Introduction

A widespread proliferation of Artificial Intelligence (AI) tools is currently underway, with the almost weekly release of new systems able to generate realistic images and videos, or create sensible text-based dialogues about wide-ranging topics. Powering the rise of these AI-based tools is deep learning, which is the modern approach to designing and fitting neural networks, a well-known machine learning (ML) technique. AI, as most of us experience it, is today synonymous with systems built with these deep learning tools. The deep learning revolution is now about 12 years old, if we take the starting date as the publication of the AlexNet paper (Krizhevsky, Sutskever, and Hinton 2012), which showed that stacking together layers of neural networks produced models capable of groundbreaking improvements in computer vision tasks. Since then, remarkable advances in AI have occurred in terms of natural language processing, computer vision, image generation and tabular data modelling. At the time of writing this essay, some AI-driven services such as advanced Large Language Models (LLMs) have already become commoditized, with multiple services available for public use at low cost.

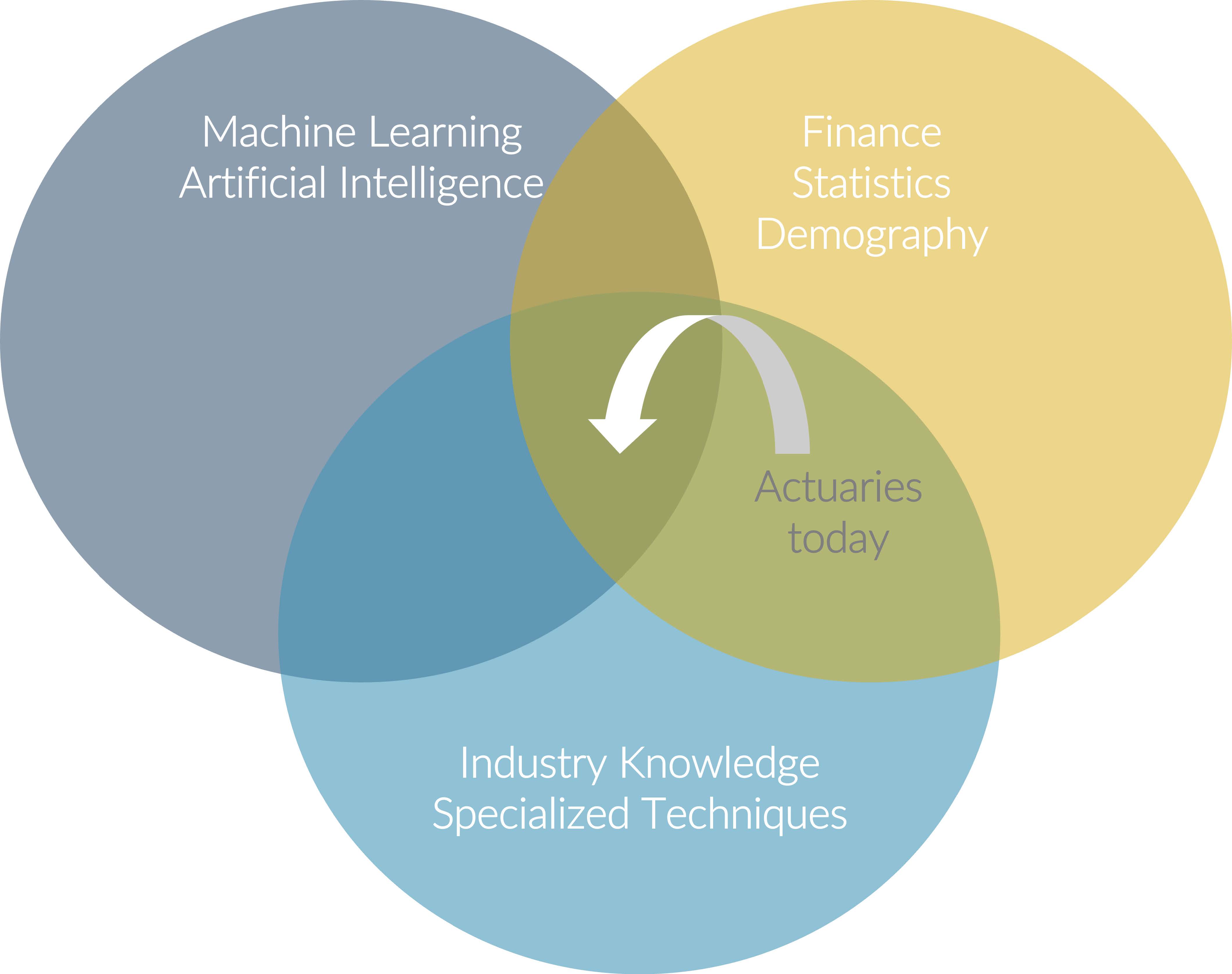

How should the actuarial profession react to these groundbreaking advances in AI, both within the methodology of actuarial science (as we shortly describe), and in wider fields? Actuaries — equipped with deep statistical and finance knowledge and professional expertise — play a key role in the management of financial services institutions in general, and of insurers in particular. From an academic point of view, a revolution is underway in the methodology of actuarial science, which has embraced the adoption of new AI and ML tools and techniques for traditional actuarial tasks (Richman 2021a). Within P&C insurance, these tasks include pricing and reserving, and, in other areas of actuarial work, these tasks cover experience analysis, mortality forecasting, capital modelling and more. However, this rapidly expanding body of research has not yet translated into widespread changes in actuarial practice, with many tools and techniques currently being used, remaining more or less unchanged for decades. For example, many reserving analyses are still performed using the chain-ladder or Bornhuetter-Ferguson (BF) techniques, and pricing models are often built using Generalized Linear Models (GLMs). The vision that we will discuss in this essay is summarized in Figure 1, which shows the current state of actuarial knowledge, and how this could evolve in coming years to include AI and ML as a core part of what actuaries do.

While LLM-based applications such as GPT-4 (from OpenAI) and Claude 3 (from Anthropic) are perhaps the AI tools that first come to mind when thinking about these areas, I think that the new tools and techniques being developed in the actuarial literature potentially hold equal or more promise for the actuarial profession. The former tools are examples of systems that may, debatably, be starting to approach a general form of AI (Bubeck et al. 2023) that can perform as well as, or better than, humans on a wide array of tasks (Anthropic 2024). On the other hand, the latter specific AI tools are designed to perform narrow tasks such as pricing or reserving, which are at the core of the technical tasks that actuaries perform in their roles. By utilizing these