Unexpectedly high increases in loss costs have occurred in recent years in some property and casualty coverages. Much of the unexpected increase has been attributed to “social inflation,” though many social and economic factors have contributed to rising claims costs as well. For instance, economic inflation also increased significantly in 2021 and 2022.

The recent focus on inflation in insurance can be considered part of managing the “New Normal,” which refers to the dramatic change in the economic and social environment since 2020. The results of a recently published survey, “The Risks of Change in the Insurance Industry: Adapting to The New Normal,” found that uncertainty about inflation ranked in the top five of risks that chief risk officers are concerned about. Social inflation was also a concern but did not rank in the top five. Some actuaries may consider social inflation to be a component of their concerns about unexpected changes in loss trend.

Defining Social Inflation

Further, the definition of “social inflation” could be considered ambiguous, but the more general definition of social inflation includes structural shifts in social and economic factors that drive insurance costs, i.e., “the New Normal.” This essay focuses on inflation in its totality, including both social inflation and unexpected economic inflation and examines some of structural shifts[1] causing unexpected increases in inflation.

Though the sudden rise in economic inflation is recent, the insurance industry has been concerned about inflation for several years. Around 2019, insurance companies were noticing unexpected increases in losses in the commercial auto line. Losses in general liability and professional liability are also experiencing unexpected increases. In 2021, the Insurance Information Institute (Triple-I) discussed social inflation as an emerging issue, and the Triple-I, the Casualty Actuarial Society and the Canadian Institute of Actuaries collaborated on a research paper on social inflation[2]. That paper discussed methods for assessing the impact of social inflation on ultimate loss estimates.

Social inflation is often defined as the excess of the rate of trend in an insurance coverage over economic inflation. Thus, claim cost increases in excess of economic inflation, typically as measured by the Consumer Price Index (CPI), are categorized as “social inflation” (See NAIC discussion of social inflation[3]). Triple-I defines social inflation as the impact of “rising litigation costs on insurance payouts.”[4] Actuarial Standard of Practice No. 13 (ASOP 13), “Trending Procedures in Property and Casualty Insurance,” states that actuaries should consider the impact of economic and social influences on trend. It defines economic and social influences as “The impact on insurance costs of societal changes such as changes in claim consciousness, court practices, and legal precedents, as well as in other noneconomic factors.” ASOP 13 therefore defines the social influences more broadly than does Triple-I, which focuses primarily on the legal and legislative drivers of claim cost trends (and thereby focuses on only one aspect of social inflation).

Loss Increases

However, defined, the insurance industry is focused on and concerned about the impact of recent increases in losses on insurance company profitability. As reported by AM Best, the U.S. property and casualty insurance industry experienced overall underwriting losses in 2022[5] after smaller underwriting losses in 2021, primarily driven by results in personal lines (auto and homeowners/farmowners) which experienced about $40 billion in losses. Eighty percent of the loss was attributable to personal auto insurance, which was affected by other factors including supply chain interruptions and lack of technology-skilled auto repair personnel.

This essay argues for a broader definition of social inflation that is similar to ASOP 13’s definition of social influences. It also argues that the CPI should not be used as an indicator of the impact of economic inflation in insurance[6], due to adjustments in how the CPI was calculated beginning in the 1980s. As a result of an adjustment known as the hedonic adjustment (to be described later in this essay), the actual out-of-pocket costs of most Americans rise at a higher rate than indicated by the CPI inflation rate.

This essay analyzes the drivers of insurance inflation using the recent cost increases in personal and commercial auto insurance. It also examines the impact of underlying societal changes and changes due to economic factors. Further, it will illustrate that some of the excess[7] inflation in insurance is a result of the hedonic adjustment to the main indicator of inflation, the U.S. Bureau of Labor Statistics’ CPI. The essay also discusses navigating the ambiguity of unknown and unknowable changes in insurance inflation that is being encountered by actuaries under the “New Normal.”

