Introduction

Loss and loss adjustment reserves are essential in the insurance industry as they represent funds set aside by insurers to cover potential future payments on claims that have occurred and may or may not have been reported as of evaluation date, ensuring their ability to fulfill obligations to policyholders. Accurate reserve calculations are paramount, as inaccuracies can lead to financial instability, and reputational damage to insurers.

In light of recent hurricane activity, it has become evident that traditional catastrophe reserving techniques do not fully incorporate underlying loss drivers, resulting in inaccuracy in reserving. This paper addresses the necessity of bifurcating catastrophe risk into systematic (inherent to the event) and unsystematic (operational) root causes to provide a more comprehensive approach to actuarial loss reserving, improving accuracy and enhancing preparedness in managing catastrophic risks.

Reserving for catastrophic events in property insurance presents a unique set of challenges for actuaries. Unlike routine claims, catastrophes are infrequent, geographically concentrated and exhibit immense variability in size and intensity. This complexity renders traditional reserving methods based on historical data less reliable as predictors of future losses, demanding actuarial expertise in alternative approaches.

Tailored for actuaries and property insurance specialists, this paper delves into the realm of catastrophe reserving. It commences by examining traditional methods employed in catastrophe reserving, highlighting their strengths and weaknesses. Subsequently, it introduces an innovative approach to catastrophe reserving, delineating its fundamental components and principles. Furthermore, it furnishes a comprehensive implementation guide alongside practical applications. This paper addresses various practical considerations inherent to catastrophes, including the state legislative environment and company claims practices, providing valuable insights for achieving more accurate estimates.

The Traditional Approaches to Catastrophe Reserving

Reserving actuaries segregate the analysis of catastrophic and non-catastrophic claims for several reasons. First, combining these claims can distort development patterns. Development triangles assume an even distribution of loss dates throughout the accident periods, which is not applicable to catastrophic events. Loss dates in such events tend to be clustered around a specific day or week. Additionally, the high volume of claims and limited access to affected areas immediately after the event can lead to delays in claims reporting and processing. Given these reasons, it’s not advisable to use development triangles for non-catastrophic claims to estimate the development of catastrophic claims.

The second reason for separately reserving for catastrophic events pertains to reinsurance. Insurance companies are obligated to report estimated ultimate losses by event to reinsurers shortly after the event occurs, forming the basis for anticipated reinsurance recoveries to be funded by the reinsurer. The recent reinsurance crisis is, in part, attributable to increasing ultimate losses (i.e., adverse development) on prior catastrophic events with each valuation, requiring reinsurers to leave risk collateral on account for the past events beyond their expectation. This situation leaves them with uncertainty regarding the capital available for the subsequent reinsurance year.

Generally, actuaries employ several reserving techniques to estimate ultimate catastrophe losses. In the immediate aftermath of a hurricane, modeled losses often serve as the first, readily available estimate for ultimate losses. This approach, frequently endorsed in actuarial literature, presents several limitations. First, models rely on simulated past events similar to the modeled event, rather than the actual event itself. This inherent uncertainty leads to a wide range in potential loss estimates. Secondly, existing models fail to fully account for social inflation, the rising trend in litigation costs and jury awards, which has significantly impacted recent catastrophe payouts. Additionally, modeled losses lack transparency as they do not provide insights into the underlying drivers of losses, thus limiting their implications for the development of claims handling strategies.

The main purpose of catastrophe models is not to predict losses at a location for a given event, but rather to provide reliable estimates of potential losses to properties or portfolios of properties from future catastrophe experience, and to effectively differentiate the vulnerability of properties in different regions.

Modelers have the capability to reconstruct the specific event, allowing for the estimation of losses based on the actual scenario. While this approach typically offers a more accurate estimate compared to using “similar” simulated events, the reconstruction process requires time, which may delay the availability of the estimate. It is worth noting that this method inherits the limitations and downsides associated with modeled losses, including potential underestimation and a lack of transparency regarding the underlying drivers of losses.

Actuaries may also compare current events to historical events experienced by their company as a benchmarking technique. However, this method can lead to inaccuracies in estimates due to the infrequency and varying severity of catastrophic events.

This paper tackles the challenge of catastrophe reserving by proposing a novel methodology. This approach prioritizes simplicity and transparency, ensuring easy comprehension for both internal stakeholders like business leaders and external partners like reinsurers. Importantly, this methodology shines in its ability to deliver accurate ultimate loss estimates for hurricanes immediately after landfall, while simultaneously pinpointing key loss drivers. This actionable insight empowers risk management decisions and strengthens financial preparedness for future hurricane events.

Originally developed for hurricane reserving, this methodology can be extended to other catastrophic events.

Frequency-MDR Reserving Methodology

Systematic vs Unsystematic Risks

Before we dive into the intricacies of the Frequency-MDR reserving methodology, let’s first explore the root causes behind the continuing adverse development in ultimate loss estimates for catastrophic events. Insurance companies point to a phenomenon known as social inflation as a significant driver behind the prolonged claims development. Specifically, they list the assignment of benefits, solicitation by roofing contractors, the involvement of public adjusters, and the uptick in lawsuits and associated litigation expenses. Various regulations have also historically contributed to a challenging environment for insurers, especially in Florida. Given that a substantial portion of losses is passed on to reinsurers, insurance companies may sometimes focus less on gross estimates, potentially leading to ongoing adverse development. This “loss creep” effect surged into prominence around 2016 and was further amplified in the aftermath of Hurricane Irma’s devastating impact on Florida.

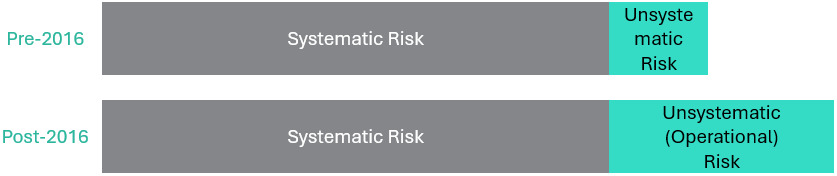

Like other reserving methods, the Frequency-MDR methodology operates most effectively in a stable environment. Therefore, we will begin by dividing hurricane risk into two components: a relatively stable systematic risk inherent to a catastrophic event itself, and variable risk associated with efficiency in insurance company operations.

The systematic component primarily entails catastrophe risk, or damage from hurricane winds, which can be extensively modeled but is beyond the control of insurance companies. On the other hand, the unsystematic component relates to company operational risk, characterized by more limited modeling capabilities. However, insurance companies can undertake measures to mitigate this risk. Unsystematic, or operational, risk largely represents the effect of social inflation as well as deficiencies in insurance company operations and stands as a major contributor to “loss creep” and underestimated reserves.