tools for applying AI within actuarial science, actuaries can build models more quickly and attain greater accuracy than using traditional methodologies (Richman 2021b), incorporate new data sources directly into their models (Gao, Meng, and Wüthrich 2019) and utilize new classes of inherently explainable models within their work (Richman and Wüthrich 2023a). In this vision of a potential future where actuaries adopt AI-based tools for actuarial tasks, actuaries will upgrade their tools, while remaining firmly committed both to the professional and ethical underpinnings of the actuarial profession (Harris, Richman, and Wuthrich 2024) and to long-standing principles underpinning P&C actuarial work, such as credibility and applying actuarial expert judgement.

Since ML and AI approaches excel at pattern recognition, complex data analysis, and predictive modeling, tools built with these methodologies are well-suited to tackle the challenges faced by actuaries in practice. By leveraging the power of AI, actuaries can develop more accurate and sophisticated models that incorporate a wider range of data sources, leading to better risk assessments and more precise pricing, than is currently the case today. Moreover, AI techniques like deep learning enable actuaries to uncover complex, non-linear relationships in data that may be difficult to capture with traditional statistical models. This enhanced predictive power can lead to more granular risk segmentation, personalized pricing, and the development of innovative insurance products tailored to individual customer needs through the use of emerging data sources such as telematics. The evolution of actuarial practice through AI is not just about building better models; it also presents opportunities to streamline and automate various aspects of actuarial work. From data pre-processing and feature engineering to model selection and updating, AI can help actuaries work more efficiently and focus on higher-level strategic tasks that require human judgment and domain expertise, as well as the ability to communicate the conclusions and implications of complex technical work to wider audiences.

A vision of the future

Let’s explore what core actuarial tasks could look like in a few years’ time if the profession chooses to embrace this path and enhance our tools and techniques using both specific and general AI applications. Today, when performing a reserving exercise, and after extracting updated data and performing reconciliations, a first step is often to compare actual reserve development to expected (AvE) to gain an idea of how accurate — or sufficient — the previously selected reserves were. Those lines of business where reserves were insufficient are often given more priority in the subsequent step, which is to select new loss development factors and assumptions, such as loss ratios for the BF method. Then, a final set of selected reserves will be produced and peer-reviewed, before wider communication of these outcomes to the business and senior management; as a result of discussion, the reserves may be modified before final numbers are booked into accounts and regulatory templates. Importantly, most of the analysis will be performed for each line of business in isolation, and new and emerging common trends across lines, for example, a change in inflation impacting motor lines, will usually only be discovered towards the end of the process.