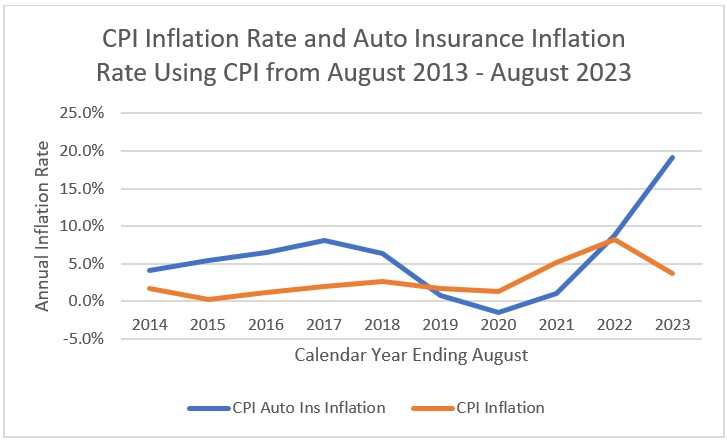

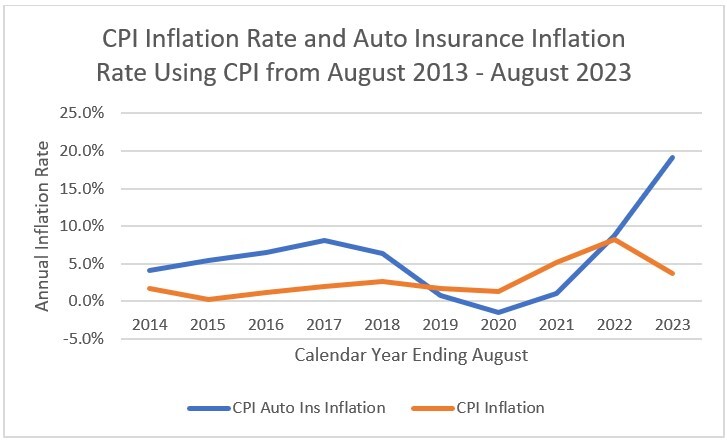

Figure 1 shows the year-over-year inflation rate, as of August 2023, in the Bureau of Labor Statistics Consumer Price Index (All Urban Consumers) and the Automobile Insurance Consumer Price Index (All Urban Consumers).[8] Figure 1 indicates that the automobile insurance inflation rate typically exceeds the inflation rate for all items in the overall CPI. The automobile insurance inflation rate declined in 2019 and 2020. A 2020 decline is to be expected, as the number of miles driven declined dramatically in 2020 due to COVID lockdowns. After 2020, the auto insurance rate increased dramatically and reached about 20% by August of 2023. It also rose dramatically above the CPI inflation rate, even though CPI inflation also increased.

Personal Auto

The personal auto trend has received a lot of attention in the business press due to the very large underwriting losses. Large auto insurers, such as Progressive[9] and Allstate,[10] have attributed their loss increases to rising automobile severity. Both companies mention property damage (PD) liability (third party) and physical damage (first party) inflation specifically as drivers of higher costs. In the past, bodily injury (BI) has frequently been an automobile insurance cost driver as BI severity is much higher than the severity of PD liability. Therefore, only small increases in BI frequency and/or severity can impact claims costs dramatically. Progressive[11] reported that its BI costs rose by 8% (still a relatively high increase but in line with CPI inflation during the period) but PD liability increased by 20% and physical damage by 16%. Progressive cited the higher costs of used vehicles and repairs and the cost of replacing totaled vehicles as contributors to the increases in personal auto insurance severity.

Increases in used car values were driven by supply chain disruptions, costs of labor and increased incorporation of high-cost, high-tech features. For instance, the consumer price index for used cars increased by about 10% in January of 2021 and by about 40%[12] in January 2022. The costs of many other components needed to repair cars also rose due to the increased use by consumers of cars with expensive high-tech components and supply chain disruptions in those components.