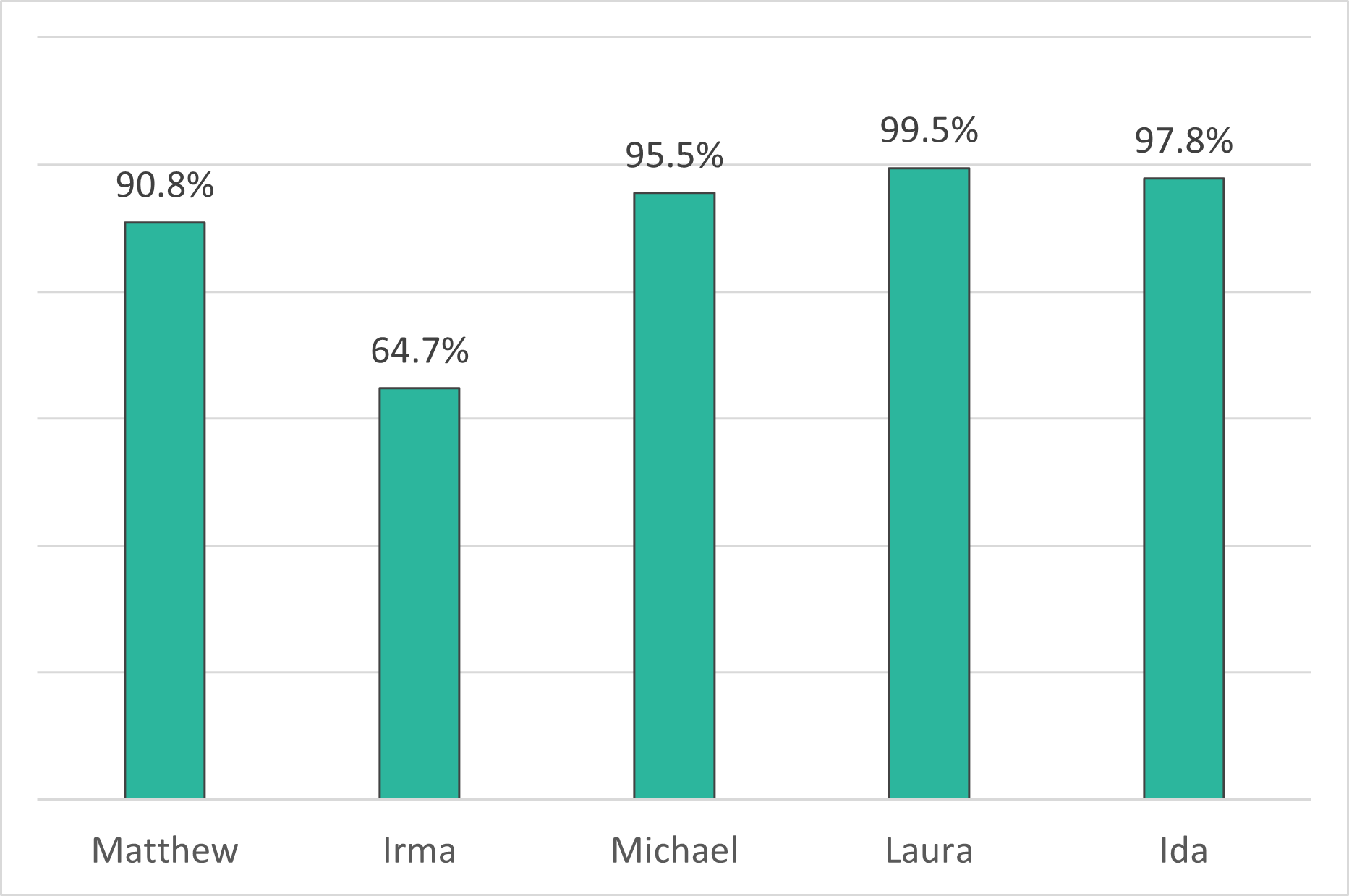

Recognizing that hurricane damage may go unnoticed for months or even years after the storm, we still operate under the assumption that a significant portion of late-reported claims stem from solicitation by roofing and other contractors. It is common for these claims to involve public adjusters and become embroiled in legal disputes. Consequently, the reporting lag serves as a useful tool in distinguishing between systematic and unsystematic risks. Below is a graph illustrating the percentage of ultimate claims reported weekly since landfall for five hurricanes that impacted Florida and Louisiana: Matthew (2016, FL), Irma (2017, FL), Michael (2017, FL), Laura (2020, LA), and Ida (2021, LA).

It has been observed that claims reporting tends to decelerate and stabilize around the 90 to 120-day mark. Therefore, we will employ a cutoff of 90 days as a distinction between the two types of risks.

Dividing the entire hurricane risk into two distinct components and analyzing them separately will increase the accuracy of the estimate.