How could the reserving process evolve to be enhanced using AI tools? A future process could start with an automated data extraction and reconciliation process, the results of which are reviewed by an AI-driven agent, which “understands” materiality and has been trained to query major data discrepancies with the relevant personnel in the Finance, IT and underwriting teams. Based on information received from these teams, an automated written report on data quality will be sent to the reserving actuaries, highlighting those areas that need manual intervention to resolve. Another AI-driven process will review the AvE exhibits, highlighting major areas of concern while being able to collate information across lines of business to pick up, automatically, on common trends. Written reporting from this system can then be used to guide the next step of analysis. Instead of manually selecting reserving assumptions for each line of business, the reserving actuary will update a large-scale neural network-based reserving model, fit across all lines of business simultaneously to enhance the credibility of the assumptions, leading to more accurate reserve indications that automatically allow for common trends across the entire business. Updating the model for all lines of business takes only a few hours, with most of the time spent waiting for the new model parameters to be fit on high-performance computers. These initial reserves can be compared to other automated reserving procedures available to the actuary, perhaps including methods that automatically select the best combination of traditional techniques such as the chain-ladder, BF and Cape Cod methods. Where the actuary is not entirely happy with the automated results, lines of business can be reserved for manually. Finally, an LLM summarizes the results of the reserving exercise and builds a presentation for the wider business, describing key changes, new insights and financial impacts on the bottom line. The reserving actuaries can use some of the time saved preparing the reserves to communicate the outcomes of the exercise to all relevant stakeholders, for example, the pricing teams within the insurer, as well as dive deeper into emerging trends or other issues coming to their attention.

Side tracked

Imagine that during this reserving process, it comes to the reserving team’s attention that a new line of business was launched over the course of the last year. The innovative new product covers errors and omissions (E&O) and crisis management for AI-based systems deployed by the company’s policyholders in their business operations. Only three quarters of reserve development is available for the actuary to derive a reserve indication from, and the loss experience to date is very noisy due to the small volumes of business currently written. The actuary decides to fine-tune a small parameter vector for the new line of business using the main company reserving neural network. Comparing the fine-tuned parameter vector for the new product to the other parameters in the model, the actuary finds that the most similar line of business is cyber insurance, followed by product recall. Given this intuitive outcome, the actuary is satisfied enough to exercise his/her expert judgement and recommend the indicated reserves for booking.

During the annual audit of the reserves by the company’s external auditors, the auditors challenge the reserving actuaries: they have noticed that on several long-tailed lines of business, the company’s neural network model allows for quite significant negative development, whereas the market practice is not to allow for negative development but rather include a tail factor. The auditors make a recommendation that the model be adjusted accordingly. To accommodate this feedback, the actuary investigates methods to align AI models to human feedback and discovers that neural networks can be informed by prior judgements, either through Bayesian techniques or by imposing suitable constraints on the network. After implementing these, judgement-based tail factors are incorporated into selected lines of business.

Are we there yet?

How far away are we for this vision of a future state for reserving? Thinking about the specific tools mentioned in the example before, neural network techniques for modelling many reserving triangles simultaneously with an allowance for common trends already exist (Gabrielli, Richman, and Wüthrich 2020) and methods for automating the selection of traditional techniques (Balona and Richman 2020) are available on the CAS’s GitHub repository (Balona 2023)! Transfer learning of a large pre-trained model to a situation where less data is available has been done, for example, in the case of yield curve forecasting (Richman and Scognamiglio 2024; Gabrielli, Richman, and Wüthrich 2020). Imposing constraints on neural networks can be done using pseudo-data (Richman and Wüthrich 2023b), or, more generally, aligning AI models to human expectations can be performed using reinforcement learning (Ouyang et al. 2022). On the other hand, these methods are not necessarily accessible to actuaries without some machine and deep learning training, and some coding skills; moreover, the robustness of these methods in the many difficult reserving situations that one encounters in practice still needs to be validated. Frameworks for building AI agents are already freely available, as are the tools to fine-tune LLMs for actuarial purposes, but the hard work of building these types of new actuarial tools has not yet been done. More subtly, the use of neural network models in practice, and the exercise of professional judgement on the results of these, needs more development as a professional competence. So, in summary, this vision of a future state for reserving is quite plausible and could be accomplished, in my view, in the next 5-10 years. In a similar manner, one can imagine applying both specific and general AI tools to other core actuarial processes, such as rating, pricing, capital modelling and new areas of actuarial practice that will become important, such as climate change analytics.