These observations suggest that the increase in personal auto insurance costs appear to be driven largely by social and economic factors specific to automobile replacement and repair cost and not by what has traditionally been considered social inflation factors, such as increased litigiousness.

Practices dubbed “sneakflation,”[13] “skimpflation” and “excuseflation”[14] are also affecting repair and replacement costs. “Sneakflation” refers to strategies that hide the actual price increases including:

-

Planning the obsolesce or the intentional manufacture of early failure into products, requiring sooner replacement

-

lowering the quality of the product while not lowering prices

-

keeping the high price of the product or service after commodity costs have declined, i.e., not lowering the price back to its original value before the commodity price increase occurred

-

charging a periodic service fee for access to products that the consumer previously bought and owned forever.

Dr. Pippa suggests the “sneaky” inflation increases are intentionally subtle and hard to detect but are becoming an important driver of inflation.

Commercial Auto

Triple-I highlights commercial auto as a coverage that has been significantly impacted by social inflation. The organization estimates the impact of inflation on commercial auto costs as approximately $4 billion in 2021.[15] Increased costs in commercial auto were noticed earlier than personal auto. For instance, for accident years 2018 and 2019, ultimate losses and loss adjustment expenses increased 15% and 11% respectively, based on Schedule P data as of 12/31/2022 published in the 2023 Best’s Aggregates and Averages.[16] In 2019, Liberty Mutual[17] pointed out that the industry had experienced its fourth consecutive year of loss increases. The Liberty Mutual Viewpoint article listed nine factors driving the commercial auto trends: distracted driving, impaired driving, aggressive driving, more vehicles on the road, new transportation modes (i.e., bicycles, pedestrians, motorcycles), driver inexperience (for commercial drivers), changes in litigation, rising vehicle repair costs and rising medical costs. Of these factors, only more vehicles on the road (since driver miles decreased in 2020 and are not yet at pre-COVID levels) would not hold today. Note that Best’s Aggregates and Averages data indicates commercial auto BI and PD liability claim volume dropped 15% in 2020, and though claim volume has increased since, it has not reached pre-COVID levels.

Many of the factors mentioned by the Liberty article, such as distracted driving and aggressive driving, could be viewed as “social influences” as defined by ASOP 13. Litigation is only one of the eight remaining factors (after removing more vehicles on the road, due to post-COVID effects), though it is often the focus of articles and papers on social inflation. However, another factor is the impact of how actuaries and insurance professionals measure and think about economic inflation. I will argue that some of the excess of the personal auto and commercial auto insurance trends over “economic inflation” as measured by the consumer price index are to be expected, due to the hedonic adjustment to prices used in computing the index.

Introduction to the Hedonic (Quality) Adjustment to the Consumer Price Index

The consumer price index (CPI) is a weighted measure of a market basket of goods and services where statistical sampling methods are used for selecting which items are included. However, the prices of the items sampled are often not measured at their retail quoted price. Instead, a quality adjustment, referred to as the hedonic adjustment, is applied to the price of the item in the sample. The Bureau of Labor Statistics (BLS) states:

"A fundamental problem for the goods and services in the CPI sample is that their characteristics, not just their prices, change over time as the retailers introduce new versions of items and discontinue the older versions. In many categories of items, this is the primary time when price change occurs. The new version of the item may provide additional benefits or, in some cases, reduced benefits. This change in benefit is quality change.

To measure price change accurately, the CPI must be able to distinguish the portion of price change due to this quality change."[18]

A result is that if a new car comes with new and “advanced” features, such as Advanced Driver Assistance Systems, the price used in the CPI measure is reduced for the quality improvement, as modeled by the BLS.