Reserving for Systematic Risk

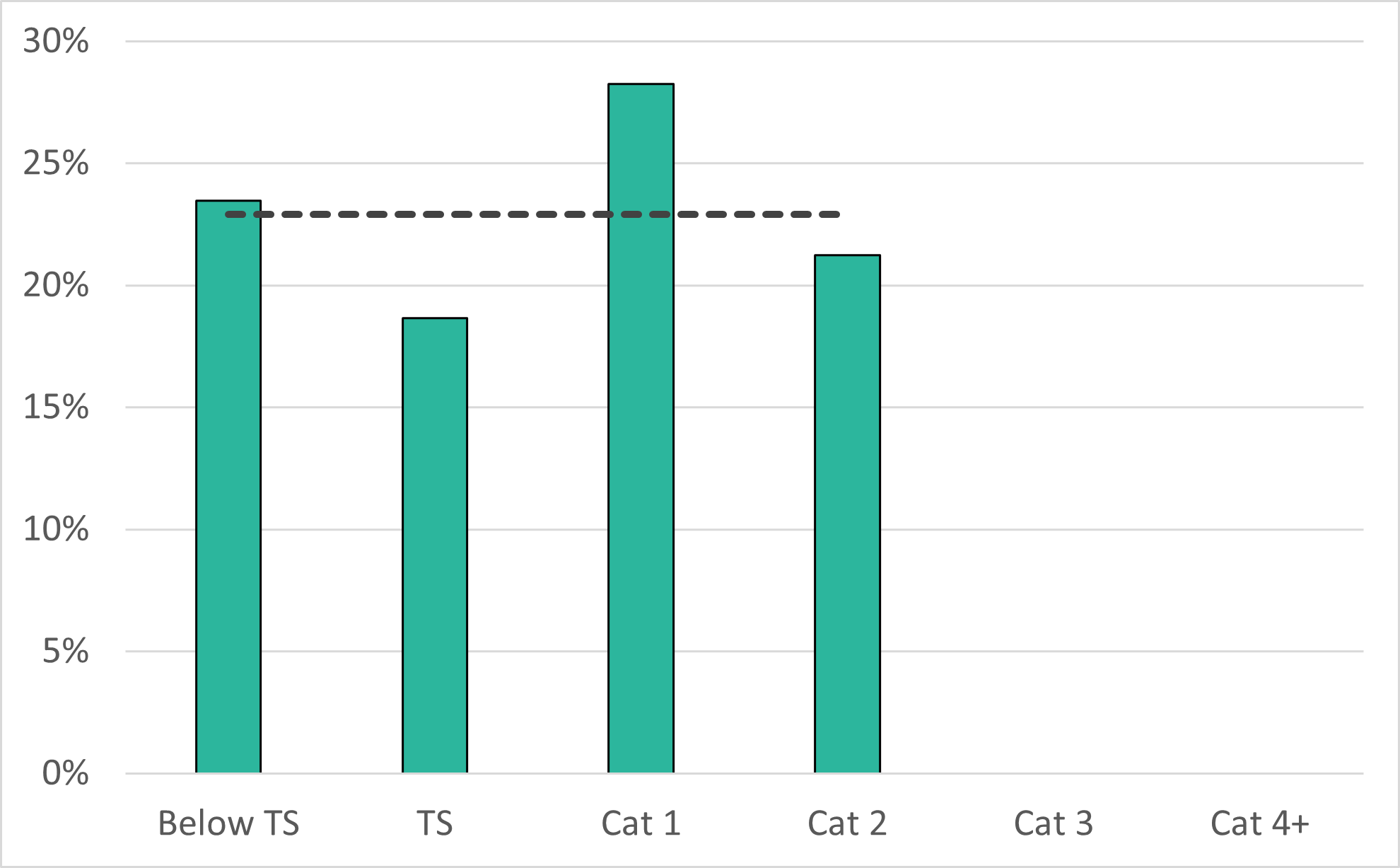

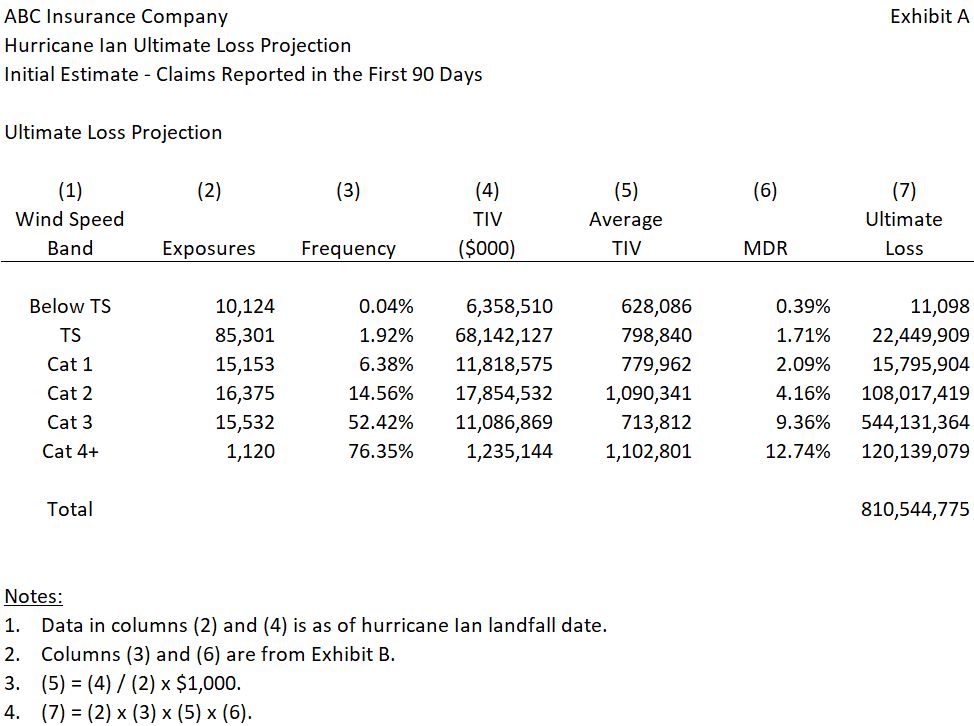

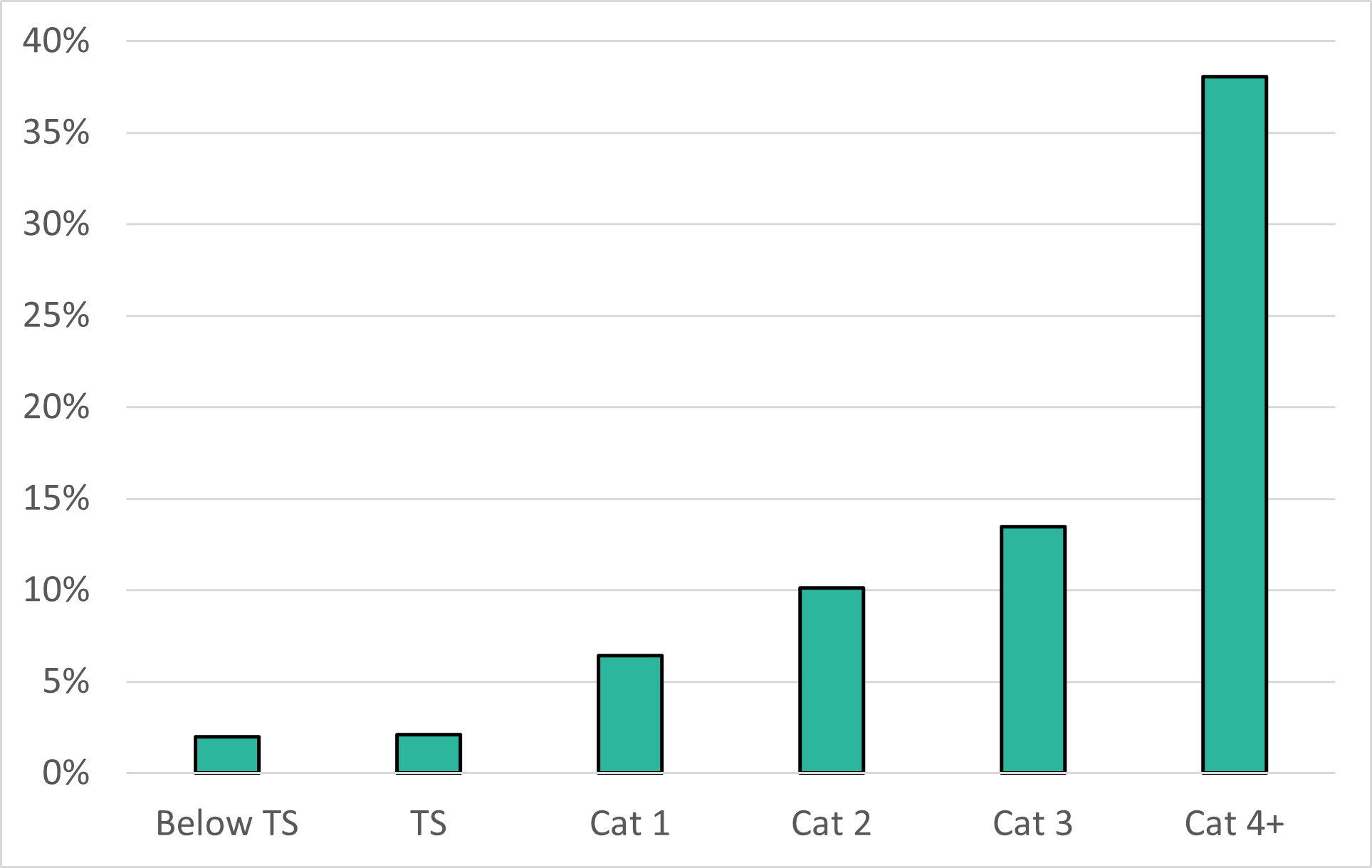

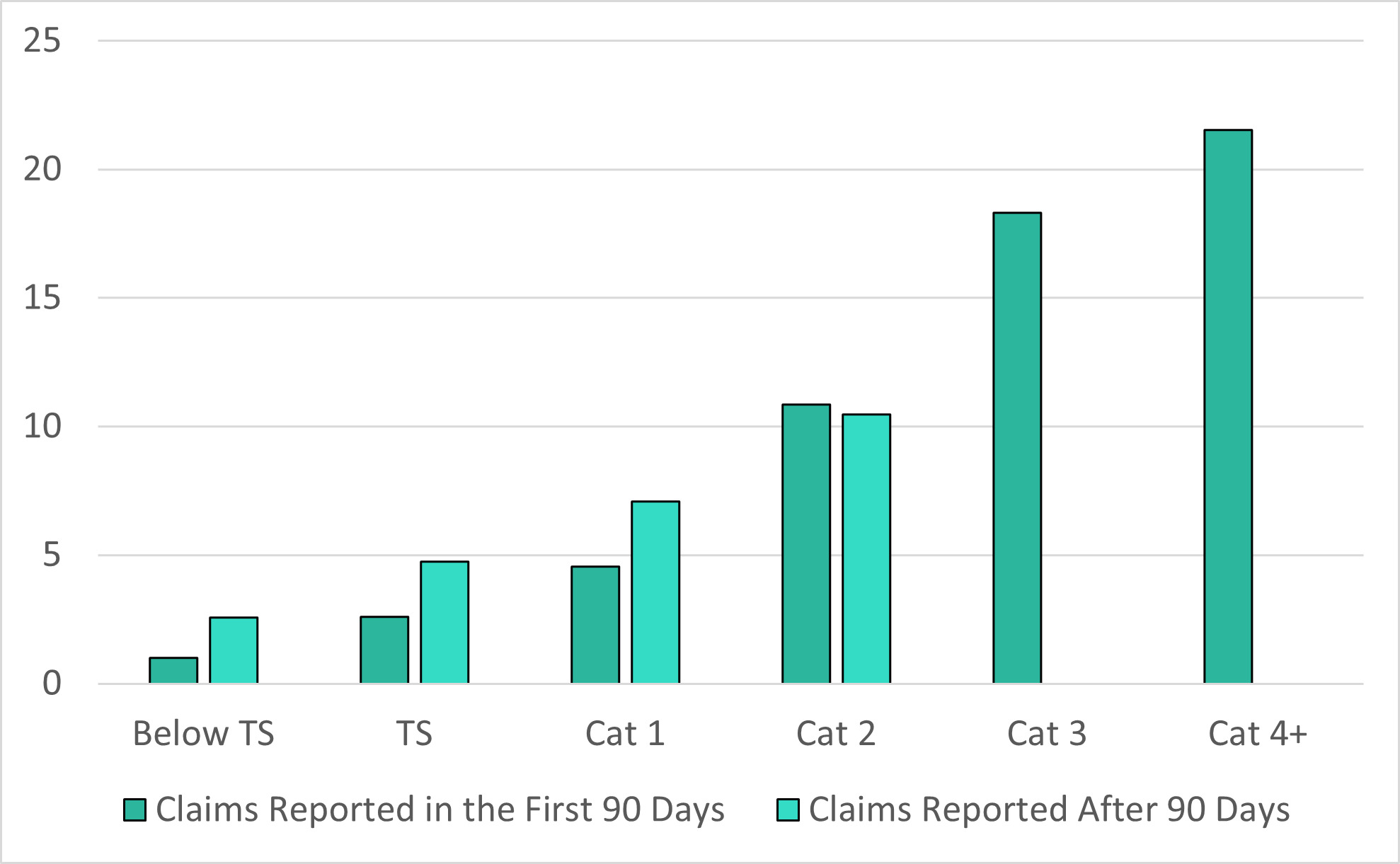

Systematic risk is a pivotal element in the determination of hurricane ultimate losses, accounting for over 90% of the total losses, as demonstrated in the Figure 3. Understanding and accurately estimating losses associated with systematic risk are essential for actuaries to effectively reduce the potential for adverse development. The Frequency-MDR methodology, outlined in this paper, emerges as a robust and precise tool tailored specifically for estimating systematic risk.