Speed-bumps on the way

What can we say about some of the challenges that implementing an AI-enhanced actuarial process might encounter? Indeed, these might be more difficult to overcome than the technological and methodological challenges we have mentioned above.

Among the first speed-bumps that are encountered when talking about AI models is the issue of explainability, which can be summarized as saying that typical models built using machine and deep learning are so-called “black boxes” which do not give access to the underlying rationale for the predictions that they make. On the other hand, actuaries and many other stakeholders in insurers are used to understanding the various factors that contribute to model outputs, for example, by having easy access to tables of relativities from pricing models. An emerging solution to this problem is to use inherently explainable AI models, which give access to the underlying rationale for the predictions made with these. A recent example of these types of models maintains the same model structure as a GLM, while predicting the relativities of the GLM for each record in the pricing dataset using a neural network (Richman and Wüthrich 2023a); other solutions also are available allowing actuaries to move away from “black box” models (Sudjianto et al. 2023; Richman 2022). A different approach is to apply model interpretability methods such as SHAP; these methods take the form of numerical “recipes” to extract explanations from black-box models (Mayer, Meier, and Wüthrich 2023).

Explainable modelling will likely be required for regulators, at least in the short- and medium-term. In the United Kingdom, for example, regulations governing actuarial work require models to be understandable (Financial Reporting Council 2023). Focusing on the United States where rates are required to be filed, it could be the case that future regulatory developments may, for example, permit the use of more complex models than GLMs if these are explainable (National Association of Insurance Commissioners 2020). Even if AI models are not permitted for predicting the technical rates to be used to price insurance policies, there are significant other uses of these models within pricing and ratemaking — for example, experience monitoring, portfolio optimization and automated underwriting.

Another issue that will almost inevitably be encountered is a perceived increased risk of potential bias and discrimination within AI-based models. Focusing on narrow AI models, this concern is often raised when considering pricing models, which may inadvertently charge differential rates to those of certain protected classes, such as gender or ethnicity, in the process violating laws or regulations. This topic has been discussed quite extensively in recent actuarial literature and new solutions, such as discrimination-free pricing (Lindholm et al. 2022), have been proposed. In more general AI models such as LLMs, there is emerging evidence of a similar phenomenon (Hofmann et al. 2024). Actuaries, who have a technical and professional competence in dealing with issues of fairness and allocation of resources among groups (for example, the management of with-profits life insurance business), seem exceptionally well placed to develop robust, practical solutions for these issues.

A final speed-bump relates to ensuring that actuaries have sufficient knowledge and experience to use AI models successfully. Currently, the main actuarial syllabuses do not have a deep coverage of AI models, thus, the majority of actuaries may be insufficiently prepared to use these models from a technical perspective. Even those actuaries with a sound technical understanding may, nonetheless, have not had much experience applying these models practically. At the moment, excellent resources exist for augmenting the actuarial syllabus with new ML and AI material (Wüthrich and Merz 2023), and it seems that with a relatively minor redesign of the syllabus, adequate coverage could easily be achieved (Harris, Richman, and Wuthrich 2024). This could be accomplished by adding a new subject focusing on ML and AI topics, covering both the theory of these areas, and practical applications within actuarial work.

The paths that lie ahead

Different paths appear to lie ahead of the actuarial profession. The safest path in the short-term is the one that we actuaries, as a global profession and community, find ourselves on today: doing what actuaries have always done and not rapidly embracing AI tools and techniques within actuarial practice, perhaps because of regulatory demands or due to some of the speed-bumps mentioned earlier. In the mid- to longer-term, however, actuaries might come under increasing pressure from other professionals, such as data scientists or machine learning engineers, who can also build models, may have more advanced knowledge than actuaries and are unconstrained by the requirements of professional guidance or regulation.