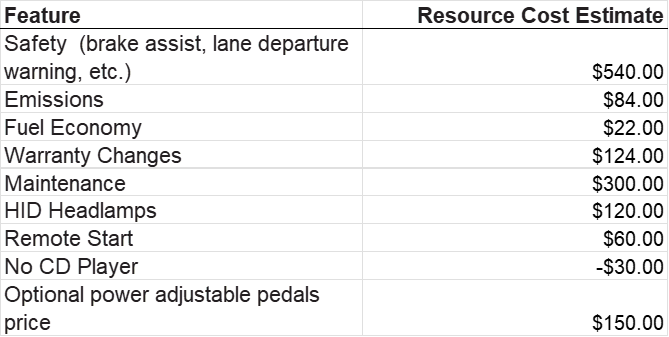

In its 2014 article on the quality adjustment to the CPI for new autos,[19] the CPI says it first makes resource cost estimates for each feature it adjusts for per Table 1.

A conversion is made to estimate the retail price from the resource cost estimates, so the final value of the quality adjustments is higher than those shown on the table. The final quality adjustment calculated from this process will be deducted from the retail cost of cars.

The new vehicle adjustment is an example of adjustments made to many of the items in the CPI. For instance, there is a hedonic adjustment for computers. Some items in the CPI are not hedonically adjusted, such as auto insurance. Over the past 11 years (2013 – 2023), the auto insurance CPI has been about 3 percentage points above the overall CPI. Because insurers cannot hedonically adjust their payments to claimants, it is reasonable to assume the insurers who must pay the actual current costs of the goods and services they indemnify will experience a higher inflation rate than inflation as measured by the CPI. Because of the hedonic adjustment, the CPI inflation rate is probably a poor benchmark for assessing the trend rates in insurance.