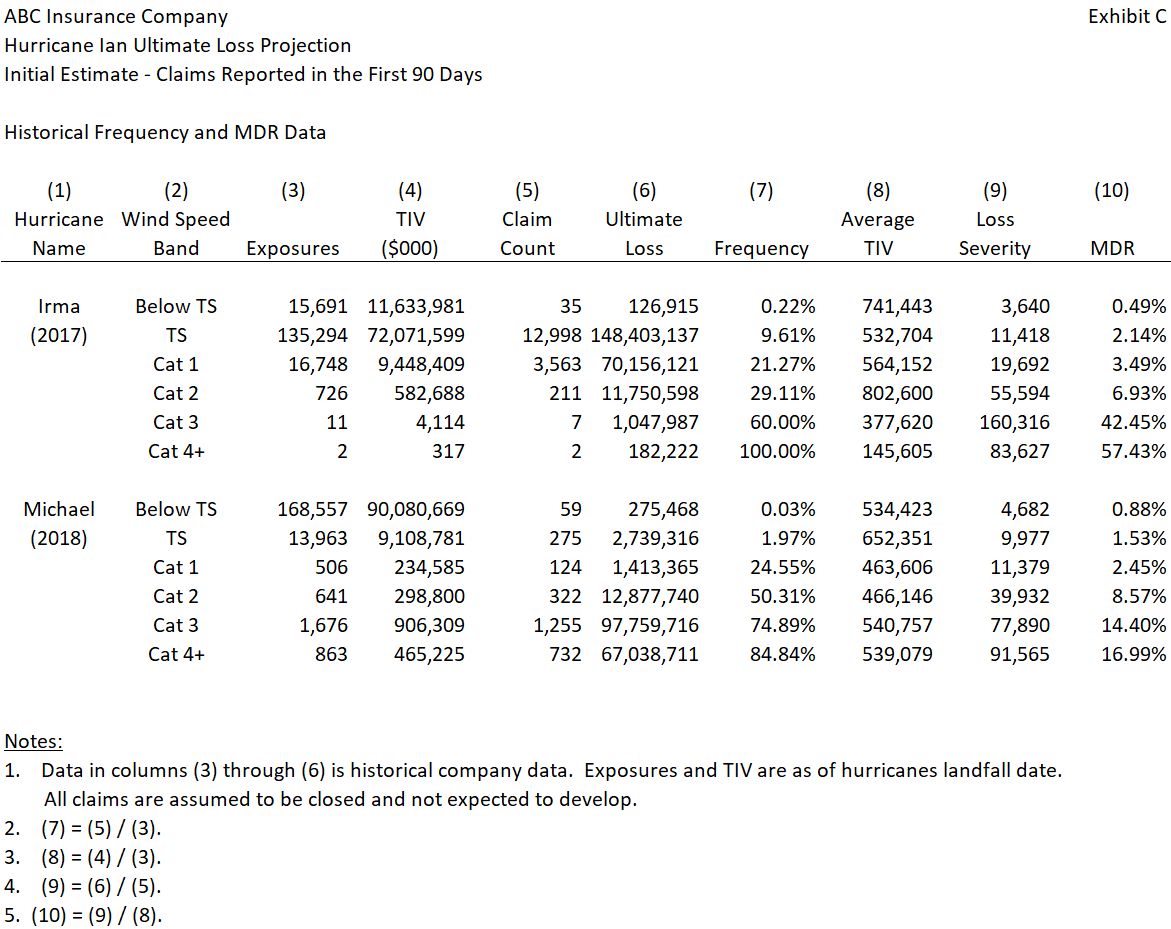

The Frequency-MDR methodology leverages both the advanced capabilities of catastrophic models and the reliance on insurance companies’ historical experience. The methodology is based on a frequency-severity method, where severity is estimated using a Mean Damage Ratio (MDR). In catastrophe models, MDR is defined as the expected ratio of repair cost of the asset to its replacement value. Replacement value usually refers to a building and to its contents. Given that hurricane claims also cover living expenses, this methodology defines MDR as the expected ratio of the claim cost to the Total Insured Value (TIV).

Recognizing the strong correlation between wind speed and both claim frequency and severity, the methodology employs a matrix-based approach for ultimate loss calculation. This framework stratifies losses by wind speed zones, enabling a more granular and accurate assessment of potential claims under differing wind intensity scenarios. Armed with accurate exposure and frequency-severity data, the methodology culminates in a straightforward formula for calculating ultimate losses.

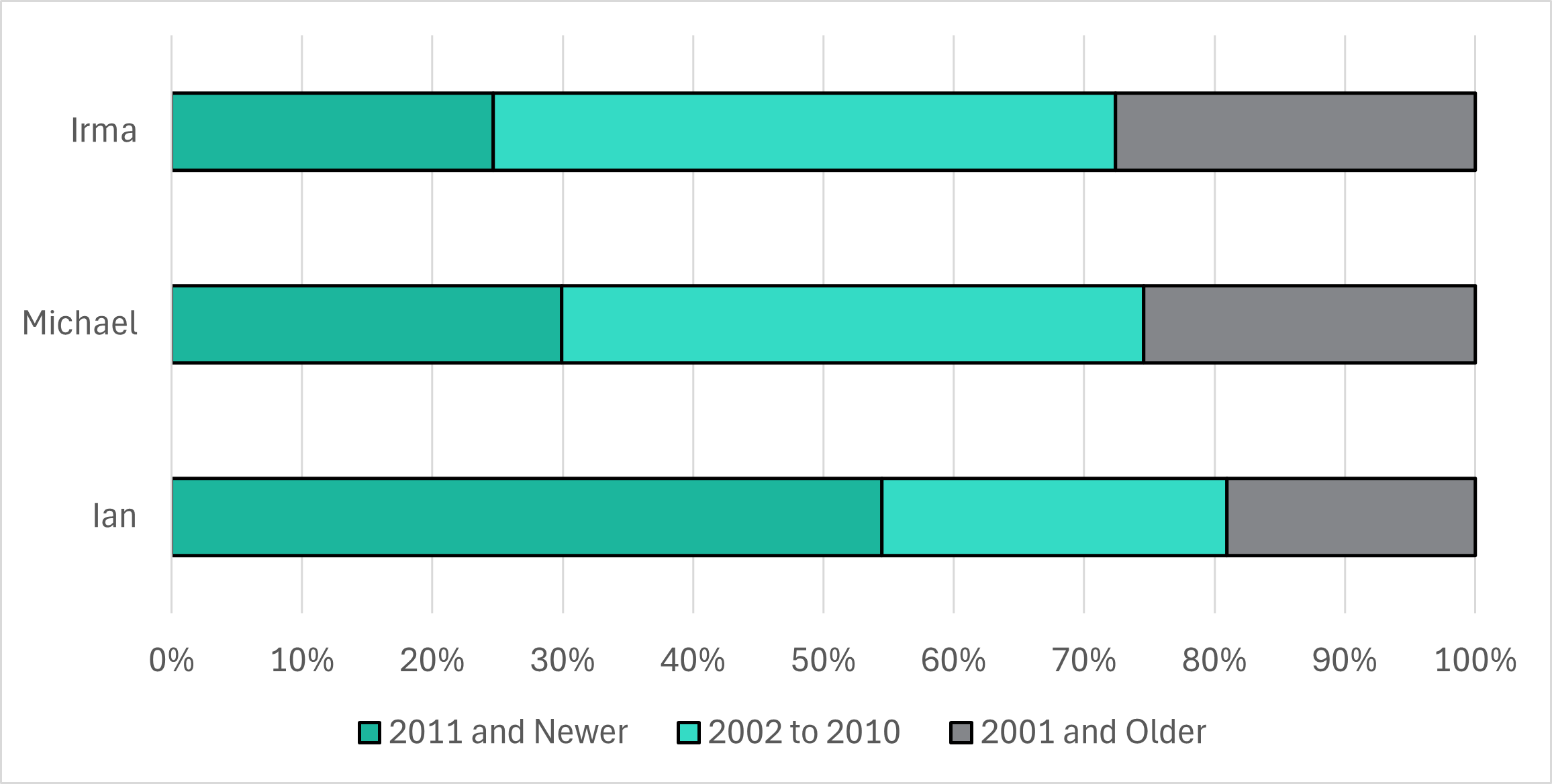

Frequency and MDR are estimated from historical events. Figure 5 shows frequency of Hurricanes Matthew, Irma and Michael claims. The frequency (axis Y) is calculated as number of claims reported in the first 90 days after landfall divided by number of exposures within each wind speed band (axis X).

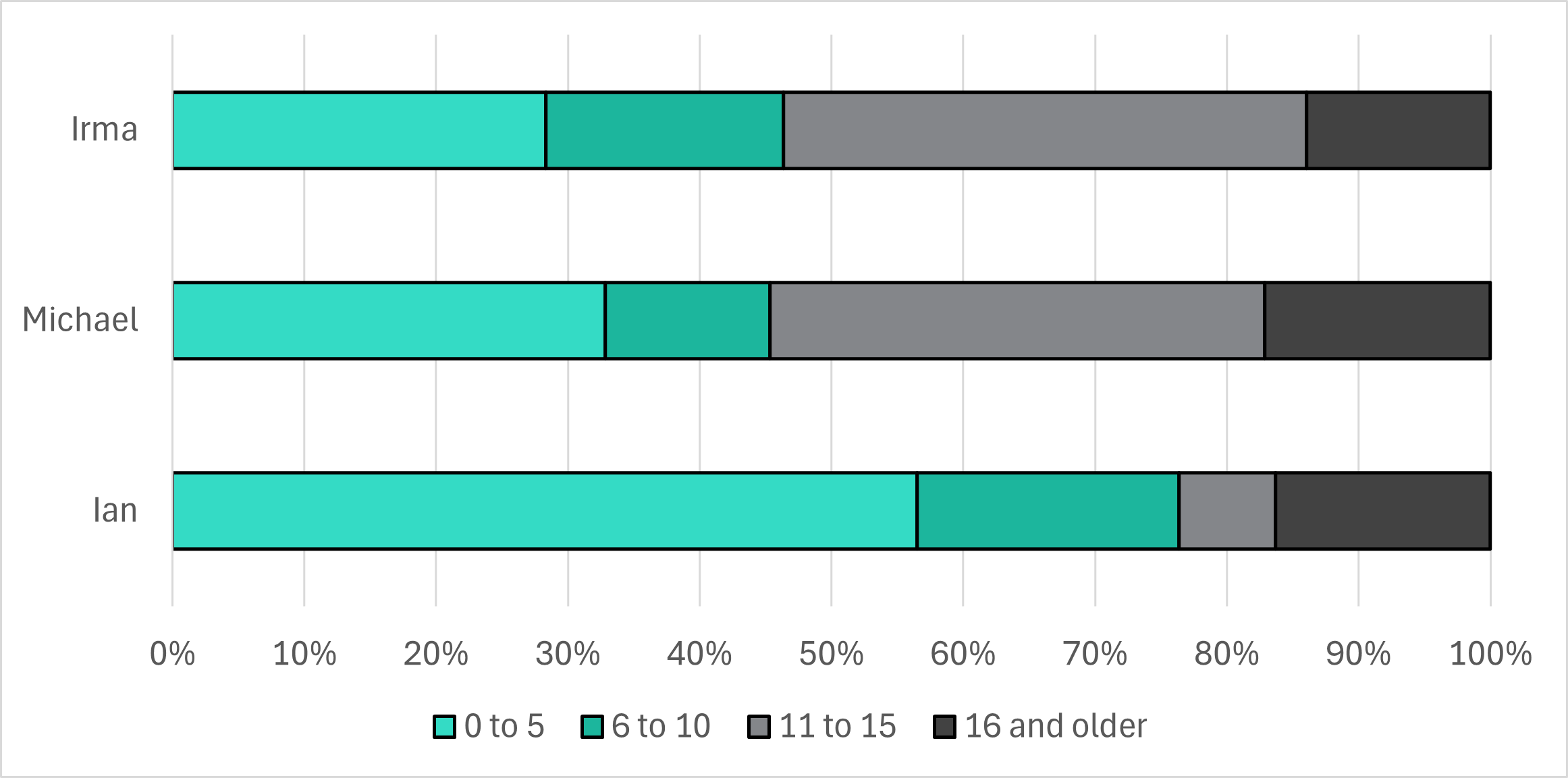

Figure 6 displays MDR (axis Y) derived from the same hurricanes data. MDR is calculated as loss severity for claims reported in the first 90 days after landfall divided by average TIV within each wind speed band (axis X).