A different path might be to react to emerging developments in too extreme a manner, for example, removing traditional actuarial concepts such as credibility or Bayesian techniques from the education syllabus in favor of ML and AI, and lose much of the key knowledge that distinguishes actuarial science, from, for example, statistics.

A middle way is for actuaries to evolve into an AI-enhanced actuarial profession, where new tools are adopted within the context of the traditional actuarial knowledge-base and professionalism that distinguish actuaries today. On this path, AI-enhanced actuaries embrace the new opportunities offered by AI tools, both narrow and general, and in doing so, are able to perform actuarial work that is more advanced and more efficient than currently possible. This would cement the role of the actuarial profession in P&C insurance and wider world for decades to come. A central part of this vision is adapting AI for actuarial purposes, to ensure that the outputs of these models meet technical, professional and ethical standards, and, in part, this has already been achieved (Harris, Richman, and Wuthrich 2024). Importantly, by following this path, actuaries will still be equipped to deal with situations where purely data-driven solutions will not work! For example, these situations include launching a line of business in a new territory where the experience is likely to be totally different, or pricing and reserving for a line of business with very low frequency and potentially high severity, such as excess casualty. In these cases, traditional techniques and professional judgement will likely be the main tools utilized by actuaries, and maintaining the expertise to apply these tools is important for the profession.

The actuarial profession is at an inflection point, where choices made whether to embrace AI and ML in the next few years will determine if the profession thrives in the age of AI or merely survives in its current form. We hope that the vision of AI-enabled actuaries discussed here will encourage the evolution of the AI-enhanced actuary.

Potential future roles for actuaries in AI

If we suppose that the AI-enhanced actuary becomes a reality, new opportunities may arise for actuaries to contribute to the broader AI field. While it might be argued that the boat has sailed for actuaries to play a significant role in shaping the general development of AI, there are still several areas where the unique combination of actuarial expertise and AI knowledge could prove valuable.

One potential avenue is in the development of AI systems for risk assessment and management beyond the traditional insurance domain. Actuaries’ deep understanding of risk quantification, coupled with their newfound AI skills, could be applied to fields such as finance, healthcare, and climate risk management and reporting. Actuaries could help design and validate AI models that assess and mitigate risks in these complex domains, ensuring that the models are not only accurate but also transparent, fair, and aligned with regulatory requirements.

Another opportunity lies in the realm of AI governance and ethics. As AI systems become increasingly prevalent in decision-making processes that affect individuals and society as a whole, there is a growing need for professionals who can bridge the gap between technical AI development and ethical considerations. Actuaries, with their strong professional code of conduct and experience in balancing competing interests, could play a crucial role in shaping AI governance frameworks and ensuring that AI systems are deployed responsibly and transparently. This would be especially compelling if actuaries can decisively deal with and mitigate the problems of unwanted and indirect discrimination within current pricing models (Lindholm et al. 2023), proving their capabilities in this area.

Furthermore, actuaries could contribute to the development of AI systems that are more resilient and adaptable to changing conditions. By leveraging their expertise in stress testing, scenario analysis, and model validation, actuaries could help design AI systems that are better equipped to handle uncertainty and adapt to evolving risks, while remaining resilient under situations of extreme stress. This could be particularly valuable in fields such as autonomous systems, where the ability to anticipate and respond to unexpected situations is critical.

While the specific roles for actuaries in the broader AI field may continue to evolve, it is clear that the combination of actuarial expertise and AI knowledge could open up new opportunities for the profession to make valuable contributions beyond the traditional insurance domain. As actuaries embrace AI and develop new skills, they may find themselves well-positioned to shape the responsible development and deployment of AI systems across various industries and domains.

Value creation and the AI-enhanced actuary

Turning back to the domain of insurance, the integration of AI into actuarial practice has the potential to create significant value for multiple stakeholders, including society, policyholders, insurers, and actuaries themselves. Through actuaries harnessing both narrow and general AI, the insurance industry as a whole can become more efficient, responsive, and customer-centric, ultimately benefiting all parties involved.

For society as a whole, AI-enhanced actuarial work can contribute to a more stable and resilient insurance market by enabling more accurate risk assessments and pricing. In an age of accelerating weather related losses, this becomes especially important to ensure well-functioning insurance markets where coverage is provided at the right price.