Alternate Inflation Index

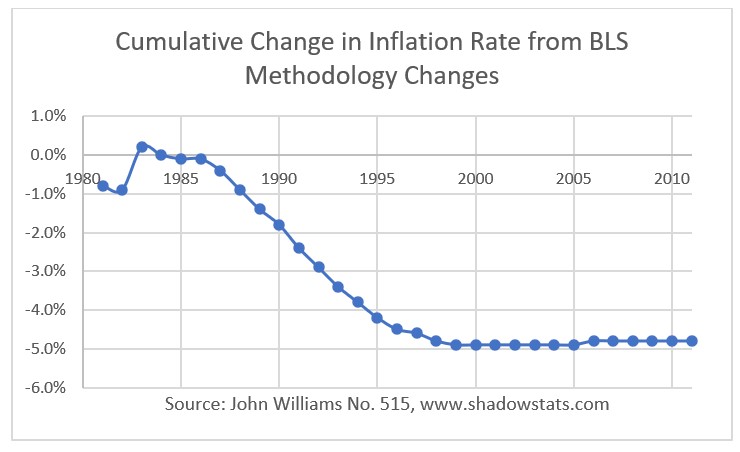

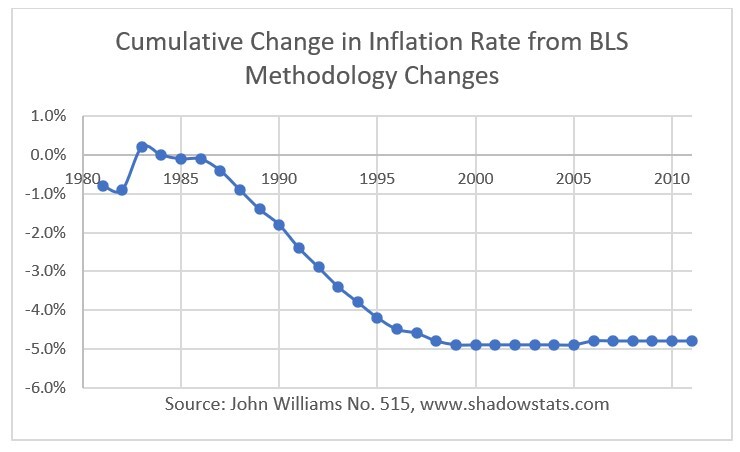

Economist Walter J. Williams publishes an alternate inflation index which removes the impact of methodological changes implemented by the Bureau of Labor Statistics (BLS). Information about the index can be found at the web site www.shadowstats.com. The index relies heavily on data in the BLS CPI-U-RS, a research index that restates the past consumer price indices to reflect all the methodological changes incorporated as of the most current consumer price index. Williams’ “Public Comment on Inflation Measurement and the Chained CPI (C-CPI)”[20] displays a table showing the research-consumer price index (CPI-U-RS) and the originally published consumer price index. These two series were used to compute two inflation rates from the two indices, along with the overall effect each year on the CPI-U measured inflation rate resulting from the methodology changes. Changes in addition to the hedonic adjustment are incorporated into the comparison. A discussion of these changes is beyond the scope of this essay, but a discussion of some of the other changes can be found in the documents on Williams’ website, as well as the Bureau of Labor Statistics web site[21]. Figure 2 displays the cumulative effect of all methodology changes as of 2011.[22] As of 2011, the cumulative effect was to lower the inflation rate by about 5%. Additional data for inflation beyond 2011 is available from Williams.[23] Williams alternate inflation index, currently available to subscribers, shows about an 8% difference between CPI inflation and his alternate inflation index.

Due to hedonic and other adjustments, there is a high probability that trend in many lines of business will exceed the CPI inflation rate. Alternative inflation indices such as William’s index can help actuaries understand what is happening to actual out-of-pocket costs for consumer products in the US economy.

Inflation in insurance loss costs is due to societal trends that have specific effects on insurance costs. This means that insurance companies need strategies specific to insurance to measure insurance trends and manage their business. Some companies compute their own “industry” insurance trends using published industry statistics, such as statistics from AM Best[24] or SNL[25], and/or from their own internal data.[26] Companies that provide reporting and statistical services to the insurance industry, such as the Insurance Services Office and the National Council on Compensation Insurance, are also sources of industry trend information. These are sources of industry specific inflation estimates that are independent of CPI measures.

The next section discusses practical approaches that have been used to deal with insurance trend in highly uncertain times.

Strategies for Assessing and Managing Trend

When socially influenced inflation is viewed more broadly as the composite of all economic and social influences that affect the cost of insurance, the increase in recent years in insurance costs is driven by much more than increased litigiousness and new ways of financing plaintiffs’ lawsuits. In both personal and commercial auto insurance, litigation issues may be one component driving Bodily Injury costs up, but there are many other factors. Property Damage liability and physical damage costs have been the big drivers of the increases in severity that drove the increase in automobile insurance costs in the past few years. These increases, though they had been developing over time, were exacerbated by effects from COVID lockdowns, as claim severity erupted in 2021 and continued upward in 2022 and 2023.

Companies familiar with the details of what was happening with their claims’ settlements and with the factors driving their loss experience, could react early to the changes. For instance, Progressive began implementing rate increases in 2021, before most insurers, and had better underwriting experience than many of its competitors.

Progressive management devoted much of the content of its 2023 annual report[27] to describing its response to recent trends, especially those in its automobile insurance coverages.

Progressive has a company-wide goal of a 4% underwriting profit. All parts of the company participate in meeting the goal. Company management reviews its progress towards its goal monthly. Early in 2023, Progressive management detected continuing increases in claims severity that were not part of their original plan for the year. While Progressive did not disclose their methods of assessing trend, they are known as early adopters of artificial intelligence and other modern technologies, so likely data analytics played a role. Their annual statement, which emphasizes the active collaboration of all parts of Progressive, would imply that the subject matter expertise of claims adjusters and the claims department management was critical.

After detecting the severity increase, Progressive made significant changes to their strategy for the 2023 year including:

-

Significant price increases, on top of increases in 2021 and 2022.

