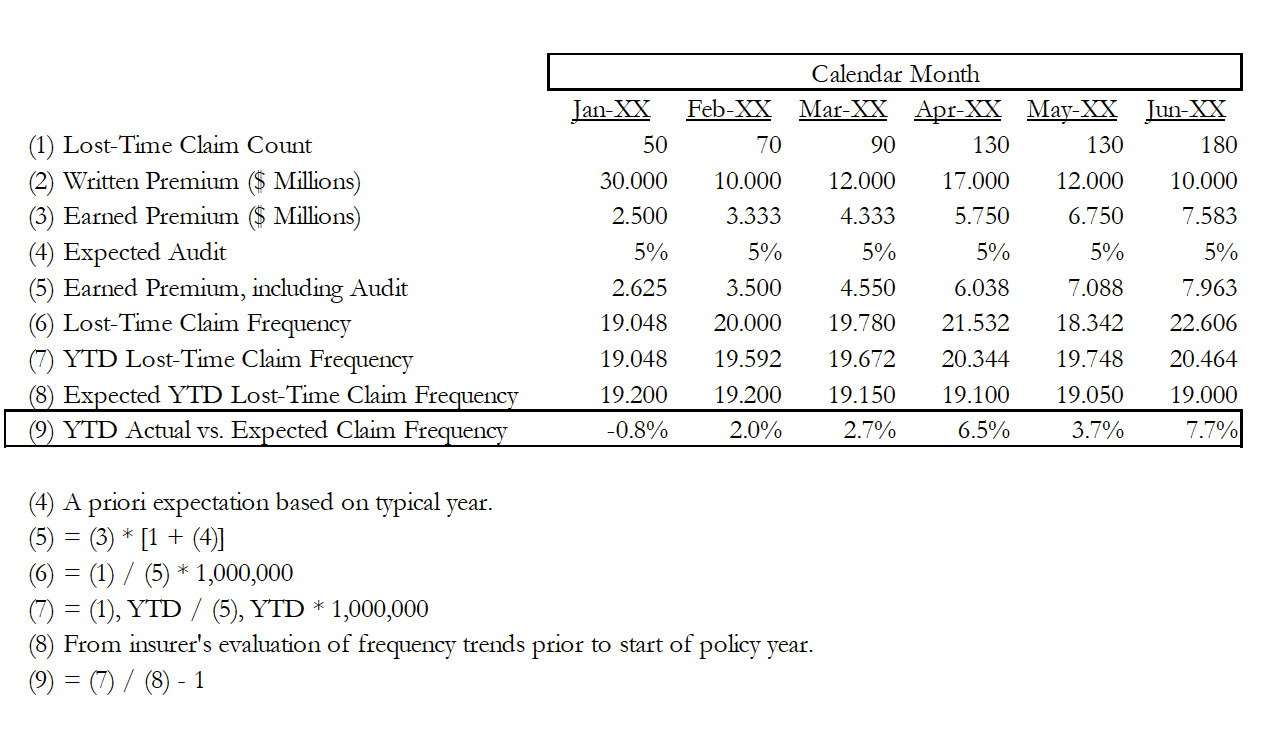

The actual results are above the expected by a high single-digit percentage at mid-year — a big concern for any WC carrier who has become accustomed to flat or declining frequency. Upon observing this, the actuary would embark on further review which might lead them to recommend selecting a higher frequency in their frequency/severity method. This could cause an increase to the accident year 20XX loss ratio, and thus to the company’s loss reserves. They would also share the results with the pricing actuary, who might conclude that the company should slow its growth or seek to exit certain segments of its book.

Examining further, there may not actually be a problem for the insurer. The actuary recalls hearing in the financial media that the economy is growing at a good clip, with rapidly increasing inflation in the prices of goods and services. Even wages are rising at a faster rate than they have in over a decade.

Hypothesizing that audits could increase with inflation, the actuary completes an analysis of audit premiums using an approach like the one in Section 4. The analysis incorporates the higher levels of inflation and growth that are taking place in the economy and are forecasted to continue for at least the next several months. Based upon this work, the actuary raises their estimate of the expected audit ratio from 5% to 10%.

Returning to the frequency calculations, now including the higher expected audit ratio in Table 2, the actuary sees that frequency is much closer to expectations than they initially thought. They will continue to monitor, but June’s elevated reading may be just one unlucky month.

5.2. Examples from Recent Recessions

The NCCI completes a WC frequency analysis each year that is watched closely by industry observers. They define claim frequency as the number of lost-time claims per $1M of pure premium at current wage and voluntary cost level.

During the Great Recession of 2007-2009, the annual change in frequency as measured by NCCI remained stable and consistent with the preceding eight years, in the low negative single-digits (averaging around -4% per annum). In 2010, the first full year of recovery after the recession ended, frequency suddenly spiked to 10.6% above 2009 levels.

What could explain this sudden surge in measured frequency? Many carriers did not update their EBUB (NCCI uses the term EBNR) provisions during the recession, instead only displaying lower premiums in 2010 when audits finally completed on policies which had seen exposures fall during the recession (Lipton 2020). The understated 2010 premiums, accompanied by overstated 2008 and 2009 premiums, went into the denominator of the frequency formula.

If premiums were restated to reflect timely updates to EBUB provisions, then it would have been evident that the 2008 and 2009 frequency changes were not as favorable as otherwise indicated, and that 2010 was less adverse than indicated by over 6 percentage points (according to the NCCI estimate). Adjusted frequency remained positive for 2010, but only due to an industry group mix change.

The next recession in the United States did not occur until 2020, and it lasted only two months according to the National Bureau of Economic Research (National Bureau of Economic Research, n.d.). If insurers improved their processes around EBUB estimation during the 11 years between recessions, it may not be as evident from annual statistics this time around, for two reasons in particular. First, the COVID-19 recession was so much shorter than the Great Recession that annual intervals may mask some of the impacts. Second, there were significant changes in the ways people worked during the pandemic that would likely have impacted claim frequency to some extent.

Nonetheless, the NCCI continued to adjust the data in their 2022 State of the Line Guide (National Association of Insurance Commissioners 2022) to reflect the impact of changes in audit activity in the 2019-2021 time period. While details of the adjustment are not provided, the fact that the NCCI saw it necessary to continue adjusting the data would suggest that carriers once again did not update their EBUB provisions to the extent that would have fully captured changes in the economy. Even after adjustment, the 2020-2021 claim frequency shows a pattern that mirrors what was seen in the Great Recession. NCCI calculates a 7.6% decline in 2020 and makes a preliminary estimate of a 7% increase in 2021. Both values are well outside the -1% to -6% range that was seen in the preceding years.

6. CONCLUSION

Premium audits contribute meaningfully to the financial results of P&C insurers, especially those who write workers’ compensation. Some carriers already use actuaries to help estimate premium audits, but there is an opportunity for actuaries to play a larger role. Actuaries can apply their skills to the estimation of the EBUB provision as well as in forecasting audit premiums over a longer period of time for planning purposes. Trend monitoring and loss reserving also involve making assumptions about premium audit, whether or not these assumptions are explicitly specified or stress-tested. By conducting a thoughtful analysis of premium audits, actuaries can help insurers improve the quality of their financial reporting and planning, trend monitoring, and loss reserving.