Similarly, policyholders stand to benefit from AI-driven innovations in several ways. First, more granular risk segmentation and personalized pricing enabled by AI can lead to fairer premiums that better reflect individual risk profiles. This means that low-risk policyholders may enjoy lower premiums, while high-risk individuals can still obtain coverage at appropriate rates. Second, AI can facilitate the development of customized insurance products that cater to specific needs and preferences of policyholders, providing more targeted and valuable coverage, for example through incorporating advanced data sources such as telematics or wearable devices directly into the rating process. Finally, an obvious benefit of more general LLM powered AI — currently being realized in several more advanced insurers — is efficient claims processing and customer service that can lead to faster, more efficient, and more responsive interactions between policyholders and insurers, improving the overall customer experience.

Actuaries themselves have much to gain from embracing AI in their work. By augmenting and enhancing their skills with AI tools and systems, actuaries can enhance their predictive modeling capabilities, tackle more complex problems, and provide more valuable insights to their organizations. AI can also automate routine tasks, freeing up actuaries to focus on higher-level strategic initiatives and decision-making, while enabling more accurate modelling than was previously possible. Moreover, as AI becomes increasingly prevalent in the insurance industry, actuaries who are proficient in AI techniques will be well-positioned to take on leadership roles and drive innovation within their companies.

In summary, the integration of AI into actuarial practice creates a virtuous cycle of value creation for all stakeholders. By enabling more accurate risk assessments, personalized products based on advanced data sources, efficient operations, and data-driven decision-making, AI can help build a more robust, responsive, and customer-centric insurance industry. As the profession continues to evolve, AI-enhanced actuaries who embrace AI methodologies will play a critical role in shaping the future of insurance and delivering value to society as a whole.

Conclusions

The integration of AI into actuarial practice represents a natural evolution of the profession, building upon the foundation of mathematical and statistical techniques that have been the cornerstone of actuarial work for decades. Indeed, modern advances in actuarial science allow accurate models to be built quickly and efficiently while respecting the traditional principles that underpin actuarial work.

Actuaries have long been at the forefront of using data-driven models to assess risk, price insurance products, and ensure the financial stability of insurance companies. The emergence of AI and machine learning techniques presents a significant opportunity to enhance and extend these traditional actuarial methods, and, for the next step in the evolution of the profession to produce AI-enhanced actuaries.

Furthermore, the development of explainable AI models aligns with the actuarial profession’s emphasis on transparency and interpretability. By using techniques like SHAP or inherently explainable models, actuaries can gain insights into the inner workings of complex AI models and communicate their findings to stakeholders in a clear and understandable manner. Likewise, by staying abreast of emerging themes in actuarial methodology, such as discrimination-free pricing, actuaries can deal with many of the speed-bumps mentioned in this essay. Whereas we have not ventured into the details of these, the references in the footnotes should offer a guide to those who are interested in learning more.

In essence, the integration of AI into actuarial practice represents a natural progression of the profession’s commitment to data-driven decision making and risk management. By embracing AI and machine learning, actuaries can unlock new opportunities for innovation, efficiency, and value creation, ensuring that the profession remains at the forefront of the rapidly evolving insurance industry.

Looking to the future, further research could explore the development of AI-driven tools specifically tailored to the needs of actuaries, such as automated data quality checks and reporting platforms, intelligent reserving models, or fine-tuned actuarial LLMs. These tools could incorporate the latest advancements in AI while adhering to actuarial principles and regulatory requirements. Another exciting area of research could focus on the integration of AI with traditional actuarial techniques, such as credibility theory or Bayesian methods. This could lead to the development of hybrid models that combine the strengths of both approaches, enhancing the accuracy and interpretability of actuarial models.

Research into the ethical and societal implications of AI in the insurance industry is also crucial. Future studies could investigate the impact of AI on insurance accessibility and affordability, and the role of actuaries in ensuring the responsible deployment of AI systems.

Finally, future research could delve into the potential applications of AI-enhanced actuarial techniques beyond the insurance industry. This could include areas such as finance, healthcare, and climate risk management, where the unique combination of actuarial expertise and AI knowledge could lead to interesting new techniques and open the door of new actuarial practice areas.

Acknowledgements

The author is very grateful to Mario Wüthrich for discussions of these topics and to his coauthors for the research projects which underpin this essay.