-

Underwriting actions, including strict underwriting discipline when loss ratios are increasing. The original plan had ambitious growth goals, which were reduced, with a focus on underwriting profitable policies.

-

Market segmentation — A a key part of Progressive’s strategy, technology, including telematics are tools used in segmentation.

-

Marketing changes – Progressive reduced overhead, including significantly reducing its marketing budget, including advertisement and other areas.

-

Claims response – Claims handling involved a quick response, and technology for evaluating and paying claims.

-

Company education – Progressive provides a data analysts boot camp for its employees who want to become data analysts. Data analytics is a key to meeting company profitability goals.

-

External environment monitoring – Progressive monitors external trends in order to respond quickly to what is changing in economy and society.

Based on the insights provided by the Progressive 2023 Annual Report, it’s clear that a comprehensive strategy involving early detection of unexpected changes in trend and rapid implementation of revised underwriting, marketing, claims and other strategies, including employee education, can successfully help insurance companies meet the challenge of the “New Normal.” In a “New Normal” world, actuaries need to navigate ambiguity. [28]The book Navigating Ambiguity states that ambiguity overlaps with but is not the same as uncertainty. It is “holding multiple ideas or possibilities” and “not knowing, the unknown, the grey area.”[29] Actuaries and insurance company managements may need to embrace ambiguity, not just endure it,[30] to successfully navigate ambiguity. The multi-functional, corporatewide response by Progressive to severity increases indicates that management planned for ambiguity and change and had strategies in place for successfully navigating ambiguity. Implementing the strategies resulted in a year 2023 that was more profitable than originally planned.

Recommendations for Further Research

Neils Bohr is credited with these words of wisdom about forecasting: “Prediction is very difficult. Especially if it is about the future.”[31] Predicting future insurance loss cost trends is a core actuarial function, yet it is one fraught with challenges and uncertainty. That’s why the CAS supports research on critical actuarial tasks, such as ratemaking and reserving.[32]

Given the daunting challenges actuaries face when predicting insurance cost trends, the CAS could sponsor research on Trend Forecasting. Perhaps a CAS Trend Working Party could take on the challenge and consider research on such topics as:

-

Conduct research to evaluate new methodologies for estimating trends. The research should use open-source data when possible. Perhaps the CAS subscription to S&P Global Capital IQ Pro could be used.

-

Perform research to identify data for assessing insurance trends.

-

Survey members on trend methodologies and their trend forecasts for emerging trends in insurance inflation.

-

Focus the research on specific lines of business.

- Professional liability trends have been very different from automobile insurance trends.

Conclusion

Actuaries routinely select trends to apply to their reserving and ratemaking analyses. Under the “New Normal,” this task has become more challenging, as most actuarial methods assume a stable environment. Some conclusions for actuaries from the information presented in this essay are:

-

Real changes in attitudes towards litigation and in how law firms finance the cost of filing insurance claims have occurred and have affected insurance costs particularly in some liability coverages. This essay has not focused on litigation driven social inflation, but instead has focused on unexpected inflation in (primarily) property coverages. However other authors, including some cited in this essay, have provided information on the impact of litigation trends on insurance costs.

-

Insurance trends in excess of the CPI inflation rate are driven by many factors unrelated to social inflation as traditionally defined, including methodologies used to compute the CPI which reduce the rate below out-of-pocket actual costs for consumers and insurers. As a mental model or benchmark index for the economic factors driving insurance losses, the CPI inflation rate has limited application. Actuaries may want to consult an alternative measure of economic inflation.

-

Recent structural social and economic changes, often referred to as the “New Normal,” have dramatically altered cost trends in some P&C insurance lines. A precise distinction between structural social changes and social inflation, under the more general definition of social inflation, may not be clear. The “New Normal” is a new challenge for insurers and is a frequent subject of current research and discussion in the insurance industry.

-

Actuaries should consult their own internal data and industry statistics when evaluating insurance-specific inflation rates.