A detailed example showing loss reserve estimate for claims reported in the first 90 days after landfall is shown in Appendix A.

Maintaining two datasets containing information on historical hurricanes is a good practice. The first dataset should include details on in-force policies at landfall for each hurricane, with wind speed or wind speed band assigned to each policy. The second dataset should store hurricane claims information at the most recent valuation. An outline of the suggested composition of these two datasets is provided in Appendix B.

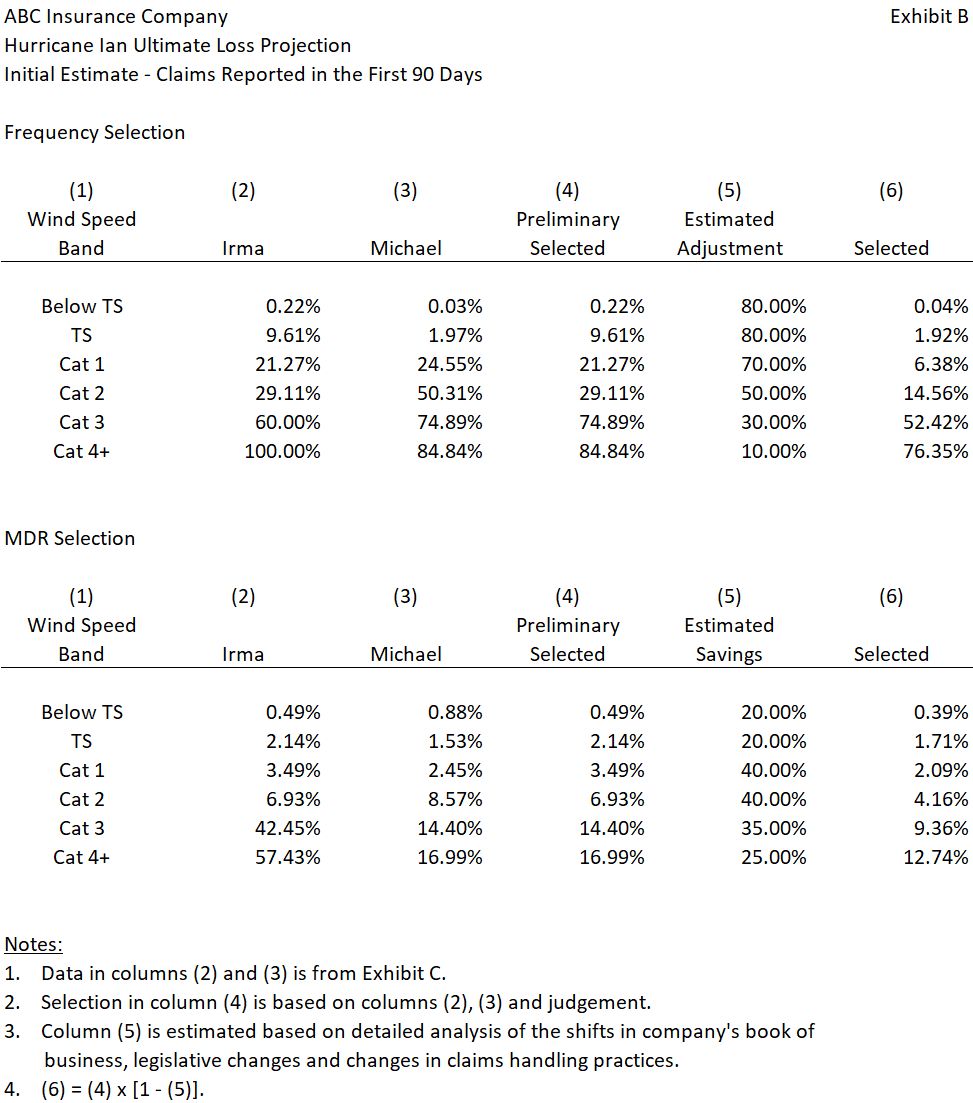

When selecting frequency and MDR, the actuary should decide what events to use as reference points. Historical hurricanes that made landfall in the same area are a logical choice. Another criterion for selection would be the presence of higher wind speed bands for stronger hurricanes. The actuary can select frequency and MDR ranges to establish a range of possible outcomes and then determine the actuarial central estimate (ACE) from within the range of outcomes.

If the dataset is sufficiently large to provide meaningful information, frequency and MDR can be selected by wind speed band and county/region as a proxy for building code and propensity to litigate, or by wind speed band and construction year as a proxy for building code. For low-speed bands, selection can be based on wind speed band and roof age/roof material. Other risk characteristics from the in-force policy dataset can also be used if they have predictive value. By using several sets of frequency and MDR, possible outcomes can be calculated, and the ACE, low and high estimates determined.

Estimating ultimate loss by wind speed band accounts for the intensity of a hurricane, while overlapping wind speed bands and company exposures accounts for the size of the wind field. However, the methodology does not directly consider forward speed. Nevertheless, the forward speed of a hurricane can significantly impact its destructive potential. For instance, slow-moving hurricanes like Dorian in 2019 tend to cause more extensive damage due to prolonged exposure to high winds, storm surges, and heavy rainfall. Conversely, fast-moving hurricanes such as Otis in 2023 pass through an area in a shorter time frame, resulting in less prolonged exposure to severe conditions. If a company has sufficient historical events, frequencies and MDRs of the events can be ranked based on the forward speed and judgmental adjustments to the selections could be made.

The number of years since the last hurricane in an area can be relevant when considering the impact of fallen trees during a hurricane. Over time, trees may grow larger and become more susceptible to uprooting or breakage during a storm. Therefore, areas that have not experienced a hurricane in a longer period may have more mature trees that pose a greater risk of causing damage to structures during a storm. By considering the time elapsed since the last hurricane, actuaries can better assess the potential for tree-related damage and adjust their frequency and MDR accordingly to reflect this risk factor.

For hurricanes that affect several states, estimating ultimate losses by state is recommended due to differences within the social, economic, and legislative environments as well as variations in building codes.

Reserving for Unsystematic Risk

The Frequency-MDR reserving methodology proves effective for addressing systematic risk. However, when it comes to unsystematic risk, several factors come into play, including the degree of social inflation within the state, the legislative landscape, and statutory hurricane claims reporting periods. The interplay of these factors increases the uncertainty surrounding actuarial estimates of unsystematic ultimate losses.

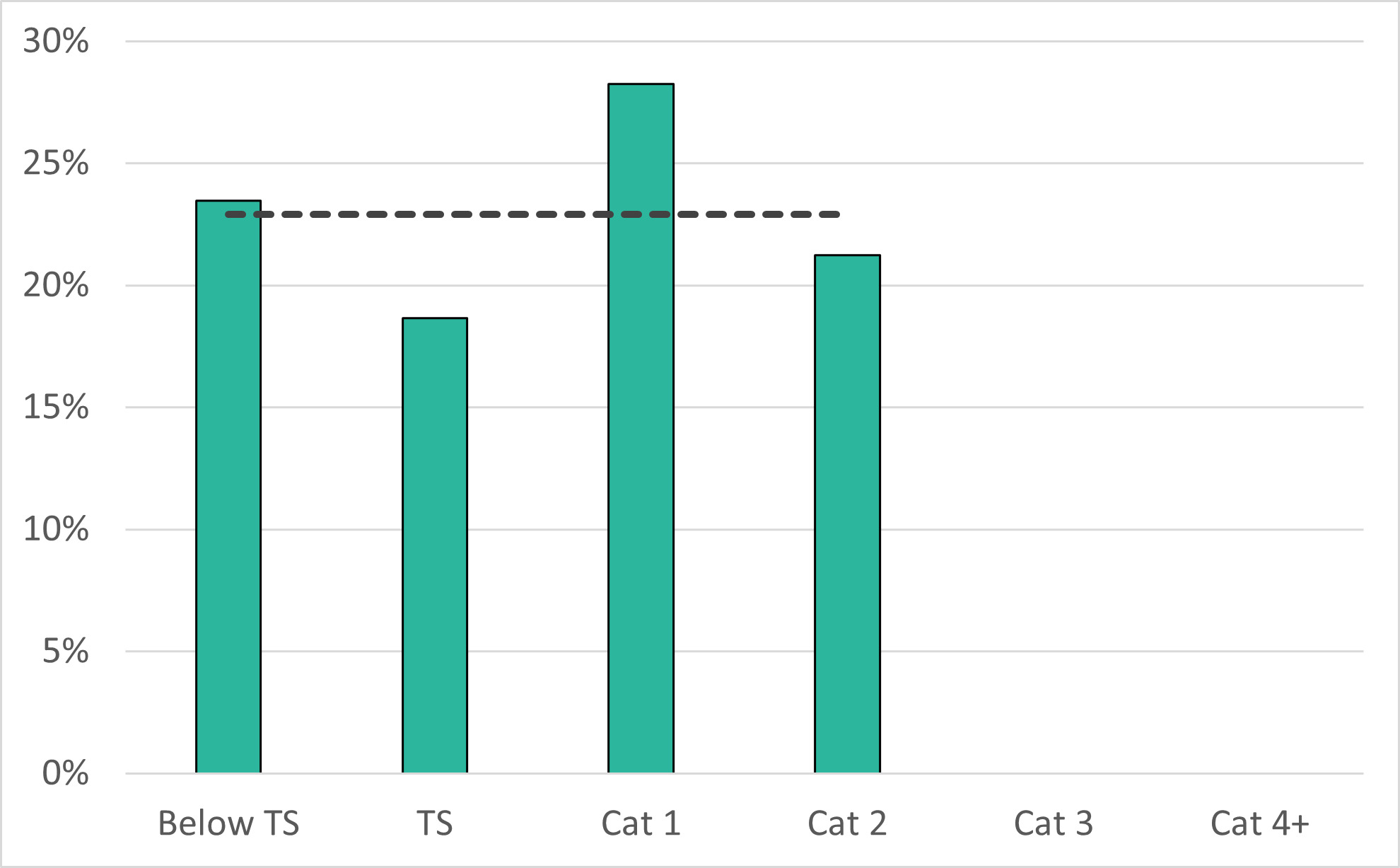

The straightforward approach to estimating losses on claims reported after 90 days would be to consider them as a percentage of systematic losses. However, as illustrated by Figure 3, this percentage can vary significantly from one hurricane to another, with Hurricane Irma standing out for its unusually large number of losses on claims reported after 90 days. If this approach is employed, understanding the underlying reasons for the variations is crucial for selecting the most appropriate unsystematic loss percentage. Let’s compare Hurricanes Irma and Michael for insight. Hurricane Irma made landfall in the Florida Keys as a Category 4 storm, then weakened to Category 3 status before hitting western Florida. It rapidly weakened over the mainland, resulting in widespread but relatively minor damage across the state. On the other hand, Hurricane Michael struck the Florida Panhandle as a Category 5 hurricane, then weakened to Category 3 intensity before exiting Florida. As we’ll explore further, late-reported claims are concentrated in areas affected by Category 2 and below winds justifying significant unsystematic risk component for Hurricane Irma. Another reason for the large amount of late-reported losses is that Hurricane Irma went through urban areas, which are known to have a higher degree of solicitation by contractors and lawyers compared to Hurricane Michael, which struck a rural area.

A more comprehensive approach involves analyzing unsystematic risk by wind speed band, mirroring the methodology applied to systematic risk. We’ll estimate the number of claims and severity separately. First, drawing from historical data, we’ll estimate the percentage of claims reported after 90 days compared to those reported within the first 90 days.

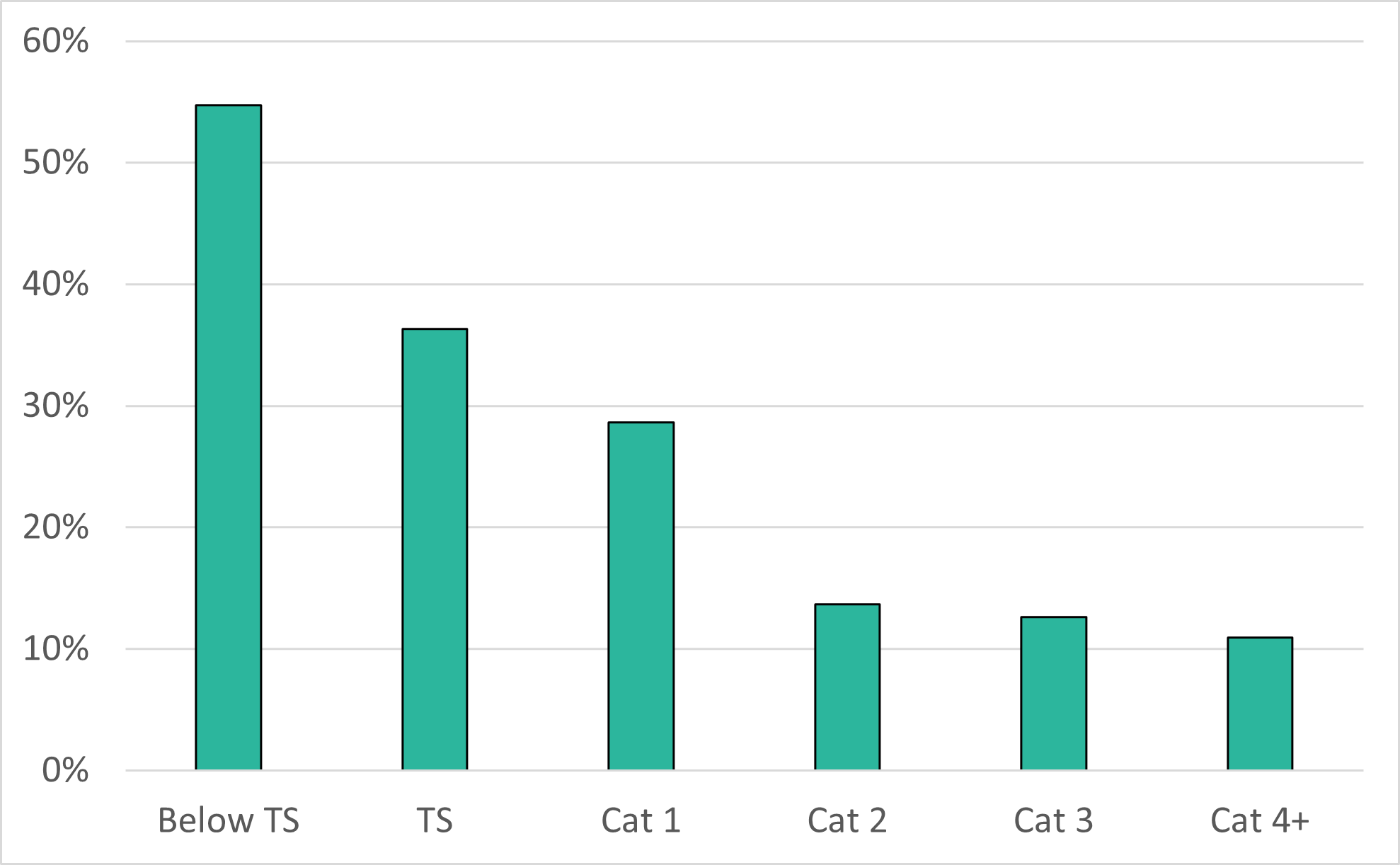

One notable observation is that properties which experienced Category 3 and higher wind speeds tend to file claims within the initial 90-day period. Secondly, unlike the pattern observed in Figure 5 for systematic risk frequency, the frequency of unsystematic risk appears to be independent of the wind speed band.