-

Practical strategies exist to detect and manage the “New Normal” in insurance inflation. An example, featuring the response of Progressive to unexpected changes in severity trend in 2023, has been provided in this essay. The Progressive response was multi-faceted and companywide, involving a process that was in place before the unexpected trends occurred.

-

The quantification of insurance inflation is a core actuarial responsibility. Further research supported by the CAS could advance the profession’s ability to respond to unexpected changes in trend.

The essay is focusing primarily on non-litigation related factors

“Social Inflation and Loss Development,” Jim Lynch and David Moore, CAS Research Paper 2022 https://www.soa.org/research/topics/risk-mgmt-res-report-list/,

“Social Inflation: What it is and why it matters,” Trends and Insights, 2022, triple-i_state_of_the_risk_social_inflation_02082022.pdf (iii.org)

https://news.ambest.com/newscontent.aspx?refnum=251188&altsrc=174

Though its use for other applications is not being discussed here

That is, the excess of insurance inflation over economic inflation as measured by changes in the CPI.

Both series were downloaded from the St. Louis Fed web site in early 2024.

The 2022 Progressive Corporation Annual Report to Shareholders.

2022 Annual Report, p. 150.

Ibid, p. 64.

Consumer Price Index for All Urban Consumers: Used Cars and Trucks in U.S. City Average, Index 1982-1984=100, Monthly, Seasonally Adjusted.

Introduced by Dr. Pippa, https://drpippa.substack.com/p/sneakflation.

https://www.freedoniagroup.com/blog/inflation,-shrinkflation,-skimpflation,-and-excuseflation-what-you-need-to-know. This site discusses “skimpflation” and "excuseflation.

https://www.iii.org/article/social-inflation-hard-to-measure-important-to-understand

Based on the Net Total Losses and Expenses Incurred, Schedule P, Part 1C, Annual Statement Total US PC Industry, Col 28.

“Commercial Auto Insurance Trends in 2019,” Liberty Mutual Viewpoint.

“Frequently Asked Questions About Hedonic Adjustments to the CPI,” https://www.bls.gov/cpi/quality-adjustment/questions-and-answers.htm.

Guidelines for Quality Adjustment of New Vehicle Prices, https://www.bls.gov/cpi/quality-adjustment/new-vehicles.pdf.

The report can be requested from www.shadowstats.com.

Two of the most commonly cited of these other changes are the substitution of rental equivalent cost for homeowners cost and the use of a chained CPI (essentially a geometric average).

The graph is based on the Table in the Public Comment on Inflation Measurement. The data is used with permission of Walter J. Williams.

Contact information can be found at www.shadowstats.com.

AM Best, https://web.ambest.com/home.

S&P Global Market Insurance: SNL Insurance, https://app.snowflake.com/marketplace/listing/GZT0Z8P3D5A/s-p-global-market-intelligence-snl-insurance.

For instance, from combining the experience of numerous insurance industry customers.

The Progressive Corporation 2023 Annual Report, https://investors.progressive.com/files/doc_financials/2023/q4/interactive/static/media/Progressive-2023-AR.f93a3e76939b58794122.pdf.

At the October2023 CAS Leadership Summit, CAS volunteer leaders were educated on navigating ambiguity.

Page 21 in Navigating Ambiguity: Creating Opportunities in a World of Unknowns, Andrea Small & Kelly Schmutte, 2022, Ten Speed Press.

This is what is advocated in Navigating Ambiguity.

Quote taken from https://blogs.cranfield.ac.uk/cbp/forecasting-prediction-is-very-difficult-especially-if-its-about-the-future/.

For instance, the Bornhuetter-Ferguson method is a commonly used actuarial method for estimating ultimate losses, as is loss development. Two CAS Research Working Parties, the Bornhuetter-Fergueson Loss Ratio Prior Working Party and the Tail Factor Working Party, are examples of CAS-sponsored research in these areas.