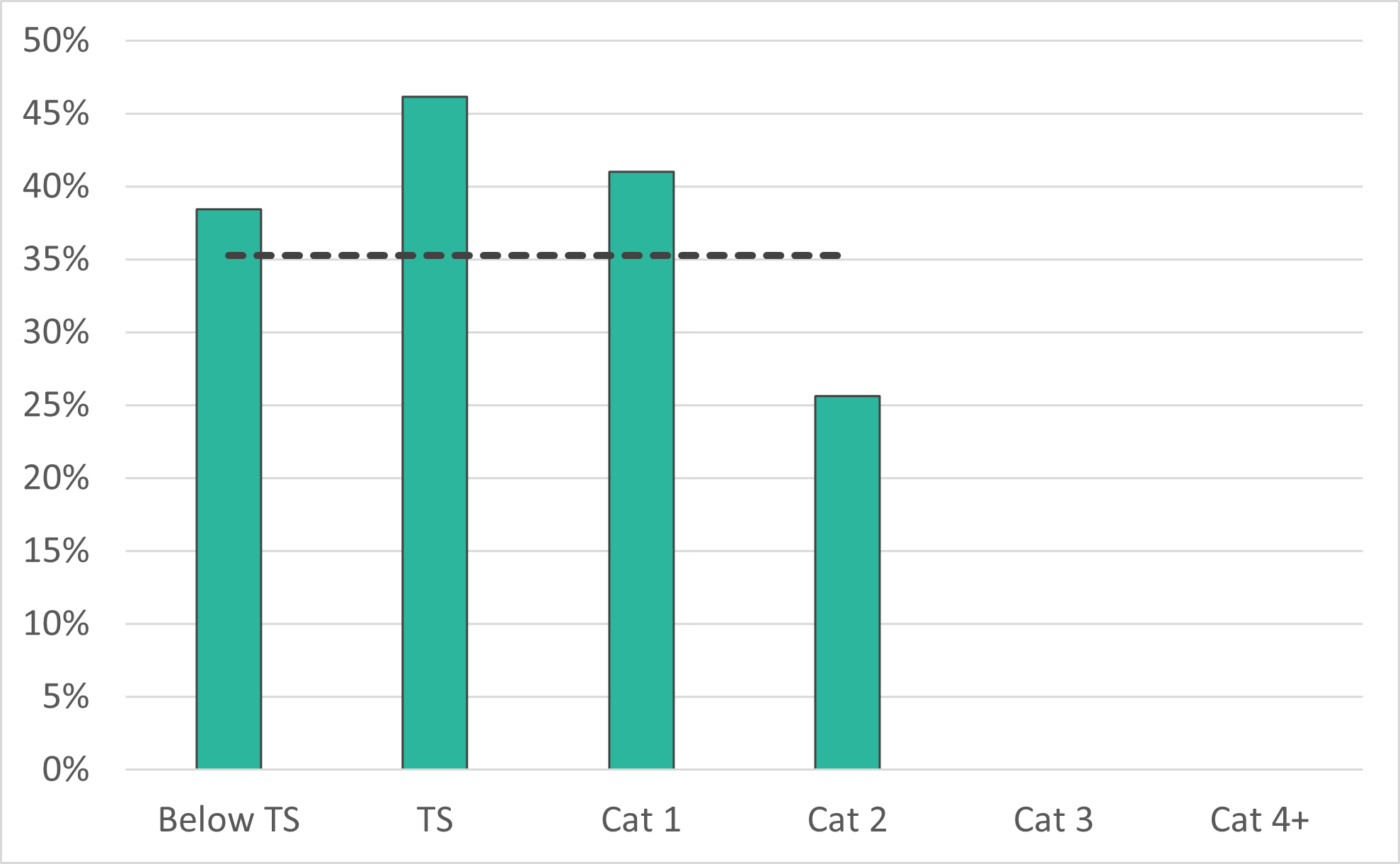

Let’s now compare historical severities for both systematic and unsystematic risk, broken down by wind speed band. Figure 8 provides a visual representation of these comparisons. The higher severity observed in late-reported claims compared to those reported within the first 90 days can be attributed to several factors. As time passes without addressing property damage, it tends to worsen, often leading to issues like mold development or structural decay, which require more extensive and costly repairs. Additionally, damages may be inflated by contractors seeking business through claim solicitation. These challenges underscore the operational risk posed by late-reported claims, which can be effectively addressed by insurance companies through the implementation of measures designed to mitigate potential increases in claims severities.

When selecting the number of claims and severity for unsystematic risk by wind speed band, similar considerations regarding historical hurricanes should be taken into account as those used in the simplified approach.

Loss Adjustment Expense (LAE) Evaluation

As claims become more complex and involve higher levels of damage, additional resources and expertise are needed to handle these claims. However, while the cost of the claims themselves may increase due to their complexity and the extent of the damages, the expenses associated with adjusting these claims typically do not rise at the same rate. Therefore, we will utilize historical LAE-to-Loss ratios by wind speed band to estimate ultimate LAE for systematic risk.

While this trend can be observed for systematic risk, unsystematic risk demonstrates a more uniform LAE-to-Loss ratio across all wind speed bands. Furthermore, the ratios for unsystematic risk are generally higher than for systematic risk. Let’s explore the causes of this phenomenon.

The data from Hurricanes Matthew, Irma and Michael claims, received on properties affected by wind speed Category 2 and below indicate that claims reported after 90 days are ten times more likely to result in litigation compared to claims reported in the first 90 days. Additionally, they are four times more likely to have benefits assigned and four times more likely to be represented by public adjusters. These representations not only escalate the cost of the claims themselves but also significantly increase the costs associated with adjusting and defending these claims.

Claims reported after 90 days are ten times more likely to result in litigation compared to claims reported in the first 90 days.

Estimate based on the analysis of Matthew (2016), Irma (2017) and Michael (2018) claims.

Implementation and Practical Applications

Estimating ultimate loss and LAE for hurricanes surpasses simple numerical calculations. It involves thorough groundwork, starting at the commencement of the hurricane season and extending through the anticipation phase before landfall. The estimation process progresses from the preliminary estimate pre-landfall to the immediate estimate post-landfall and continues to evolve as the event matures.

Benchmark Historical View

Benchmarking the historical hurricanes catalogue is foundational to the reserving process, often initiated at the onset of the hurricane season. During this stage, the loss dataset undergoes updating with the latest data, and any relevant information regarding prior year hurricanes is incorporated as appropriate. Additionally, the historical loss data is segmented into systematic and unsystematic components based on selected reporting lag. Frequency and MDR calculations by wind speed bands are performed for the data assigned to the systematic component. This calculation can encompass various exposure attributes, such as geography, year of construction, and roof age. Ratios of unsystematic to systematic losses and LAE ratios are also determined during this step.

Pre-Landfall Estimate

After the binding restrictions are imposed by an insurance company prior to hurricane landfall, wind speed band assignments for the approaching storm can be initiated. This task can be delegated to the company’s reinsurance broker. The broker overlays property locations from the in-force book with the hurricane shape file and assigns wind speeds and/or wind speed bands to each location. If the insurance company’s actuary has access to a hurricane shape file, this task can also be done internally using Geographic Information Systems (GIS) tools.

The National Hurricane Center (noaa.gov) updates the projected hurricane path and wind speed probabilities five days before expected landfall. For major hurricanes, updates are released every six hours. Modelers incorporate NHC projections into their models. The modeling software enables the overlapping of a company’s in-force risk location and projected wind speed bands, resulting in exposures and TIV by wind speed band.

It is important to note that different modelers can use various measures for wind speed, such as 1-minute sustained wind (Saffir-Simpson scale), 3-minute sustained wind, or others. Wind speed should be consistently defined for all historical events and the event being estimated.

During this step, an actuary also selects preliminary frequency and MDR values for each wind speed band as well as other benchmarking values to complete the calculation of ultimate loss and LAE for the event. These selections are informed by the catalogue prepared in the prior step.

The wind speed band assignments and preliminary benchmarking values selection process can be iterative as the storm approaches and new information about its strength and path becomes available. As the National Hurricane Center provides updated forecasts and projections, actuaries can reassess and adjust their estimations to reflect the dynamic nature of the approaching storm.

While this step may not seem necessary, it holds significant importance for insurance companies as they prepare for the upcoming storm. During this phase, insureds located within the cone of the storm can be promptly notified via text or e-mail, warning them about the approaching storm and providing guidance on how to safeguard themselves, their families, and their property. The content of these messages may vary depending on the assigned wind speed band, ensuring that recipients receive information relevant to their specific risk level. This proactive approach may aid in reducing potential claim sizes when policyholders take steps to prepare their properties for the approaching hurricane and mitigate damages afterward. Moreover, by fostering confidence in policyholders regarding the insurance company’s support, it may deter them from seeking assistance from soliciting contractors and assigning benefits to them. A company can also identify neighborhoods where the presence of insurance company representatives immediately after the landfall would be particularly valuable and helpful.

The second implication of this step involves aiding in decisions regarding the temporary staffing of claims departments and first notice of loss personnel based on the estimated number of claims expected in the first several weeks following the storm’s landfall. By proactively addressing these operational aspects, insurance companies can effectively manage the anticipated influx of claims and ensure a prompt and effective response to their policyholders’ needs in the aftermath of the storm.

With an estimated ultimate of 10,000 claims, as many as 1,400 claims could be reported on the first day alone. An additional 1,000 claims are expected to be reported on the second day.

Estimate based on the analysis of Irma (2017) and Michael (2018) reporting patterns.

Post-Landfall Estimate

Obtaining a reliable estimate of ultimate loss and LAE immediately after a hurricane occurs is essential for insurance companies, reinsurers, and investors. Ultimately, this will bolster investor confidence and expand coastal catastrophe reinsurance capacity.

If an actuary believes that replacing the in-force book of business after binding restrictions are imposed with the in-force book of business at the date of landfall will result in more accurate estimates, this adjustment can be considered. Final wind speed bands will be assigned based on the actual hurricane wind field and intensity. Benchmarking value selections will also be finalized, and the initial estimate of ultimate loss and LAE will be calculated. Utilizing this framework and extensive preparation activities, the initial estimate can be produced within several days after the hurricane’s passage.

Post-90-Day Reserving

Once 90 days since the landfall have elapsed, adjustments are made to the Frequency-MDR reserving methodology for systematic risk. At this stage, the frequency component is replaced with actual claim counts, eliminating uncertainty around this aspect of the estimate of systematic risk. Additionally, N-days from landfall-to-ultimate MDR development factors for historical hurricanes by wind speed bands can be calculated. These values are used to select the appropriate MDR development factor for systematic risk assessment, reflecting the progression of loss severity over time. Ratios for unsystematic risk can be calibrated based on the observed development and benchmarking against historical hurricanes, facilitating more accurate and reliable loss and LAE projections.

Strategies for New or Data-Scarce Insurance Companies

When an insurance company lacks historical data or the data available has limited credibility, several techniques can be employed to estimate ultimate losses:

-

Utilizing Modeled Losses: Despite the inherent limitations discussed earlier, relying on modeled losses might represent the most viable option for new insurance companies or those venturing into new states or lines of business to estimate ultimate losses immediately after landfall.

-

Leveraging MDR from Catastrophe Models: After 90 days from landfall, when the number of claims for systematic risk becomes known, the simplified Frequency-MDR methodology can be applied. In this scenario, MDR by wind speed band can be estimated from catastrophe models.

-

Relying on Industry Historical Data: State Departments of Insurance typically collect data from insurance companies on major hurricane events. For example, the Louisiana Department of Insurance (http://ldi.state.la.us/) publishes quarterly hurricane data calls online for the first four quarters after landfall. Similar information can be obtained from the Florida Department of Insurance (floir.com).

-

Utilizing the Company’s Non-Catastrophic Claims Loss Development: While loss development triangles may not be suitable as discussed above, N-days-to-ultimate loss development factors can be estimated from closed non-catastrophic claims grouped by loss size as a proxy for wind speed bands. Here, N represents the number of days from landfall to the hurricane evaluation date.

-

Fitting Payout Patterns: Curve fitting can be applied to loss payments grouped by calendar month. This method is particularly effective for more mature hurricanes as they provide more data points to fit the curve.

For LAE estimate, LAE-to-loss ratio from non-catastrophic claims grouped by loss size as a proxy for wind speed band can be utilized.

External and Internal Changes

Similar to various non-catastrophic claims reserving methods, actuaries should take into account shifts in the socio-economic environment, as well as regulatory and legislative changes, when relying on historical experience. Effective communication with underwriters and the claim department is key to understanding internal shifts within an insurance company, such as changes in the book of business or claims handling practices.

Economic Inflation

The Frequency-MDR methodology does not rely on dollar estimates of severity. Instead, severity is quantified as a percentage of TIV, known as the MDR. If an insurance company employs an inflation guard, no further adjustments are necessary. However, if an inflation guard is not in use, the MDR should be adjusted to accommodate trends in severity. Demand surge is inherently incorporated into the MDR as it is derived from historical experience.

Social Inflation

Social inflation refers to the impact of societal factors on an increase in the frequency and severity of insurance claims, escalating litigation costs and jury awards. This phenomenon is evident in historical data, particularly at low-speed bands, and pertains to unsystematic risk. When selecting benchmark values, it is crucial to account for changes in policyholders’ inclination to inflate claims due to evolving societal norms and attitudes. Recent legislative initiatives, such as lifting the matching principle or eliminating one-way attorney fees, aimed to reduce social inflation effect.

Legal Environment

Understanding the legal environment in a state is important for estimating hurricane losses due to its significant impact on insurance claims handling and settlement processes.

Statutory Hurricane Claims Reporting Periods

Statutory regulations governing time limits for filing insurance claims vary from state to state. For example, in Florida (2011 F.S. 627.70132), hurricane claims were required to be reported “within 3 years after the hurricane first made landfall or the windstorm that caused the covered damage”. Louisiana law (La R.S. 22:1264) stipulates that “[t]he time limit for the submission of proof of loss shall be not less than one hundred eighty days.” This difference in reporting requirement results in varying percentages of claims reported within 90 days from landfall, as demonstrated by comparison of data from Florida and Louisiana.

For Hurricane Irma (2017), only 79% of claims were reported within 90 days after landfall. The three-year reporting period prolonged an opportunity for roof replacement solicitation, exacerbated financial strains on insurance companies, leading to increased insolvencies.

To address this situation, effective July 1, 2021, Florida Senate Bill 76 amended the hurricane claim reporting deadline to two years. In Florida, claims for Hurricanes Ian (2022) and Nicole (2022) are required to be filed within two years from the landfall. Subsequently, Florida Senate Bill 2A, further reduced the reporting deadline to one year for new or reopened claims and to 18 months for a supplemental claim on policies effective on or after January 1, 2023.

Given the adjustments in reporting deadlines, selections based on Florida historical data should be appropriately modified to account for the differing statutory requirements for historical and future hurricanes.

Florida Senate Bill 76 (SB 76)

SB 76, which came into effect on July 1, 2021, not only amended the deadline for reporting hurricane claims but also revised the one-way attorney fee provision. Additionally, in response to the surge in roofing claims and associated litigation, the bill prohibited roofing contractors from soliciting claims. However, shortly after the bill was enacted, this provision was ruled unconstitutional.

Florida Senate Bill 2D (SB 2D)

On May 26, 2022, SB 2D and SB 4D were signed into law. SB 2D limited the attorney fees to “a reasonable hourly rate multiplied by a reasonable number of hours spent on a case”, eliminated collection of attorney fees from insurance companies by a third party under Assignment of Benefits (immediately challenged in a lawsuit), and prohibited contractors from roof claims solicitations.

Florida Senate Bill 4D (SB 4D)

Before May 26, 2022, if over 25% of a roof needed repair or replacement, the entire roof had to be replaced. SB 4D, effective May 26, 2022, abolished this rule, now requiring only the repaired or replaced portion of the roof to comply with the current Florida Building Code (FBC), as long as the rest of the roof meets requirements of 2007 or later FBC. However, the benefits of this change were not realized for 12-18 months.

Florida Senate Bill 2A (SB 2A)

In addition to lowering statutory hurricane claim reporting requirements, SB 2A, effective January 1, 2023, eliminated one-way attorney fees and prohibited assignment of benefits (AOB).

Shifts in the Book of Business

Each year insurance companies naturally gravitate towards insuring newer homes constructed under increasingly stringent building codes. These modern structures are better equipped to withstand the ravages of hurricanes compared to their older counterparts. For that reason, it is recommended to select frequency and MDR by wind speed band and construction year. It is logical to use effective years of revised building code as split points for the hurricane experience. Hurricane Andrew (1992) prompted a sweeping overhaul of building codes in Florida and the coastal U.S . The Florida Building Code (2001 FBC) was adopted effective March 1, 2002, making construction year 2002 a good bifurcation point for Florida hurricane experience. With the evolution of building standards over time, further segmentation of data is warranted. For example, the 7th Edition of FBC (2020), effective in January 2021, contains noticeable changes to roofing and wind load requirements, representing yet another logical cut off point for analysis.

Roof age represents another dimension to the shifting nature of books of business. In the aftermath of Hurricane Irma (2017), a significant number of roofs were replaced, spurred by solicitation efforts from roofing contractors, not only within Irma’s impact zone but across Florida as a whole. As a result, a disproportional number of roofs were 5 years old or newer by the time Hurricane Ian (2022) struck. Given this shift, it is advisable to make frequency and MDR selections based on roof age (roof age categories) within each wind speed band.

Similar considerations can be given to other rating attributes, like increased hurricane deductibles, that may be present in the in-force book of business dataset.

Changes in Claims Handling Practices

In response to social inflation, insurance companies have increasingly relied on preferred contractor networks and may opt for repair instead of cash settlements. These shifts in practice could potentially alter the rate of claim payments and ultimately reduce severity. Additionally, it’s crucial to assess how swiftly a company can secure temporary staffing to handle the surge in claims in the initial weeks, even days, following the landfall, and how this compares to historical benchmarks set by previous hurricanes.

Reserving for Catastrophes Other Than Hurricanes

While initially developed for hurricane event reserving, this methodology can be applied to well-modeled events where distinct frequency-MDR groups can be identified. Exploring its application to tornados, hailstorms, earthquakes, and floods represents an area for future research.

Conclusion

This paper introduces a Frequency-MDR reserving methodology tailored specifically for catastrophic events. It breaks down systematic and unsystematic risks and offers a structured approach to separate them, providing a clear and transparent framework for estimating loss and loss adjustment expenses (LAE). While the main focus of the methodology is on evaluating systematic risk, the paper also explores ideas for assessing unsystematic risks, giving a comprehensive overview of the reserving process.

The applicability of this methodology extends beyond post-event loss estimation. It demonstrates value in proactive measures like early policyholder notifications about impending storms, thereby fostering risk awareness and preparedness. Additionally, it assists the claims department by facilitating efficient workflows and ensuring readiness for the incoming surge of first notices of loss. Improved accuracy in catastrophe events reserving is also vital for boosting confidence among reinsurers, thereby strengthening partnerships with insurance companies.

One key takeaway from this paper is that estimating losses goes beyond just analyzing historical data and using actuarial techniques. Actuaries need to tap into insights from catastrophic models and understand their outputs, blending these findings with their expertise to improve the accuracy of loss projections. Additionally, they must possess comprehensive knowledge of historical catastrophic events, including their geography, intensity, and impact on insured properties. Plus, they need to have a deep understanding of the company’s book of business, along with knowledge of historical and current legislative environments and statutory requirements. Actuaries also should work closely with claims departments to spot any differences in claims handling between current and historical events.

And let’s not forget about innovation. Actuaries need to keep up with technological advancements and embrace new ideas. As new technologies emerge in catastrophe risk management and predictive analytics, there are opportunities to develop new reserving methodologies. By staying on top of these developments, actuaries can keep refining their approaches and adapt to changing risk landscapes.

_track_and_intensity__according_to_the_saffir--simpson.jpeg)

_track_and_intensity__according_to_the_saffir--simpso.jpeg)

_track_and_intensity__according_to_the_saffir--sim.jpeg)

__michael_(2018)_and_ian_(202.png)

_distribution_for_hurricanes_irma_(2017)__michael_(2018)_and_ian_(2.png)